How to Get a Home Equity Line of Credit (HELOC) in 2026

Imagine tapping into your home's value to fund that dream kitchen remodel, pay for college tuition, or consolidate high-interest debt—all without refinancing your entire mortgage. In 2026, a Home Equi...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine tapping into your home's value to fund that dream kitchen remodel, pay for college tuition, or consolidate high-interest debt—all without refinancing your entire mortgage. In 2026, a Home Equity Line of Credit (HELOC) offers flexible, often lower-rate borrowing backed by your home equity, making it a smart choice for many Americans facing rising costs.

With home values holding strong in most markets and average HELOC rates around 7.31% as of February 2026, now's the time to explore if a HELOC fits your financial plans. This guide walks you through every step to get a HELOC in 2026, from eligibility checks to closing the deal, tailored for U.S. homeowners.

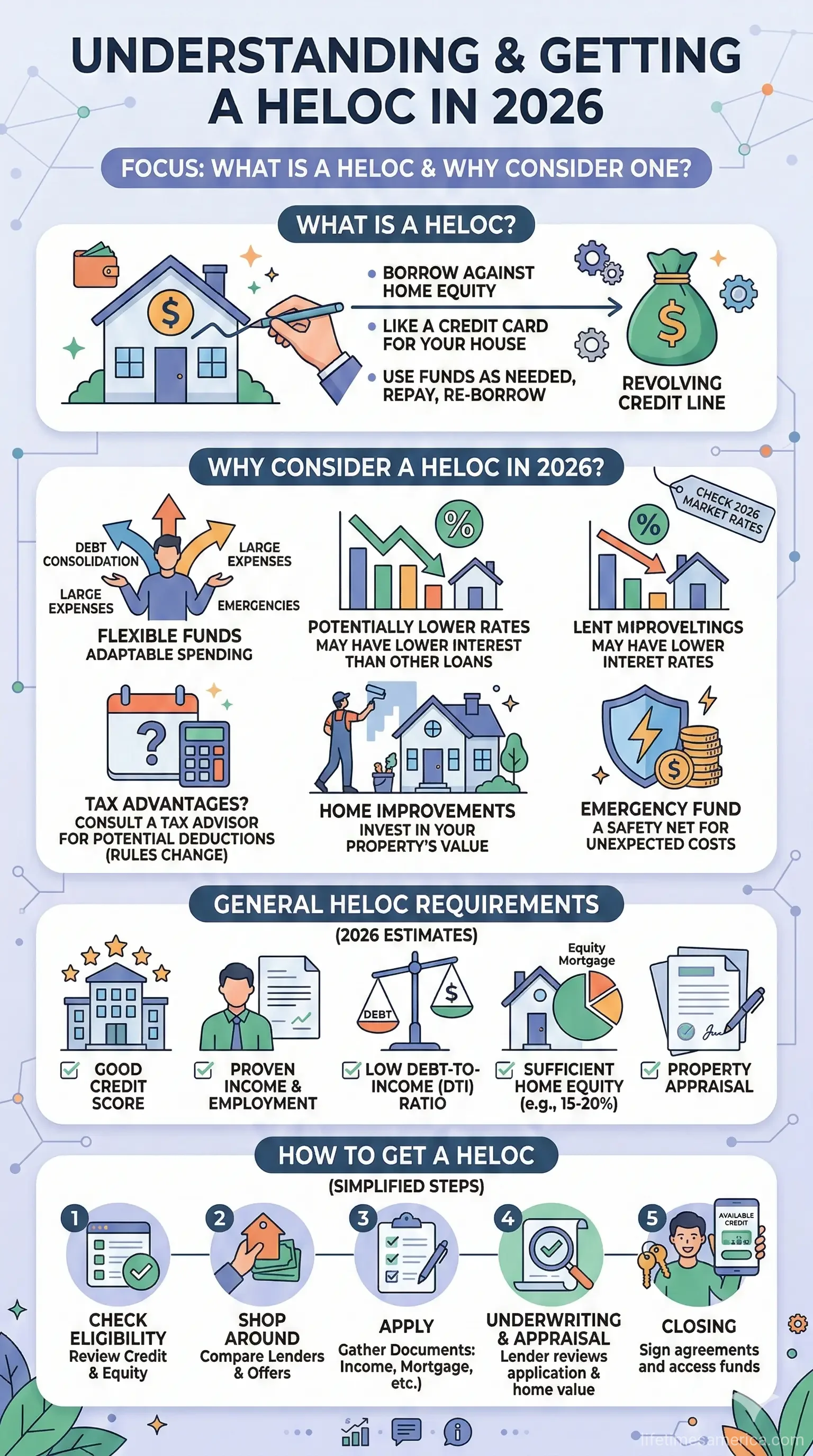

What Is a HELOC and Why Consider One in 2026?

A HELOC functions like a credit card secured by your home's equity. You get a revolving line of credit during a draw period (typically 10 years), where you can borrow as needed up to your limit, often paying interest-only. After that, repayment kicks in over 10-20 years.

In 2026, HELOCs shine for their variable rates tied to the prime rate, which could drop if the Fed cuts rates further. Use them for home improvements (potentially tax-deductible under IRS rules if used for qualifying purposes), debt consolidation, or emergencies. But remember, your home is collateral—if you can't repay, foreclosure is a risk.

