What Is an Annuity and Should You Buy One for Retirement?

An annuity is a contract between you and an insurance company that converts your savings into a guaranteed income stream for retirement[1]. Whether you should buy one depends on your retirement goals,...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

An annuity is a contract between you and an insurance company that converts your savings into a guaranteed income stream for retirement. Whether you should buy one depends on your retirement goals, risk tolerance, and financial situation—but for many Americans, annuities offer valuable protection against outliving your money.

Understanding Annuities: The Basics

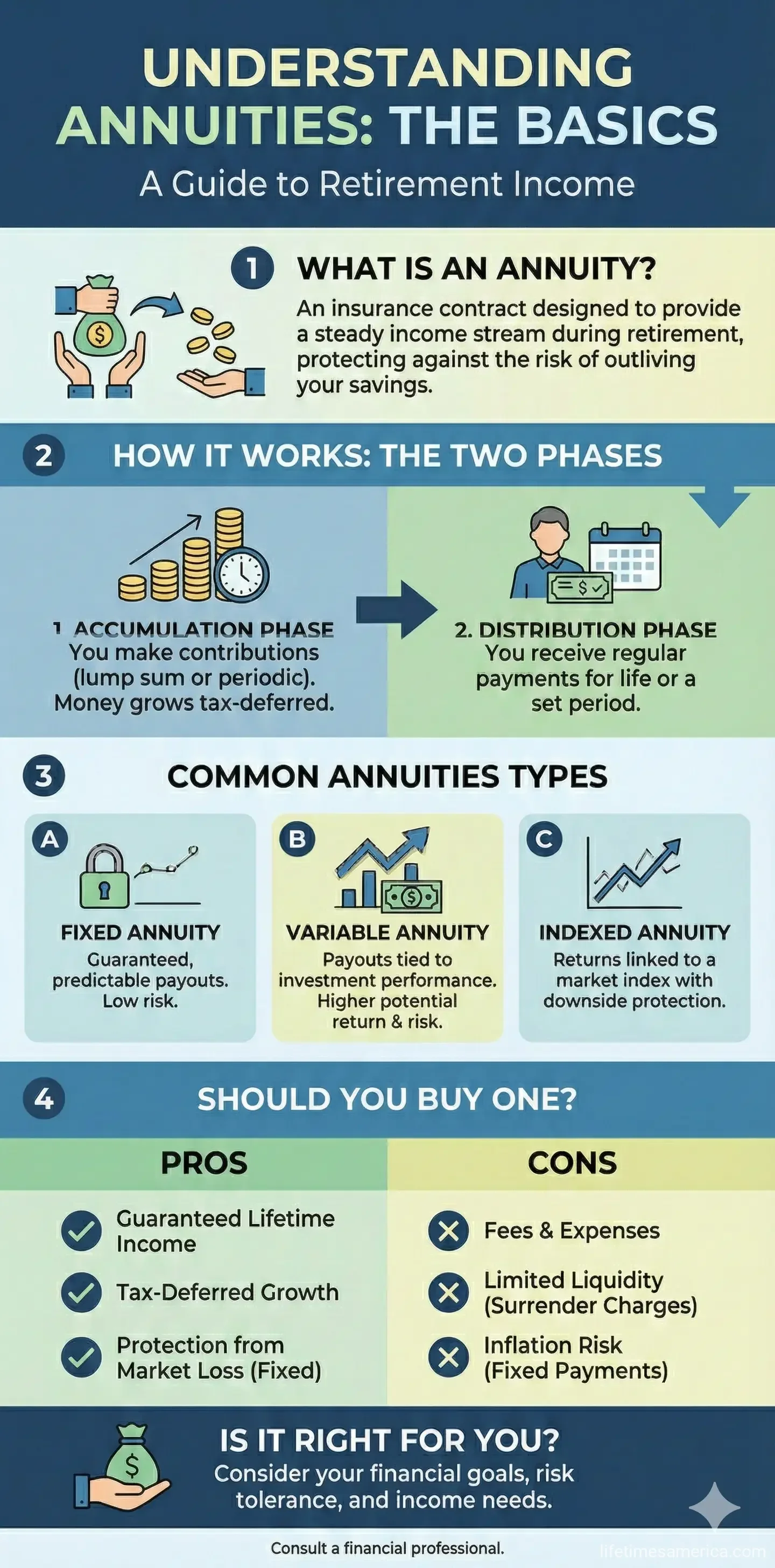

At its core, an annuity is a long-term retirement investment product issued by an insurance company. You pay money upfront (either as a lump sum or over time), and in return, the insurance company promises to pay you income—either immediately or at a future date. This arrangement shifts some of your financial risk onto the insurance company, which can be especially valuable during retirement when you're no longer earning a paycheck.

Annuities work in two main phases: the accumulation phase, when you contribute money and it grows (often tax-deferred), and the distribution phase, when you receive regular income payments.

The Two Main Categories of Annuities

Immediate Annuities

Immediate annuities are designed for retirees who want income right away. You make a single lump-sum payment, and the insurance company typically starts paying you within one year. These are ideal if you've just retired and want to convert a portion of your savings into a guaranteed "paycheck" immediately. The income amount is calculated based on your age, the lump sum you invest, and your chosen payout option.

Deferred Annuities

Deferred annuities let you accumulate savings over time with the option to convert them into income later. This approach works well if you're still working and want to build retirement income for future years. Your money grows tax-deferred during the accumulation phase, and you can annuitize (convert to income) at a time that matches your retirement timeline.

Types of Deferred Annuities

Fixed Annuities

Fixed annuities are the most straightforward option and appeal to conservative investors. The insurance company guarantees a fixed interest rate on your contributions, which generates a steady, predictable income stream. Your returns don't fluctuate with the stock market—instead, they grow at a rate determined by the insurance company's general account investments. Fixed annuities are considered one of the safest retirement investment options, similar to certificates of deposit.

Best for: Conservative savers who prioritize predictability and principal protection over growth potential.

