Is a 15-Year or 30-Year Mortgage Better for Your Long-Term Wealth?

Choosing between a 15-year and 30-year mortgage is one of the biggest financial decisions you'll make as a homeowner. While both options have their place, the right choice depends on your income, fina...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Choosing between a 15-year and 30-year mortgage is one of the biggest financial decisions you'll make as a homeowner. While both options have their place, the right choice depends on your income, financial goals, and long-term wealth strategy. Let's break down the real numbers and help you decide which path aligns with your future.

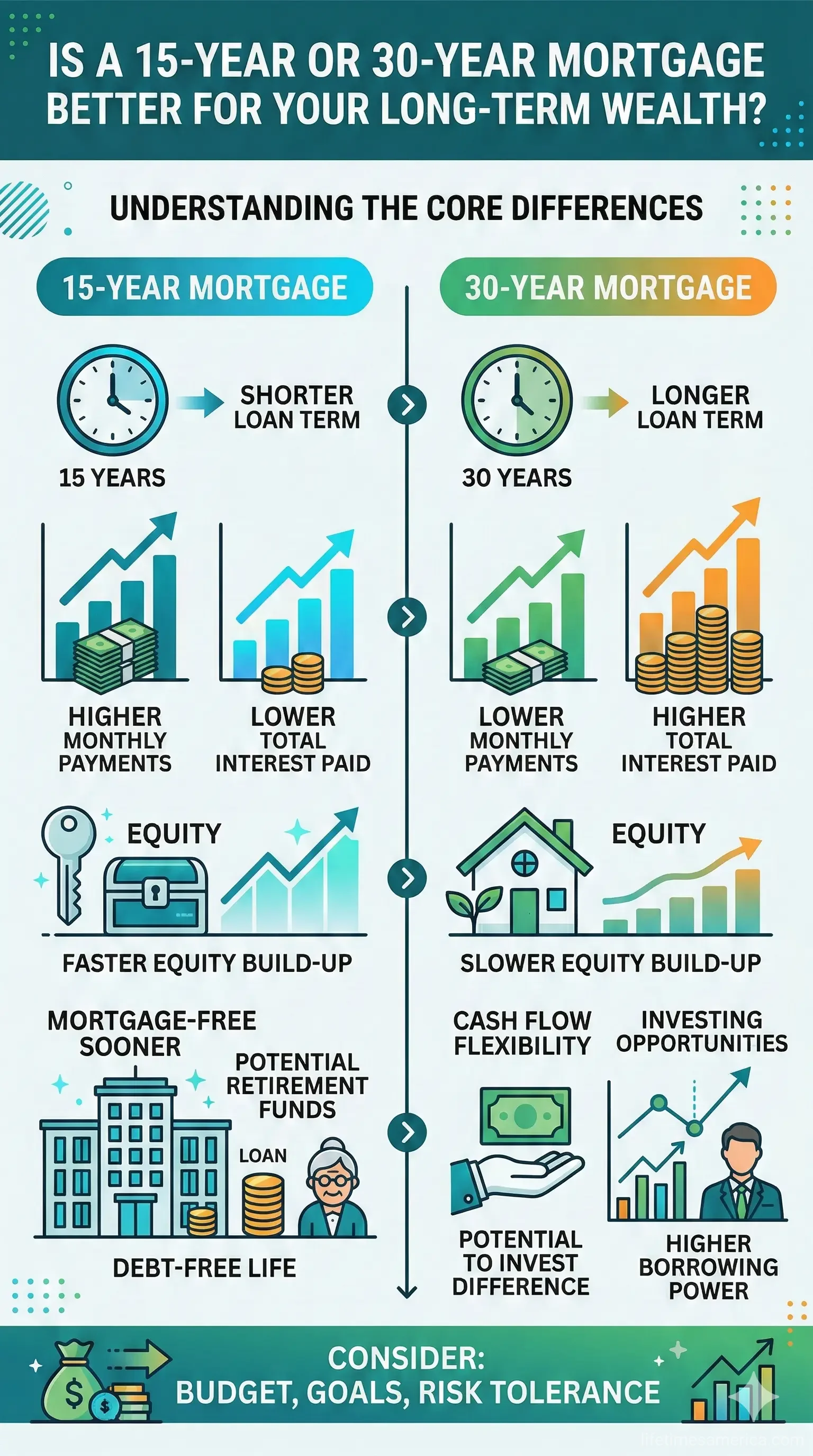

Understanding the Core Differences

The fundamental difference between these two mortgage types comes down to how you spread your payments over time. A 15-year mortgage requires you to pay off your home loan in half the time of a 30-year mortgage, which means higher monthly payments but significantly less interest paid overall. A 30-year mortgage stretches your payments across three decades, lowering your monthly obligation but increasing the total interest you'll pay.

Currently, as of February 2026, the average interest rate on a 30-year fixed-rate mortgage is 5.86% APR, while 15-year mortgages average 5.42% APR. Notice that 15-year mortgages typically carry lower interest rates—a benefit that compounds your savings over time.

The Monthly Payment Reality

Let's look at concrete numbers. If you're financing $240,000 (after a 20% down payment on a $300,000 home), here's what you're looking at:

With a 15-year mortgage, your monthly payments will be significantly higher than a 30-year loan. The exact amount depends on current interest rates, but the trade-off is clear: you're paying more each month to own your home faster. A 30-year mortgage, by contrast, offers lower monthly payments because you're spreading the repayment over twice as much time, giving you more flexibility in your monthly budget.

For example, one recent calculation showed that a 15-year mortgage costs $466 more per month than a 30-year loan, but saves you $98,526 in total interest. That's a substantial difference over the life of your loan.

Interest Costs: Where the Real Money Matters

Here's where the 15-year mortgage shines for long-term wealth building. 30-year mortgages cost significantly more in total interest because you're paying interest for twice as long. In your first few years of a 30-year mortgage, most of your payments go toward interest rather than building equity in your home.