HELOC vs. Other Borrowing Options

Compare HELOCs to alternatives to see if it's right for you:

| Option | Collateral Required | Approval Time | Best For |

|---|---|---|---|

| HELOC | Yes (home) | 4-7 weeks | Flexible, ongoing needs |

| Home Equity Loan | Yes (home) | 4-7 weeks | Lump-sum needs |

| Cash-Out Refinance | Yes (home) | 30-60 days | Lower rates on full mortgage |

| Personal Loan | No | 1-5 days | Small, quick amounts |

HELOC Eligibility Requirements in 2026

Lenders evaluate several key factors to approve a HELOC. Meeting these boosts your odds and unlocks better terms.

1. Home Equity: The Foundation

You'll need at least 15-20% equity in your home, calculated as (home value - mortgage balance) / home value. Most lenders cap combined loan-to-value (CLTV) at 80-90%, letting you borrow up to 85% of your home's value minus what you owe.

Example: For a $250,000 home with a $150,000 mortgage, you have $100,000 equity (40%). At 80% CLTV max, you could access up to $50,000 ($250,000 x 0.8 - $150,000). With 50%+ equity, expect higher limits like $50K-$200K+.

- Get a rough estimate via Zillow or Redfin, but lenders require a professional appraisal.

- Primary homes qualify easiest; some allow second homes or investments.

2. Credit Score: Aim High for Best Rates

Minimum scores range from 620-680, but 720+ unlocks top rates and limits. In 2026, scores of 680-719 still qualify widely, though with potential CLTV caps. Check your FICO via AnnualCreditReport.com (free weekly) and improve by paying down debt or fixing errors.

3. Debt-to-Income (DTI) Ratio: Keep It Under 44-45%

DTI = (monthly debts / gross monthly income) x 100. Lenders want it below 44-45%, including estimated HELOC payments. No universal income minimum—focus on stable employment and proof like W-2s or tax returns.

4. Other Requirements

- Income/Employment Proof: Pay stubs, tax returns.

- Appraisal & Insurance: Lender-ordered appraisal; proof of homeowners (and flood insurance if in a flood zone).

- Property Type: Best for owner-occupied; restrictions in states like TX/FL/GA.

Step-by-Step: How to Get a HELOC in 2026

Follow these actionable steps to secure your HELOC efficiently.

Step 1: Check Your Eligibility at Home

- Calculate equity using online tools or recent statements.

- Pull your credit report from Experian, Equifax, TransUnion.

- Compute DTI: List debts (mortgage, car, cards) vs. income.

Step 2: Shop and Compare Lenders

Compare banks, credit unions, and online lenders like Rocket Mortgage or local options. Look at rates (avg. 7.31%), fees, draw periods, and CLTV. Prequalify without a hard credit pull—many offer online calculators.

| Lender Example | Min. Line | Draw/Repay | Sample Rate (Feb 2026) |

|---|---|---|---|

| National Average | $25,000+ | 10/20 years | 7.31% |

| Sample Lender A | $25,000 | 10/20 years | 6.59% |

| Sample Lender B | Up to $1M | 10/20 years | 6.75% (intro 5.99%) |

Step 3: Submit Your Application

Provide: ID, income docs, mortgage info, home details. Authorize credit check and appraisal (costs $300-500, often lender-paid). Approval takes 30-45 days.

Step 4: Underwriting and Closing

Underwriters verify everything. If approved, review terms, sign docs (notary may visit), and funds become available. Closing fees: 0-2% of line.

Costs, Rates, and Tax Perks in 2026

Expect variable rates (prime + margin), annual fees ($50-75), and closing costs. Interest may be IRS-deductible for home improvements—consult a tax pro or IRS Publication 936. Shop for no-fee options to save.

Pros and Cons of a HELOC

- Pros: Flexible access, lower rates than cards, interest-only payments initially.

- Cons: Variable rates can rise, home at risk, not ideal for short-term needs.

Next Steps to Secure Your HELOC

Start today: Check your equity and credit, then prequalify with 3 lenders. Gather docs early to speed things up. If rates drop, lock in a fixed-rate option during the draw period. For personalized advice, visit ConsumerFinancialProtectionBureau.gov or consult a HUD-approved counselor. With smart planning, your HELOC can fuel your 2026 goals without breaking the bank.

Frequently Asked Questions

Sources & References

-

1

What You Need to Know About HELOCs in 2026 - Experian — www.experian.com

-

2

HELOC Requirements, 2026: What You Need to Know - Freedom Mortgage — www.freedommortgage.com

-

3

How To Get A Home Equity Line Of Credit (HELOC) - CU SoCal — www.cusocal.org

-

4

How Much HELOC Can You Qualify For in 2026? Rates, Limits - ReAlpha — www.realpha.com

-

5

2026 HELOC and Home Equity Loan Requirements - Rate — www.rate.com

-

6

Home Equity Line of Credit Guide 2026 - Meadowbrook — mfmbankers.com

- 7

Related Articles

Buying Your First Home in 2026: FHA vs. Conventional Loans

Imagine standing in front of your dream home in 2026, keys in hand, finally owning a piece of the American dream. For first-time buyers, choosing between an FHA loan and a conventional loan can make o...

Is a 15-Year or 30-Year Mortgage Better for Your Long-Term Wealth?

Choosing between a 15-year and 30-year mortgage is one of the biggest financial decisions you'll make as a homeowner. While both options have their place, the right choice depends on your income, fina...

The Ultimate Guide to VA Loans for Veterans and Active Duty

Imagine owning your dream home without scraping together a down payment or worrying about private mortgage insurance—that's the power of a VA loan for veterans and active duty service members. Backed...

How to Buy a House with a Low Credit Score

Buying a home with a low credit score is challenging but absolutely possible in 2026. Whether you're working with a score below 580 or rebuilding after financial difficulties, there are government-bac...