Variable Annuities

Variable annuities offer growth potential by allowing you to choose where your contributions are invested. You typically have low-, moderate-, and high-risk investment options available. Your income payments increase or decrease based on how your chosen investments perform. If your portfolio performs well, your payments grow—potentially helping you keep pace with inflation. However, if your investments underperform, your payments may be smaller.

Most variable annuities include a standard death benefit that protects your beneficiaries if you pass away before withdrawing your funds.

Best for: Investors comfortable with market risk who want the potential for higher returns and the option to structure guarantees through riders.

Fixed Index Annuities

Fixed index annuities (FIAs) are hybrid products that combine the best features of fixed and variable annuities. Your returns are linked to the performance of a market index (like the S&P 500), but your principal is protected from market losses. This means you can benefit from market gains while avoiding the downside risk of a market crash.

Fixed index annuities typically provide a guaranteed minimum interest rate combined with growth potential tied to index performance. This makes them attractive for people who want market-based growth with guardrails.

Best for: Those seeking growth potential with downside protection and the ability to earn higher returns than fixed annuities.

Key Advantages of Annuities for Retirement

- Guaranteed income: Annuities provide predictable income payments you can count on, reducing the risk of outliving your savings.

- Tax-deferred growth: With deferred annuities, your money grows without annual tax consequences until you begin withdrawals.

- Principal protection: Fixed and fixed index annuities protect your initial investment, making them suitable for conservative retirement planning.

- Customizable payout options: You can choose to receive payments for a specific period or for life, and some options include survivor benefits for your spouse or beneficiaries.

- Inflation protection potential: Variable annuities can increase payments over time, potentially keeping pace with inflation.

- Death benefits: Many annuities include guarantees that protect your beneficiaries.

Important Considerations Before Buying

While annuities offer valuable benefits, they're not right for everyone. Here are critical factors to evaluate:

- Surrender charges: Most annuities have surrender schedules—fees you'll pay if you withdraw money during the early years of the contract. Understand these terms before committing.

- Fees and complexity: Variable annuities can involve multiple fees, including management fees and rider costs, which can reduce your returns.

