What Is the Standard Deduction in the USA?

When you file your federal income tax return, you'll encounter one of the most important numbers in the entire tax code: the standard deduction. This dollar amount directly reduces the income you owe...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

When you file your federal income tax return, you'll encounter one of the most important numbers in the entire tax code: the standard deduction. This dollar amount directly reduces the income you owe taxes on, potentially saving you hundreds or even thousands of dollars. Understanding how it works—and whether you should take it—is essential for every American taxpayer.

What Is the Standard Deduction?

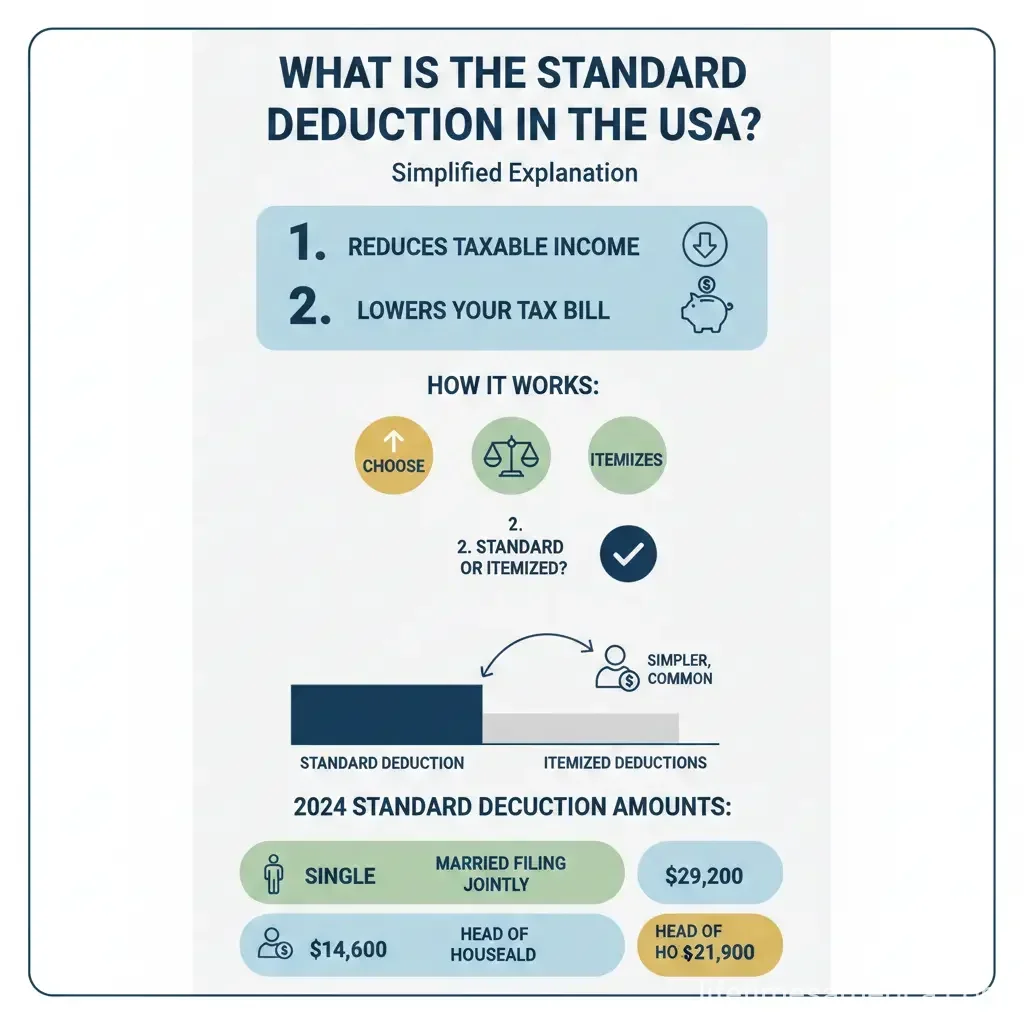

The standard deduction is a flat dollar amount that reduces your taxable income based on your filing status. Think of it as a baseline reduction the IRS gives you before calculating how much federal income tax you owe. If your income falls below the standard deduction for your filing status, you typically won't owe any federal income tax at all.

The IRS adjusts the standard deduction annually for inflation, which means the amounts change each year. For the 2025 tax year (returns filed in April 2026), the standard deduction ranges from $15,750 for single filers to $31,500 for married couples filing jointly.

2025 and 2026 Standard Deduction Amounts

Here's what you can claim based on your filing status:

2025 Tax Year (Filed in 2026)

For the 2025 tax year, the standard deduction amounts are:

- Single filers: $15,750

- Married filing jointly: $31,500

- Married filing separately: $15,750

- Head of household: $23,625

- Qualifying surviving spouse: $31,500

2026 Tax Year (Filed in 2027)

For the 2026 tax year, amounts increase slightly due to inflation:

- Single filers: $16,100

- Married filing jointly: $32,200

- Married filing separately: $16,100

- Head of household: $24,150

- Qualifying surviving spouse: $32,200

Additional Standard Deduction for Seniors (Age 65+)

If you're 65 or older, you're eligible for an extra standard deduction on top of your base amount. For 2026, seniors can claim an additional $6,000 deduction. This means a single filer age 65+ can deduct $22,100 instead of $16,100 for the 2026 tax year.

