What Is the Earned Income Tax Credit (EITC)?

Imagine getting money back from the IRS even if you owe little or no taxes—that's the power of the Earned Income Tax Credit (EITC). This refundable credit puts real cash in the pockets of millions of...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine getting money back from the IRS even if you owe little or no taxes—that's the power of the Earned Income Tax Credit (EITC). This refundable credit puts real cash in the pockets of millions of low- to moderate-income American workers every year, helping families cover essentials like groceries, rent, or school supplies.

Whether you're a single parent juggling two jobs, a young worker without kids, or part of a household scraping by on modest wages, the EITC could mean thousands in your bank account come tax time. In this guide, we'll break down everything you need to know about the EITC for the 2025 tax year (returns filed in 2026), including who qualifies, how much you might get, and how to claim it. Let's dive in so you can maximize your refund.

What Is the Earned Income Tax Credit (EITC)?

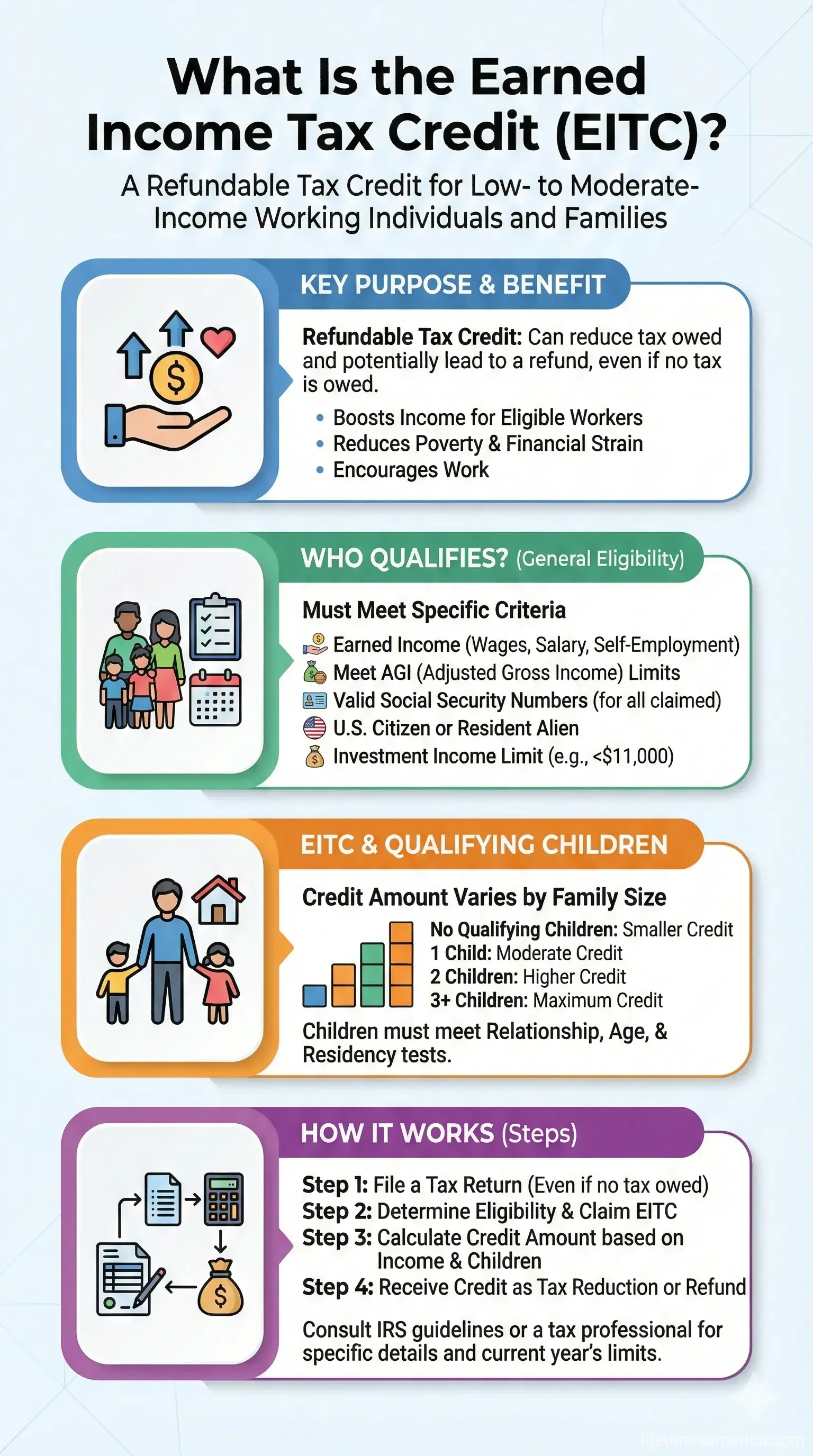

The Earned Income Tax Credit (EITC), also called the Earned Income Credit (EIC), is a federal tax credit designed to boost the take-home pay of low- and moderate-income workers. Unlike a deduction that reduces taxable income, the EITC directly lowers your tax bill dollar-for-dollar. Because it's refundable, if the credit exceeds what you owe, the IRS sends you the difference as a check or direct deposit.

Created in 1975, the EITC rewards work by basing the credit on your earned income—think wages from a job, tips, or self-employment profits. It phases in as you earn more (up to a maximum), stays flat, then phases out at higher incomes. Families with qualifying children get bigger credits, but childless workers can qualify too.

"The earned income tax credit subsidizes low-income working families. The credit equals a fixed percentage of earnings from the first dollar until it reaches its maximum."

In 2024, over 25 million households claimed the EITC, receiving about $70 billion in refunds. For 2025 taxes filed in 2026, amounts are inflation-adjusted upward, offering slightly more relief amid rising costs.

How Does the EITC Work?

The EITC follows a simple structure:

