How to Protect Your Assets Before You Need Nursing Home Care

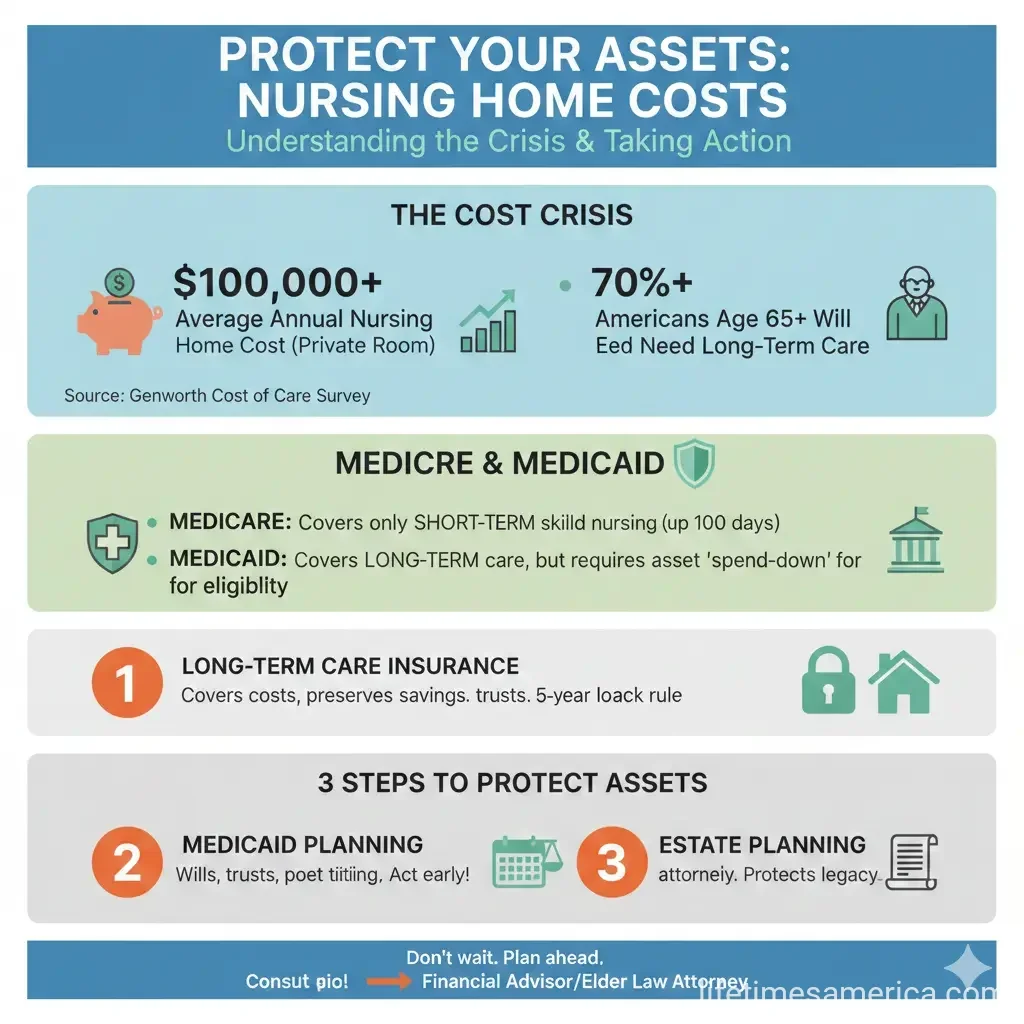

Imagine working a lifetime to build your nest egg, only to watch it vanish paying for nursing home care. In the United States, the average cost of a private room in a nursing home exceeds $100,000 per...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine working a lifetime to build your nest egg, only to watch it vanish paying for nursing home care. In the United States, the average cost of a private room in a nursing home exceeds $100,000 per year in 2026, forcing many families to deplete their savings or turn to Medicaid. But you don't have to lose everything—proactive planning lets you protect your assets while ensuring quality care.

Whether you're planning for yourself, your parents, or a spouse, understanding Medicaid rules, trusts, and insurance options is key. This guide breaks down proven strategies tailored for Americans, drawing on current 2026 regulations like Medicaid's 60-month look-back period. Start planning today to safeguard your wealth and legacy.

Understanding the Nursing Home Cost Crisis

Nursing home expenses can drain retirement savings quickly. In high-cost states like Massachusetts, annual costs top $200,000, while even in Florida, monthly fees exceed $9,000. Medicaid, a joint federal-state program, covers long-term care for eligible low-income individuals, but strict asset limits apply—typically $2,000 for a single applicant.

Medicaid's 60-month look-back period reviews all asset transfers five years before your application. Improper gifts or sales can trigger penalties, delaying eligibility. Spousal protections help, too: the Community Spouse Resource Allowance (CSRA) lets the at-home spouse keep up to about $154,000 in assets in 2026, varying by state.

Why Assets Are at Risk

- Medicaid estate recovery: After death, states can claim assets like your home to recoup costs.

- No spend-down loopholes: You must qualify by reducing countable assets legally.

- Rising costs: Long-term care inflation outpaces Social Security adjustments.

