What Is a 401(k) and How Does It Work?

A 401(k) plan is an employer-sponsored retirement savings account that allows you to set aside pre-tax money from your paycheck for retirement. It's one of the most popular ways Americans build long-t...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

A 401(k) plan is an employer-sponsored retirement savings account that allows you to set aside pre-tax money from your paycheck for retirement. It's one of the most popular ways Americans build long-term wealth, and understanding how it works can help you make the most of this powerful savings tool.

What Is a 401(k)?

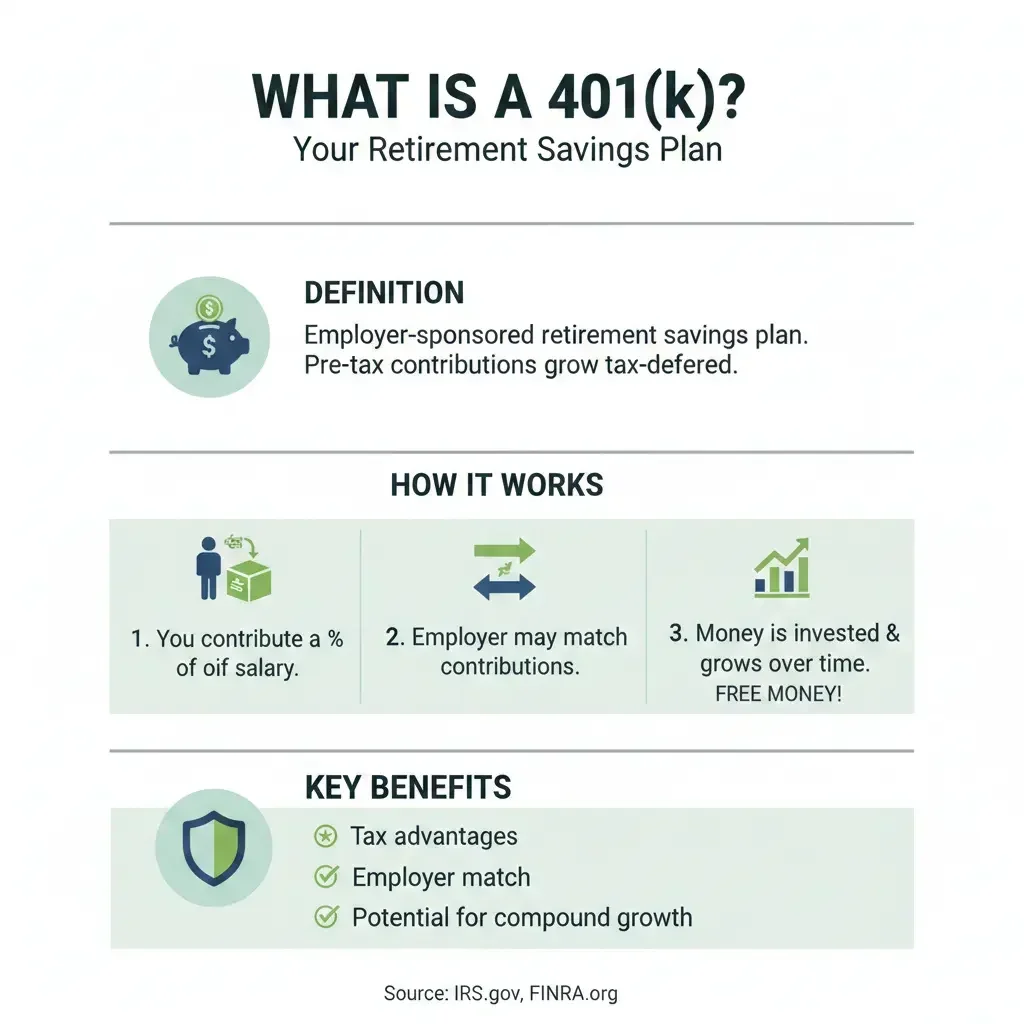

A 401(k) is a qualified retirement plan named after the section of the Internal Revenue Code that governs it. It's offered by employers to their employees as an employee benefit, allowing workers to contribute a portion of their salary directly into a retirement account before taxes are taken out. The money you contribute grows tax-deferred, meaning you don't pay income taxes on the contributions or investment earnings until you withdraw the money in retirement.

The plan gets its name from Section 401(k) of the Internal Revenue Code, which outlines the rules and regulations for these plans. Most employers who offer 401(k)s use them as a core retirement benefit to help employees save for their future.

How Does a 401(k) Work?

Employee Contributions

When you enroll in your employer's 401(k) plan, you choose a percentage of your gross salary to contribute. This money is automatically deducted from your paycheck before income taxes are calculated, reducing your taxable income for the year. For 2026, you can contribute up to $24,500 per year if you're under age 50. If you're 50 or older, you can make additional "catch-up contributions" of up to $8,000 per year, bringing your total to $32,500.

There's also a special provision for workers aged 60-63. Under recent changes, these employees can contribute an additional $11,250 on top of their regular contributions, allowing them to save up to $35,750 annually.