- Phase-in: Credit grows with your earned income (e.g., 34% rate for families with three kids).

- Plateau: Hits maximum credit and stays there.

- Phase-out: Reduces gradually until zero, based on income thresholds.

This design ensures the biggest boost goes to those who work but earn modestly. Use the IRS EITC Assistant tool online to estimate your credit instantly.

Who Qualifies for the EITC in 2026?

Not everyone gets the EITC, but if you meet these basics, you might. Key requirements include having earned income, staying under income limits, and following rules on age, residency, and investment income.

Basic Eligibility Rules

To claim the EITC:

- Have at least $1 in earned income (wages, salaries, tips, net self-employment income, or farm/business earnings). No earned income? No credit.

- Meet adjusted gross income (AGI) and earned income limits (see table below).

- Investment income under $11,950 for 2025 (rising to $12,200 in 2026).

- Not be claimed as a dependent or qualifying child on another's return.

- Live in the U.S. for more than half the year.

Special Rules for Workers Without Qualifying Children

Childless? You still qualify if:

- Age 25 to 64 at year-end.

- Meet income limits (strictest at $19,104 single/$26,214 joint).

- One spouse meets age rule if married filing jointly.

What Counts as a Qualifying Child?

A qualifying child boosts your credit big time. They must be:

- Your child, stepchild, foster child, sibling, or descendant (under 19, or 24 if full-time student; no age limit if permanently disabled).

- Live with you in the U.S. over half the year.

- Not file a joint return (unless only for refund).

- Not support themselves via another job.

Pro tip: Same child can qualify for both EITC and Child Tax Credit (CTC).

2025 EITC Income Limits and Maximum Credits

For taxes filed in 2026 (2025 tax year), here's the breakdown. Both earned income and AGI must be below these thresholds.

| Number of Qualifying Children | Maximum Credit | Income Limit (Single/Head of Household) | Income Limit (Married Filing Jointly) |

|---|---|---|---|

| None | $649 | $19,104 | $26,214 |

| One | $4,328 | $50,434 | $57,554 |

| Two | $7,152 | $57,310 | $64,430 |

| Three or More | $8,046 | $61,555 | $68,675 |

Investment income limit: $11,950 or less. Thresholds adjust annually for inflation; check IRS updates for 2026 tax year.