The numbers are striking: you'll typically spend tens of thousands of dollars more over the life of a 30-year loan compared to a 15-year loan. That money could otherwise go toward retirement savings, investments, or other wealth-building strategies.

The longer loan term also means more time for interest to accrue on your debt. Even a small difference in interest rates compounds dramatically over 30 years versus 15 years.

Which Mortgage Fits Your Financial Situation?

Choose a 15-Year Mortgage If:

- You want to pay off your home faster and own it outright before retirement

- You have a stable, comfortable income that can handle higher monthly payments

- You want to take advantage of lower interest rates typically offered on 15-year terms

- You're prioritizing wealth building through home equity rather than monthly cash flow flexibility

- You're in your 40s or younger and have decades to benefit from the savings

Choose a 30-Year Mortgage If:

- You need lower monthly payments to fit your budget comfortably

- You want more breathing room in your monthly finances

- You'd rather free up funds for investments, retirement accounts (like your 401(k)), or other savings goals

- You're concerned about job security or have variable income

- You're a first-time homebuyer and want to keep your housing costs manageable

The Wealth-Building Perspective

For long-term wealth, the math often favors the 15-year mortgage—but only if you can afford the payments without sacrificing other financial goals. Here's why:

Building home equity faster: With a 15-year mortgage, you're building ownership in your most valuable asset much quicker. By your mid-50s or early 60s, your home could be paid off, eliminating a major expense in retirement.

Interest savings compound: That $98,000+ in interest savings isn't just a number—it's money that stays in your pocket. Invested wisely, that could grow substantially over time.

Flexibility in later years: Imagine reaching retirement with your home paid off. Your Social Security and other retirement income go much further when you don't have a mortgage payment.

However, the 30-year mortgage also has wealth-building merit. If you invest the difference between a 15-year and 30-year payment into a diversified portfolio earning 7-8% annually, you might actually come out ahead financially. This strategy assumes discipline—you must actually invest that money rather than spend it.

