Buying Your First Home in 2026: FHA vs. Conventional Loans

Imagine standing in front of your dream home in 2026, keys in hand, finally owning a piece of the American dream. For first-time buyers, choosing between an FHA loan and a conventional loan can make o...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine standing in front of your dream home in 2026, keys in hand, finally owning a piece of the American dream. For first-time buyers, choosing between an FHA loan and a conventional loan can make or break that moment. With housing markets evolving and rates shifting, understanding these options helps you save thousands and secure the best deal.

This guide breaks down everything you need to know about buying your first home in 2026: FHA vs. conventional loans, from down payments to long-term costs, tailored for Americans navigating today's economy.

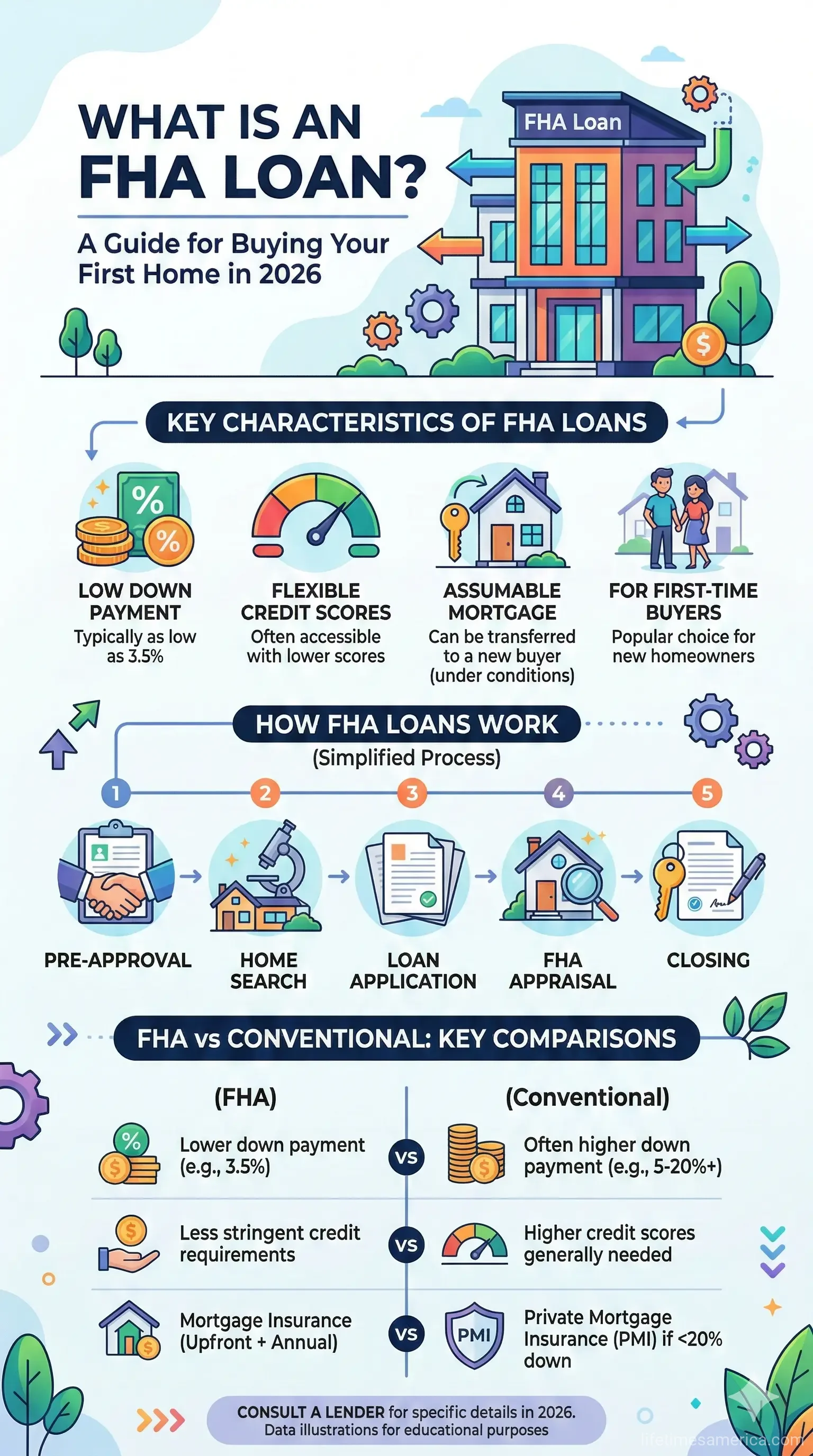

What Is an FHA Loan?

FHA loans, backed by the Federal Housing Administration, make homeownership accessible for first-time buyers with modest savings or credit challenges. They're government-insured, so lenders take less risk, offering flexible terms.

Key FHA Loan Requirements in 2026

- Credit score: As low as 580 with 3.5% down, or 500 with 10% down.

- Down payment: Minimum 3.5% of the purchase price.

- Debt-to-income (DTI) ratio: Up to 56.9% in some cases, higher than conventional limits.

- Loan limits: Vary by county; check HUD's site for 2026 updates via usa.gov.

- Mortgage insurance: Required for the life of the loan unless you refinance.

For example, on a $300,000 home, you'd need just $10,500 down—ideal if you're saving while paying off student loans.

What Is a Conventional Loan?

Conventional loans are private mortgages not backed by the government, offered through banks like PNC or Fannie Mae/Freddie Mac programs. They suit buyers with stronger credit and suit those planning long-term ownership.

Key Conventional Loan Requirements in 2026

- Credit score: Typically 620 or higher; 680+ unlocks better rates.

