Capital Gains Tax Explained for Everyday Americans

Imagine selling your home after years of ownership, only to face a surprise tax bill on the profit—or better yet, discovering ways to minimize or even eliminate it. That's the world of capital gains t...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine selling your home after years of ownership, only to face a surprise tax bill on the profit—or better yet, discovering ways to minimize or even eliminate it. That's the world of capital gains tax, a key part of managing investments for everyday Americans. Whether you're flipping stocks, selling a rental property, or cashing in on collectibles, understanding this tax can save you thousands and help you plan smarter for retirement or big life goals.

In this guide, we'll break down capital gains tax explained for everyday Americans using 2026 rates, real-world examples, and practical strategies. From short-term vs. long-term rates to exclusions and deductions, you'll get actionable steps tailored to U.S. taxpayers.

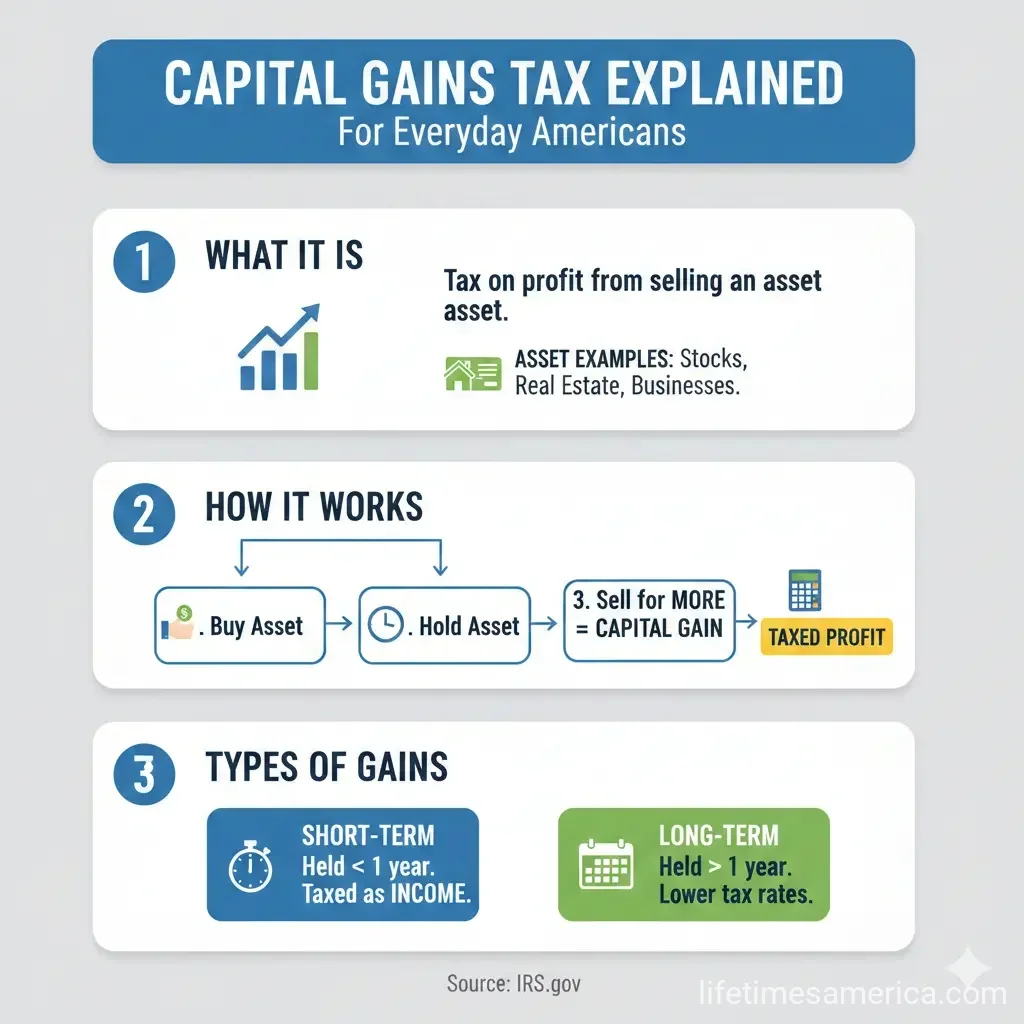

What Is Capital Gains Tax?

Capital gains tax is the federal tax you pay on the profit from selling an asset that has increased in value, like stocks, real estate, or cryptocurrency. The gain is calculated as the sale price minus your "basis"—typically what you paid for it, plus any improvements or fees.

For instance, if you bought stock for $10,000 (your basis) and sold it for $15,000, your capital gain is $5,000. This profit isn't taxed until you sell, unlike wages taxed as you earn them.

Short-Term vs. Long-Term Capital Gains

The holding period determines your tax rate:

- Short-term capital gains: Assets held one year or less. Taxed at your ordinary income tax rate, which ranges from 10% to 37% in 2026.

- Long-term capital gains: Assets held more than one year. Preferential rates of 0%, 15%, or 20%, based on your taxable income and filing status.

Why does it matter? Holding an asset longer can slash your tax bill dramatically. A $10,000 short-term gain for someone in the 24% bracket costs $2,400 in taxes, but the same long-term gain might cost just $1,500 at 15%—or nothing at 0%.