- Liquidity: Annuities are long-term commitments. If you need immediate access to your money, the surrender charges may make annuities expensive.

- Irrevocable income tradeoff: Once you begin receiving income from an immediate annuity, you can't reverse that decision. Choose your payout options carefully.

- Inflation planning: Fixed annuities provide predictable income, but that income doesn't increase with inflation. Consider whether this meets your long-term needs.

- Complexity: Some annuities, particularly variable annuities with multiple riders, can be complex. Make sure you fully understand what you're purchasing.

Is an Annuity Right for You?

Deciding whether to buy an annuity depends on your personal situation. Consider an annuity if you:

- Want guaranteed income you can't outlive

- Prefer predictable, stable retirement income over investment growth

- Have a significant lump sum to invest (from a pension payout, inheritance, or retirement savings)

- Want to reduce your investment risk as you approach or enter retirement

- Are concerned about market volatility affecting your retirement income

- Want to create an income "floor" that covers essential expenses

You might want to reconsider if you:

- Need frequent access to your money

- Are uncomfortable with the long-term commitment and surrender charges

- Prefer maximum flexibility and control over your investments

- Have a short life expectancy (annuities work best for longer-living individuals)

- Already have sufficient guaranteed income from Social Security and pensions

Next Steps: Getting Started with Annuities

If you're considering an annuity as part of your retirement strategy, here's what to do:

- Assess your retirement income needs. Calculate how much guaranteed income you'll need from Social Security, pensions, and other sources. An annuity can fill any gap.

- Determine your risk tolerance. Are you comfortable with market fluctuations, or do you prefer guaranteed returns? This will guide your choice between fixed, variable, and fixed index annuities.

- Get quotes from multiple insurers. Compare rates, fees, and terms from several insurance companies. Rates vary significantly.

- Review the fine print. Understand surrender charges, payout options, and any riders (additional features) you're considering.

- Consult a financial advisor. A qualified financial professional can help you determine if an annuity fits your overall retirement plan and ensure you're getting a fair deal.

- Consider your overall strategy. Annuities work best as part of a diversified retirement income plan, not as your only investment.

Annuities aren't a one-size-fits-all solution, but for many Americans, they're a valuable tool for creating reliable, predictable retirement income. By understanding the different types available and carefully evaluating your personal situation, you can determine whether an annuity belongs in your retirement portfolio.

Frequently Asked Questions

Sources & References

-

1

What is an annuity? Understanding the basics — Ameriprise Financial — www.ameriprise.com

-

2

Annuity Basics — Insured Retirement Institute (IRI) — www.irionline.org

-

3

Types of Annuities Explained: Evaluating Retirement Income Options — Bankers Life — www.bankerslife.com

-

4

Annuities Explained: Types, Benefits, & How They Work — Guardian Life — www.guardianlife.com

-

5

What are the Different Types of Annuities? — Equifax — www.equifax.com

-

6

Annuities — 2026 Retirement income option and quotes — Blake Insurance Group — blakeinsurancegroup.com

-

7

Annuities — Investor.gov — www.investor.gov

-

8

What are annuities and how do they work? — Fidelity Investments — www.fidelity.com

Useful Tools

Related Articles

What Is a Self-Directed IRA and What Can You Invest In?

Imagine unlocking a retirement account that lets you invest in rental properties, precious metals, or even cryptocurrency—all while enjoying the same tax advantages as a traditional IRA. That's the po...

How to Protect Your Assets Before You Need Nursing Home Care

Imagine working a lifetime to build your nest egg, only to watch it vanish paying for nursing home care. In the United States, the average cost of a private room in a nursing home exceeds $100,000 per...

What Is a Gold IRA and Is It a Good Investment?

If you're looking to diversify your retirement portfolio beyond traditional stocks and bonds, a gold IRA might be worth considering. This self-directed retirement account allows you to hold physical p...

Best Online Brokers for Beginner Investors in the USA

Starting your investing journey doesn't have to be overwhelming. With the right online broker, you can build wealth through stocks, ETFs, and more—without hidden fees or complex tools holding you back...