- Down payment: As low as 3% for first-time buyers via programs like HomeReady or Home Possible.

- DTI ratio: Usually up to 43%.

- Reserve requirements: 2-6 months of payments, higher than FHA.

- Private mortgage insurance (PMI): Only if under 20% down; cancellable once you reach 20% equity.

On that same $300,000 home, a conventional loan might require $9,000 down, beating FHA slightly upfront.

FHA vs. Conventional Loans: Side-by-Side Comparison

Here's how they stack up for first-time buyers in 2026:

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Credit Score | 580 (3.5% down) or 500 (10% down) | 620+ |

| Minimum Down Payment | 3.5% | 3% (first-time buyers) |

| DTI Ratio | Up to 56.9% | Up to 43% |

| Mortgage Insurance | Lifelong (unless refinance) | PMI if <20% down; cancellable |

| Interest Rates | Often higher; government-backed | Competitive for strong credit |

| Best For | Lower credit, high DTI, limited reserves | Good credit, 20%+ down, long-term savings |

Down Payment: FHA vs. Conventional Breakdown

Down payments are a top concern for first-timers. FHA's 3.5% feels low, but conventional's 3% edges it out for qualified buyers. On a $200,000 home in places like Northeast Ohio:

- FHA: $7,000 down.

- Conventional: $6,000 down.

FHA allows gifts or seller concessions up to 6% for closing costs. Conventional shines with 20% down—no PMI, potentially saving $100+ monthly.

Real-World Example

Buying a $350,000 home in 2026? FHA down payment: $12,250. Conventional 97: $10,500. But factor in FHA's lifelong MIP (about 0.55% annually) vs. conventional PMI (0.5-1%, dropping off). Over 10 years, conventional could save $5,000+ if you build equity fast.

Credit Scores and Qualification: Who Qualifies Easier?

FHA wins for credit-challenged buyers—qualify at 580 vs. conventional's 620. If your score is 700+, conventional rates drop, and PMI vanishes sooner.

DTI tells another story: FHA's flexibility (e.g., $2,845 monthly debt on $60K income) beats conventional's $2,500 limit. Recent grads with loans? FHA might be your ticket.