2026 Long-Term Capital Gains Tax Rates

For tax year 2026 (filed in 2027), long-term rates depend on your taxable income. Most Americans pay 0% or 15%.

| Tax Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 0% | $0 - $49,450 | $0 - $98,900 | $0 - $49,450 | $0 - $66,200 |

| 15% | $49,451 - $545,500 | $98,901 - $613,700 | $49,451 - $306,850 | $66,201 - $579,600 |

| 20% | $545,501+ | $613,701+ | $306,851+ | $579,601+ |

Note: These brackets are inflation-adjusted for 2026.

Short-Term Capital Gains Rates

Short-term gains follow 2026 ordinary income brackets, starting at 10% and topping at 37%. High earners may also face the 3.8% Net Investment Income Tax (NIIT) if modified adjusted gross income exceeds $200,000 (single) or $250,000 (joint).

Special Capital Gains Tax Rates

Not all gains are equal. Certain assets have unique rules:

- Collectibles (art, coins, antiques): Long-term max 28%; short-term at ordinary rates.

- Depreciable real estate (unrecaptured Section 1250 gain): Max 25%.

- Home sales: Exclude up to $250,000 (single) or $500,000 (joint) if you've lived there 2 of the last 5 years. Use IRS Publication 523 for details.

Example: Selling a rental property with $50,000 unrecaptured gain? Expect 25% tax on that portion, even if your long-term rate is lower.

How to Calculate Your Capital Gains Tax

- Determine your basis: Purchase price + improvements - depreciation (for rentals).

- Calculate gain: Sale price - basis - selling costs.

- Classify: Short- or long-term based on holding period.

- Apply rates: Use brackets above; stack gains on top of ordinary income for "stacking" calculation.

- Subtract losses: Offset gains with capital losses; up to $3,000 net loss deductible against ordinary income.

Real-world example: Single filer with $70,000 wages + $10,000 long-term gain. After standard deduction, taxable income ~$60,000. The gain falls in the 0% bracket—zero tax on it!

For married filing jointly with $200,000 wages + $50,000 long-term gain: Portion in 0%/15% brackets taxed accordingly after stacking.

Strategies to Minimize Capital Gains Tax

Smart planning keeps more money in your pocket:

Hold for Long-Term

Wait over a year to qualify for lower rates. Ideal for retirement accounts like 401(k)s or IRAs, where gains grow tax-deferred.

Tax-Loss Harvesting

Sell losing investments to offset gains. Carry forward excess losses indefinitely.

Use Tax-Advantaged Accounts

ROTH IRAs allow tax-free withdrawals; 529 plans for education gains.

Step-Up in Basis

Inherit assets? Basis steps up to fair market value at death, erasing prior gains for heirs.

Opportunity Zones and 1031 Exchanges

Defer gains by reinvesting in Qualified Opportunity Zones or like-kind exchanges for real estate.

Pro tip: Time sales to fill lower brackets. If nearing retirement, realize gains in low-income years.

State Capital Gains Taxes

Federal rules apply nationwide, but 41 states tax capital gains as ordinary income (rates 0%-13.3%). No state tax in AK, FL, NV, NH, SD, TN, TX, WA, WY. Check your state's revenue department.

Reporting Capital Gains on Your Taxes

Brokers send Form 1099-B. Report on Schedule D (Form 1040). Use IRS Free File or software like TurboTax for accuracy. Deadline: April 15, 2027, for 2026 taxes (extensions available).

"Net short-term capital gains are subject to taxation as ordinary income at graduated tax rates." — IRS Topic No. 409

Next Steps for Managing Your Capital Gains

Review your portfolio today: Identify short-term holdings to consider extending, harvest losses before year-end, and model scenarios with a calculator. Consult a CPA or use IRS tools at irs.gov for personalized advice—this isn't tax advice, so verify with a professional for your situation.

Track basis meticulously, contribute to retirement accounts, and plan sales strategically. With these tools, you'll navigate capital gains tax like a pro and keep more of your hard-earned profits.

Frequently Asked Questions

Sources & References

-

1

2025 and 2026 Capital Gains Tax Rates and Rules - NerdWallet — www.nerdwallet.com

- 2

- 3

- 4

-

5

Capital gains tax (CGT) rates - PwC — taxsummaries.pwc.com

-

6

A Guide to the Capital Gains Tax Rate: Short-term vs. ... - TurboTax — turbotax.intuit.com

-

7

2025-2026 Tax Brackets & Federal Income Tax Rates | H&R Block® — www.hrblock.com

Useful Tools

Related Articles

How to Avoid the "Marriage Penalty" in the 2026 US Tax Code

Imagine tying the knot and then discovering your tax bill just skyrocketed—thousands of dollars higher than if you'd stayed single. That's the harsh reality of the marriage penalty in the US tax code,...

The Best "Side-Hustle" Tax Software for 2026 Filers

Running a side hustle in 2026 means juggling gigs like Uber driving, freelance graphic design, or selling handmade crafts on Etsy while keeping your day job. But come tax time, tracking those 1099-NEC...

How to Use "Tax-Loss Harvesting" to Offset Your 2026 Stock Gains

Imagine locking in hefty stock gains in 2026 only to watch a big chunk vanish to capital gains taxes. What if you could slash that tax bill without derailing your investment strategy? That's the power...

The Gig Economy Tax Guide: How to Deduct Your Car; Internet; and Office

If you're earning money through gig work—whether you're driving for a rideshare company, freelancing, delivering groceries, or running a side hustle—you're probably wondering how to keep more of what...