Tax Considerations and Deductions

One often-overlooked factor: mortgage interest deductions. You can deduct mortgage interest on loans up to $750,000 if you're filing jointly (or $375,000 if married filing separately). A 30-year mortgage means more years of deductible interest, though this benefit decreases over time as more of your payment goes toward principal.

That said, with the current standard deduction being substantial, many Americans don't itemize deductions anyway, so this shouldn't be your primary decision driver.

Real-World Scenarios for 2026

Scenario 1: The Stable Earner You're 35, earning $100,000 annually, and have a strong emergency fund. A 15-year mortgage aligns with your goal to retire at 65 with your home paid off. Yes, the payments are higher, but they're manageable, and you'll sleep better knowing you're building wealth aggressively.

Scenario 2: The Young Family You're 28, just had your first child, and your spouse is considering part-time work. A 30-year mortgage gives you breathing room during these expensive years. You can invest in your children's education funds and your 401(k) while keeping housing costs manageable. You can always pay extra toward principal in higher-earning years.

Scenario 3: The Late-Start Buyer You're 50 and buying your first home. A 15-year mortgage means you'll own it by 65, perfect for retirement. A 30-year mortgage would mean mortgage payments well into your 80s—likely not ideal unless you plan to downsize later.

Making Your Decision

The "better" mortgage isn't universal—it's personal. Ask yourself these questions:

- Can I comfortably afford a 15-year payment without sacrificing retirement savings or emergency funds?

- Do I plan to stay in this home for at least 10-15 years?

- What's my timeline for retirement, and when do I want to own my home outright?

- Would I invest the payment difference from a 30-year mortgage, or would I spend it?

For most Americans focused on long-term wealth building, the 15-year mortgage wins on paper—you'll pay less interest and own your home faster. But the 30-year mortgage wins in practice if it allows you to maximize retirement contributions, build an emergency fund, and invest in other growth opportunities.

The best mortgage is the one you can afford without stress, that aligns with your retirement timeline, and that supports your overall financial strategy. Consider speaking with a mortgage professional who can run specific numbers for your situation, and don't let interest rates alone drive your decision. Your financial peace of mind matters more than saving a few thousand dollars in interest.

Frequently Asked Questions

Sources & References

-

1

15-year vs. 30-year mortgage comparison - Rocket Mortgage — www.rocketmortgage.com

-

2

15- vs. 30-year mortgage calculator | Which is better? - U.S. Bank — www.usbank.com

-

3

15-Year vs. 30-Year Mortgage Calculator | Landmark Credit Union — landmarkcu.com

-

4

15-Year vs. 30-Year Term Mortgage Calculator - Freddie Mac — myhome.freddiemac.com

-

5

Mortgage Comparison - 15 Years vs. 30 Years - Tech CU — www.techcu.com

-

6

Compare Today's Mortgage Rates | NerdWallet — www.nerdwallet.com

Related Articles

Buying Your First Home in 2026: FHA vs. Conventional Loans

Imagine standing in front of your dream home in 2026, keys in hand, finally owning a piece of the American dream. For first-time buyers, choosing between an FHA loan and a conventional loan can make o...

How to Get a Home Equity Line of Credit (HELOC) in 2026

Imagine tapping into your home's value to fund that dream kitchen remodel, pay for college tuition, or consolidate high-interest debt—all without refinancing your entire mortgage. In 2026, a Home Equi...

The Ultimate Guide to VA Loans for Veterans and Active Duty

Imagine owning your dream home without scraping together a down payment or worrying about private mortgage insurance—that's the power of a VA loan for veterans and active duty service members. Backed...

How to Buy a House with a Low Credit Score

Buying a home with a low credit score is challenging but absolutely possible in 2026. Whether you're working with a score below 580 or rebuilding after financial difficulties, there are government-bac...