This additional deduction is subject to an adjusted gross income (MAGI) limitation. For 2026, the income thresholds are:

- Single filers and heads of household: $75,000 or less (MAGI)

- Joint filers and surviving spouses: $150,000 or less (MAGI)

If your income exceeds these limits, your additional $6,000 deduction is reduced by 6 cents for every dollar over the threshold. Some high-income seniors may not qualify for the full benefit.

Additional Standard Deduction for Blindness

If you're blind, you're also entitled to an additional standard deduction. The amount depends on your filing status and marital situation, but this benefit helps ensure blind taxpayers aren't disadvantaged in the tax code.

Standard Deduction vs. Itemized Deductions

Here's a critical point: you can only claim one deduction method—either the standard deduction or itemized deductions, but not both. Most Americans take the standard deduction because it's simpler and often results in a larger deduction.

However, if you have significant deductible expenses, itemizing might save you more money. Itemized deductions can include:

- State and local income or sales taxes

- Real property taxes

- Mortgage interest

- Charitable donations

- Medical and dental expenses

- Disaster losses

- Certain gambling losses

If your total itemized deductions exceed your standard deduction, you should itemize. Otherwise, take the standard deduction and keep your tax filing straightforward.

New Tax Deductions for 2026

The IRS introduced several new deductions for the 2026 tax year that go beyond the standard deduction:

- Tipped workers: Can deduct up to $25,000 for qualified tips

- Overtime workers: Can deduct up to $12,500 ($25,000 for joint filers) for qualified overtime

- Vehicle loan interest: Can deduct up to $10,000 in qualified passenger vehicle loan interest

- Charitable donations: Non-itemizers can deduct cash donations to charity—up to $1,000 for single filers or $2,000 for married couples filing jointly

These deductions are available in addition to your standard deduction, which means they can further reduce your taxable income.

Who Can't Take the Standard Deduction?

Most Americans can claim the standard deduction, but certain taxpayers aren't eligible:

- Married individuals filing separately whose spouse itemizes deductions

- Nonresident aliens or dual status aliens (with limited exceptions)

- Individuals filing for a period of less than 12 months due to accounting period changes

- Estates, trusts, common trust funds, or partnerships

Additionally, if you can be claimed as a dependent by another taxpayer, your standard deduction is limited to the greater of $1,350 or your earned income plus $450 (but not more than the basic standard deduction for your filing status).

How the Standard Deduction Affects Your Taxes

Here's a practical example: If you're a single filer in 2026 with $35,000 in income, your taxable income would be calculated as follows:

$35,000 (gross income) − $16,100 (standard deduction) = $18,900 (taxable income)

You'd only pay federal income tax on $18,900, not the full $35,000. This is why the standard deduction is so valuable—it directly reduces the amount of income subject to taxation.

If your income is below the standard deduction for your filing status, you typically won't owe federal income tax. However, you may still want to file a return if you're eligible for refundable tax credits like the Earned Income Tax Credit (EITC) or the Child Tax Credit.

Key Dates and Deadlines

For the 2025 tax year, the filing deadline is Wednesday, April 15, 2026. You can request an extension if you need more time, but any taxes owed are still due by the original deadline date.

Next Steps

Understanding the standard deduction is the first step toward smarter tax planning. Here's what you should do:

- Calculate your estimated deduction: Use your filing status and age to determine your standard deduction amount.

- Gather your documents: Collect income statements (W-2s, 1099s) and any deduction documentation.

- Consider itemizing: If you have significant deductible expenses, calculate whether itemizing would save you more.

- File before April 15, 2026: Meet the deadline for the 2025 tax year or request an extension.

- Consult a tax professional: If your situation is complex, a CPA or tax advisor can help you optimize your deductions.

The standard deduction is one of the most valuable tools in the tax code for reducing your tax burden. By understanding how it works and ensuring you're claiming the correct amount, you'll keep more of your hard-earned money and simplify your tax filing process.

Frequently Asked Questions

Sources & References

-

1

Standard Deduction 2025-2026: Amounts, How It Works — NerdWallet — www.nerdwallet.com

- 2

-

3

Tax Deductions 2025-2026: What's New or Changed — TurboTax — turbotax.intuit.com

- 4

- 5

-

6

2025 and 2026 Tax Brackets and Federal Income Tax Rates — Fidelity — www.fidelity.com

Useful Tools

Related Articles

How to Avoid the "Marriage Penalty" in the 2026 US Tax Code

Imagine tying the knot and then discovering your tax bill just skyrocketed—thousands of dollars higher than if you'd stayed single. That's the harsh reality of the marriage penalty in the US tax code,...

The Best "Side-Hustle" Tax Software for 2026 Filers

Running a side hustle in 2026 means juggling gigs like Uber driving, freelance graphic design, or selling handmade crafts on Etsy while keeping your day job. But come tax time, tracking those 1099-NEC...

How to Use "Tax-Loss Harvesting" to Offset Your 2026 Stock Gains

Imagine locking in hefty stock gains in 2026 only to watch a big chunk vanish to capital gains taxes. What if you could slash that tax bill without derailing your investment strategy? That's the power...

The Gig Economy Tax Guide: How to Deduct Your Car; Internet; and Office

If you're earning money through gig work—whether you're driving for a rideshare company, freelancing, delivering groceries, or running a side hustle—you're probably wondering how to keep more of what...