Mortgage Insurance and Long-Term Costs

FHA requires upfront and annual MIP forever (unless refinanced). Conventional PMI ends at 20% equity—key for 2026's rising home values.

"Conventional loans usually offer cheaper mortgage insurance over time, but FHA loans provide more flexible qualification standards upfront."

Run numbers: For strong-credit buyers, conventional saves long-term. Use IRS tools or bls.gov salary data to model your scenario.

Pros and Cons for First-Time Buyers

FHA Pros

- Lower credit barriers.

- Higher DTI allowance.

- Lower reserves (1-2 months).

- Seller paid closing costs up to 6%.

FHA Cons

- Lifelong insurance.

- Property condition rules (no major fixes).

- Loan limits cap pricier areas.

Conventional Pros

- PMI cancellable.

- Flexible property types (second homes, investments).

- Better rates for high credit.

Conventional Cons

- Stricter credit/DTI.

- Higher reserves.

- Less gift fund flexibility.

Interest Rates and Closing Costs in 2026

Rates fluctuate, but FHA often runs slightly higher due to insurance; conventional competes better for 680+ scores. Expect 6-7% averages per recent trends—shop lenders via usa.gov's marketplace.

Closing costs: 2-5% of loan. FHA allows more seller help; conventional may require more cash reserves.

Which Loan Is Right for You in 2026?

Got credit under 620 or high debt? Go FHA. Strong profile and 10%+ saved? Conventional saves money long-term. Use this quiz:

- Credit <620? FHA.

- DTI >43%? FHA.

- Plan 20% down? Conventional.

- Buying investment later? Conventional.

In competitive markets, conventional homes appeal more to sellers.

Next Steps to Buy Your First Home

1. Check credit via AnnualCreditReport.com (free weekly).

2. Get pre-approved—contact lenders for 2026 rates.

3. Use HUD's affordability calculator at usa.gov.

4. Explore down payment assistance via irs.gov or state housing agencies.

5. Compare quotes from 3+ lenders.

Ready to decide? Pull your numbers today—homeownership in 2026 is within reach.

Frequently Asked Questions

Sources & References

-

1

Deciding Between FHA vs Conventional Loans in 2026 — www.treadstonemortgage.com

-

2

FHA vs. Conventional Loans in 2026: Comparing Key Differences — www.amerisave.com

-

3

FHA vs Conventional Loan | 2026 Rates & Differences — themortgagereports.com

-

4

FHA Vs Conventional Loans in Northeast Ohio (2026) — www.neohomepros.com

-

5

FHA vs. Conventional Loans: Which is Right for You in 2026? — altitudehomeloans.com

-

6

FHA vs. Conventional Loan: Which Is Better for You in 2026? (Video) — www.youtube.com

-

7

FHA vs. Conventional Loan: What Homebuyers Should Know — www.pnc.com

-

8

FHA Loan Requirements for 2026 - Compass Mortgage — www.compmort.com

-

9

Loan Guidelines Comparison: FHA vs. Conventional — www.fha.com

Related Articles

How to Get a Home Equity Line of Credit (HELOC) in 2026

Imagine tapping into your home's value to fund that dream kitchen remodel, pay for college tuition, or consolidate high-interest debt—all without refinancing your entire mortgage. In 2026, a Home Equi...

Is a 15-Year or 30-Year Mortgage Better for Your Long-Term Wealth?

Choosing between a 15-year and 30-year mortgage is one of the biggest financial decisions you'll make as a homeowner. While both options have their place, the right choice depends on your income, fina...

The Ultimate Guide to VA Loans for Veterans and Active Duty

Imagine owning your dream home without scraping together a down payment or worrying about private mortgage insurance—that's the power of a VA loan for veterans and active duty service members. Backed...

How to Buy a House with a Low Credit Score

Buying a home with a low credit score is challenging but absolutely possible in 2026. Whether you're working with a score below 580 or rebuilding after financial difficulties, there are government-bac...