Without planning, families face tough choices: pay privately, impoverish one spouse, or risk denial of care.

Key Strategies to Protect Your Assets

Effective protection combines legal tools, insurance, and timely action. Consult an elder law attorney early—state rules differ, and mistakes are costly.

1. Medicaid Asset Protection Trusts (MAPTs)

A Medicaid Asset Protection Trust (MAPT) is an irrevocable trust that removes assets from your countable estate after the 60-month look-back. Transfer your home, savings, or investments into the trust; you lose direct control but can often retain income or use rights.

- Protects the family home via life estates or full transfers.

- Shields assets for heirs, bypassing probate and recovery.

- Best for middle-income families ($100,000–$1M in assets).

Pro tip: Set it up at least five years before needing care. In Florida, pair it with the Homestead Exemption for extra home protection.

2. Spousal Protections and Transfers

If married, leverage Medicaid's spousal impoverishment rules. The community spouse keeps the CSRA (up to $154,000 in 2026) plus a home and car. Transfer assets to the healthy spouse legally, outside the look-back.

Other transfers include:

- Gifting to children or trusts—five years early to avoid penalties.

- Medicaid-compliant annuities: Convert lump sums to income streams that don't count as assets.

- Life estate deeds: Keep living in your home while deeding it to heirs.

3. Spend Down on Exempt Assets

Reduce countable resources legally by buying exempt items:

- Prepaid funeral or burial plans.

- Home modifications or repairs.

- A new vehicle or personal items.

- Debt payoff (mortgage, medical bills).

These don't trigger penalties and preserve lifestyle.

4. Long-Term Care Insurance

Buy a policy early to cover costs privately, avoiding Medicaid altogether. Policies pay for home care, assisted living, or nursing homes. Combine with trusts for hybrid protection—but check if it affects low-income Medicaid eligibility.

| Strategy | Potential Benefit | Key Drawback | Look-Back Impact |

|---|---|---|---|

| Irrevocable MAPT | Shields assets for heirs after 5 years | Loss of control | 60 months |

| Spousal Protections | Community spouse keeps higher assets | State-specific limits | Varies |

| Annuities/Life Estates | Retain income/home use | Complex rules | 60 months |

| LTC Insurance | Covers costs privately | Premium costs | None |

5. Caregiver Agreements and Powers of Attorney

Pay family caregivers via a formal agreement at fair market value—reduces assets legally. Update powers of attorney and healthcare proxies to control decisions and assets.

State-Specific Considerations

Rules vary: Florida's Homestead Exemption protects unlimited home equity; Massachusetts tightened MassHealth in 2026. Check your state's Medicaid agency via medicaid.gov or usa.gov. Arkansas allows OBRA trusts.

Common Mistakes to Avoid

- DIY transfers: Risk penalties without attorney guidance.

- Last-minute planning: Look-back voids recent moves.

- Ignoring estate recovery: Homes can still be claimed post-death.

- Overlooking insurance details: Some policies disqualify Medicaid.

Next Steps to Secure Your Future

Don't wait for a diagnosis—act now. Inventory your assets, review estate documents, and schedule a free consultation with an elder law attorney. Estimate costs using tools on longtermcare.gov. Pair strategies like a MAPT with insurance for robust protection. Your family's financial security depends on today's choices.

Frequently Asked Questions

Sources & References

-

1

Smart Strategies to Protect Assets from Nursing Homes - seniorsolutionsinfo.com — www.seniorsolutionsinfo.com

-

2

How to Protect Your Assets from Nursing Home Costs - elderlawguidance.com — elderlawguidance.com

- 3

-

4

How to Protect Assets from Long-Term Care - robbinsdimonte.com — robbinsdimonte.com

-

5

Ways to Protect Assets from Medicaid - thechamberlainlawfirm.com — www.thechamberlainlawfirm.com

-

6

Medicaid and Asset Protection Planning in 2026 - jdavenportassociates.com — jdavenportassociates.com

-

7

Don't Lose It All to the Nursing Home - mcclellandfirm.com — mcclellandfirm.com

-

8

How to Protect Your Assets from Nursing Home Costs in 2026 - wny-lawyers.com — www.wny-lawyers.com

-

9

Medicaid Asset Protection Trusts: How They Work - medicaidplanningassistance.org — www.medicaidplanningassistance.org

Related Articles

What Is a Self-Directed IRA and What Can You Invest In?

Imagine unlocking a retirement account that lets you invest in rental properties, precious metals, or even cryptocurrency—all while enjoying the same tax advantages as a traditional IRA. That's the po...

What Is a Gold IRA and Is It a Good Investment?

If you're looking to diversify your retirement portfolio beyond traditional stocks and bonds, a gold IRA might be worth considering. This self-directed retirement account allows you to hold physical p...

Best Online Brokers for Beginner Investors in the USA

Starting your investing journey doesn't have to be overwhelming. With the right online broker, you can build wealth through stocks, ETFs, and more—without hidden fees or complex tools holding you back...

Investment Property Loans: How to Finance a Rental Property

Imagine turning a spare $50,000 into a steady stream of rental income that builds your wealth over time. That's the power of investment property loans—they let you leverage borrowed money to buy renta...