Employer Matching

Many employers offer matching contributions as an incentive for employees to save. A common match is 50% of what you contribute, up to 6% of your salary. For example, if you earn $50,000 and contribute 6% ($3,000), your employer might contribute an additional $1,500. This is essentially free money—don't leave it on the table.

Investment Growth

Once your contributions are in the account, you choose how to invest the money from a menu of options your employer's plan provides. These typically include mutual funds, target-date funds, and sometimes company stock. Your investments grow tax-deferred, meaning you don't pay taxes on dividends, capital gains, or interest earnings until you withdraw the money.

Annual Contribution Limits

The IRS sets annual limits on how much can be contributed to your 401(k) each year. For 2026, the combined limit for employee deferrals, employer contributions, and after-tax contributions is $72,000 (or $80,000 if you're age 50 or older and eligible for catch-up contributions).

Traditional vs. Roth 401(k)

Most employers offer a traditional 401(k), where contributions are made with pre-tax dollars and you pay taxes on withdrawals in retirement. However, some employers also offer a Roth 401(k) option, where you contribute after-tax dollars but your withdrawals in retirement are tax-free.

The choice between traditional and Roth depends on your current tax bracket and expectations about your tax situation in retirement. If you expect to be in a lower tax bracket when you retire, a traditional 401(k) makes sense. If you expect to be in a higher bracket, a Roth 401(k) may be more beneficial.

Vesting: When the Money Is Really Yours

Your own contributions to your 401(k) are always yours immediately—you're 100% vested in your deferrals from day one. However, employer matching contributions often come with a vesting schedule. This means you must work for the company for a certain period before you fully own the employer's contributions.

Common vesting schedules include:

- Immediate vesting (you own employer contributions right away)

- Cliff vesting (you become 100% vested after a set period, typically 3-5 years)

- Graded vesting (you gradually own more each year, typically becoming fully vested after 5-7 years)

If you leave your job before becoming fully vested, you forfeit the unvested portion of employer contributions. Always check your plan documents to understand your specific vesting schedule.

Withdrawals and Early Withdrawal Penalties

You can't access your 401(k) money penalty-free until you reach age 59½. If you withdraw money before that age, you'll typically owe a 10% early withdrawal penalty plus income taxes on the amount withdrawn. However, there are some exceptions to this rule, including:

- Hardship withdrawals for medical expenses, home purchases, or education

- Substantially equal periodic payments

- Withdrawals due to disability or death

- Loans from your 401(k) (if your plan allows them)

Once you reach age 59½, you can withdraw money without the 10% penalty, though you'll still owe income taxes on traditional 401(k) withdrawals. At age 73, you must begin taking required minimum distributions (RMDs) from your traditional 401(k).

Key Benefits of a 401(k)

- Tax advantages: Traditional 401(k) contributions reduce your taxable income in the year you make them, potentially lowering your tax bill.

- Employer matching: Free money from your employer when they match your contributions.

- Tax-deferred growth: Your investments grow without annual tax liability.

- Automatic contributions: Payroll deduction makes saving automatic and consistent.

- High contribution limits: You can save significantly more than in an IRA ($24,500 vs. $7,500 for IRAs in 2026).

- Loan options: Some plans allow you to borrow against your balance for emergencies.

What Happens When You Change Jobs?

When you leave your job, you have several options for your 401(k):

- Leave it with your former employer: You can keep your money in the plan if your balance is above a certain amount (typically $5,000).

- Roll it to your new employer's plan: If your new job offers a 401(k), you can roll your old balance into it (if the new plan allows).

- Roll it to an IRA: You can roll your 401(k) into a traditional or Roth IRA for more investment options and potentially lower fees.

- Cash it out: You can withdraw the money, but you'll owe taxes and potentially a 10% penalty if you're under 59½.

Getting Started With Your 401(k)

If your employer offers a 401(k), enrollment is typically straightforward. Here's what to do:

- Review your employer's plan documents and enrollment materials.

- Decide on your contribution amount—start with enough to get any employer match.

- Choose your investment options from the available menu.

- Enroll through your employer's HR or benefits portal.

- Review your contributions and investments annually.

- Increase your contributions whenever you get a raise.

A 401(k) is one of the most effective tools for building retirement security. By starting early and contributing consistently, you can take advantage of decades of tax-deferred growth and employer matching to build substantial retirement savings. If you haven't enrolled in your employer's plan yet, now is the time to start—the sooner you begin, the more time your money has to grow.

Frequently Asked Questions

Sources & References

- 1

-

2

2026 Retirement Plan Contribution Limits (401k, 457(b) & More) — Mission Square — www.missionsq.org

-

3

401(k) Contribution Limits: 2024, 2025, and 2026 — Charles Schwab — www.schwab.com

-

4

401(k) Contribution Limits |2026, 2025 and Earlier — ADP — www.adp.com

-

5

What are 2026 401(k) and IRA max contribution limits? — Principal — www.principal.com

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...