Example: Maria, a single mom with two kids, earns $35,000 in wages. Her AGI qualifies under $57,310. She gets the full $7,152 max credit, refunded since she owes minimal tax.

How to Calculate and Claim Your EITC

Don't guess—use free tools:

- Run your numbers through the IRS EITC Assistant.

- File Form 1040 with Schedule EIC if you have kids.

- Choose direct deposit for fastest refund (up to 21 days).

Free File program (for AGI under $79,000) or VITA sites offer help. Deadline: April 15, 2026 (or October with extension).

Common Mistakes to Avoid

- Forgetting qualifying kids or wrong SSN.

- Miscalculating self-employment income (use Schedule C).

- Exceeding investment limits (interest, dividends count).

- Not filing prior-year returns—claim up to 3 years back.

Accuracy matters: Wrong claims trigger audits. Double-check with IRS Publication 596.

Practical Tips to Maximize Your EITC Refund

Make the most of this credit:

- Track earned income: Save W-2s, 1099s religiously.

- Combine credits: Stack with CTC, Child and Dependent Care Credit.

- Self-employed? Deduct business expenses first to lower AGI.

- Advance EITC: Get half monthly via employer (Form W-5).

- State EITC: 30+ states offer matches (e.g., California's up to 50% of federal).

A family of four earning $25,000 might pocket $7,000+ combined federal/state—enough for a month's rent.

Next Steps to Claim Your EITC

Ready to grab your refund? Start with the IRS EITC Assistant today, gather your docs, and file early in 2026. Use free tax help via VITA or IRS Free File to avoid prep fees. Remember, tax laws change—consult IRS.gov or a pro for your situation. This isn't advice; see a tax professional for personalized guidance.

Claiming the EITC isn't just smart—it's a game-changer for hardworking Americans. Don't leave money on the table.

Frequently Asked Questions

Sources & References

-

1

Earned Income Tax Credit (EITC) definition — usafacts.org — usafacts.org

-

2

What is the earned income tax credit? — taxpolicycenter.org — taxpolicycenter.org

-

3

Earned Income Tax Credit (EITC): What It Is, Who Qualifies — nerdwallet.com — www.nerdwallet.com

-

4

The Earned Income Tax Credit — michiganlegalhelp.org — michiganlegalhelp.org

-

5

Earned Income Tax Credit (EITC) 2025 & 2026 — kiplinger.com — www.kiplinger.com

- 6

-

7

How Much is My Child Tax Credit or Earned Income Tax Credit — bipartisanpolicy.org — bipartisanpolicy.org

Useful Tools

Related Articles

How to Avoid the "Marriage Penalty" in the 2026 US Tax Code

Imagine tying the knot and then discovering your tax bill just skyrocketed—thousands of dollars higher than if you'd stayed single. That's the harsh reality of the marriage penalty in the US tax code,...

The Best "Side-Hustle" Tax Software for 2026 Filers

Running a side hustle in 2026 means juggling gigs like Uber driving, freelance graphic design, or selling handmade crafts on Etsy while keeping your day job. But come tax time, tracking those 1099-NEC...

How to Use "Tax-Loss Harvesting" to Offset Your 2026 Stock Gains

Imagine locking in hefty stock gains in 2026 only to watch a big chunk vanish to capital gains taxes. What if you could slash that tax bill without derailing your investment strategy? That's the power...

The Gig Economy Tax Guide: How to Deduct Your Car; Internet; and Office

If you're earning money through gig work—whether you're driving for a rideshare company, freelancing, delivering groceries, or running a side hustle—you're probably wondering how to keep more of what...