What Is PMI (Private Mortgage Insurance) and How Do You Avoid It?

Buying your first home is exciting, but those extra mortgage costs can quickly dampen the thrill. If you've heard whispers about Private Mortgage Insurance (PMI) sneaking into your monthly payments, y...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Buying your first home is exciting, but those extra mortgage costs can quickly dampen the thrill. If you've heard whispers about Private Mortgage Insurance (PMI) sneaking into your monthly payments, you're not alone—it's a common hurdle for many Americans chasing the dream of homeownership without a hefty down payment.

This guide breaks down exactly what PMI is, why lenders demand it, how much it stings your wallet, and—most importantly—practical strategies to dodge it entirely, even in 2026's competitive housing market.

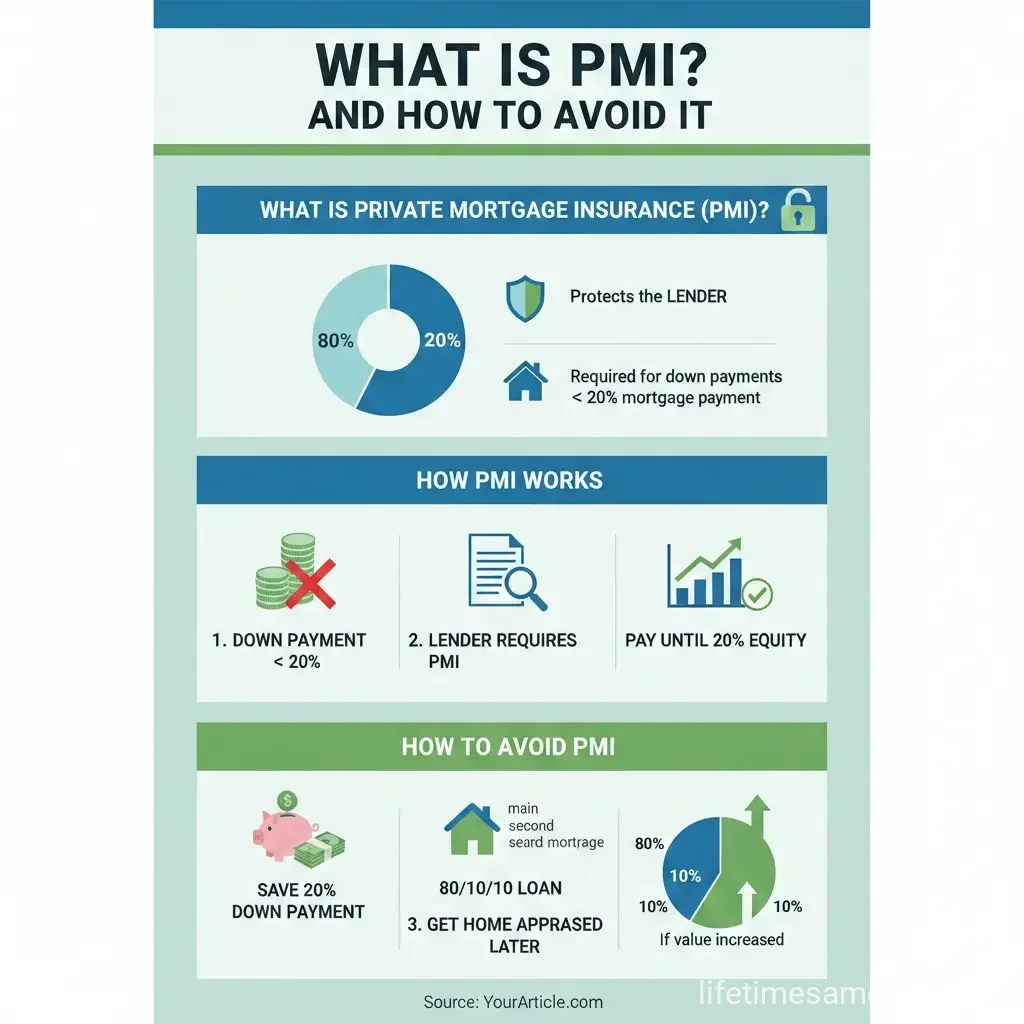

What Is Private Mortgage Insurance (PMI)?

Private Mortgage Insurance (PMI) is a policy that protects the lender, not you, if you default on your home loan and the foreclosure sale doesn't cover the full amount owed. Lenders require it on conventional mortgages when your down payment is less than 20% of the home's purchase price, or if you have under 20% equity during a refinance.

Think of PMI as the lender's safety net. It reimburses them for losses (like the mortgage balance plus foreclosure costs) if you stop payments. But here's the kicker: it doesn't shield you from foreclosure or credit damage—it's purely for their benefit.

PMI vs. Other Mortgage Insurance Types

Don't confuse PMI with similar-sounding protections. PMI applies only to conventional loans (not government-backed ones). Compare it side-by-side:

| Type | Applies To | Key Features | Removal |

|---|---|---|---|

| PMI | Conventional loans | Protects lender; required under 20% down | Cancellable at 80% LTV; automatic at 78% |

| MIP (Mortgage Insurance Premium) | FHA loans | Upfront 1.75% + annual fee (0.15%-0.75%); protects FHA | Lifelong or 11 years (if >10% down); refinance to remove |

| Lender-Paid MI (LPMI) | Conventional | Lender pays, but hikes your rate | Tied to loan life |

PMI also differs from homeowners insurance, which protects your property and belongings from damage—not lender defaults.

How Does PMI Work on Your Mortgage?

When you close on a home with less than 20% down, PMI kicks in immediately. It's typically bundled into your monthly escrow payment alongside principal, interest, taxes, and insurance (PITI).

Your lender arranges the policy through private insurers, but you foot the bill. Payments continue until you hit 20% equity, measured by the loan-to-value (LTV) ratio: LTV = (Loan Balance / Home Value) x 100. At 80% LTV or below, you can request cancellation; it drops off automatically at 78%.

How Is PMI Calculated?

Lenders base your rate on credit score, down payment, LTV, and loan type. Rates range from 0.30% to 1.15% annually of the loan balance in 2026, divided monthly.

Formula: Monthly PMI = (Loan Amount × Annual PMI Rate) ÷ 12

Example: For a $300,000 home with 10% down ($270,000 loan) and 0.8% PMI rate:

- Annual PMI: $270,000 × 0.008 = $2,160

- Monthly: $2,160 ÷ 12 = $180

Lower credit scores or smaller down payments spike rates up to 1.5%. Check your Loan Estimate and Closing Disclosure for exact figures—PMI appears in projected payments.

PMI Payment Options

- Monthly Premium: Most common; added to mortgage.

- Upfront Premium: One-time at closing (no refund if you refinance early).

- Split Premium: Part upfront, rest monthly.

- Lender-Paid (LPMI): Avoids upfront costs but raises your interest rate permanently.

How Much Does PMI Cost in 2026?

Expect $90 to $210 monthly on a $300,000 home with under 20% down, varying by your profile. Nationally, PMI adds 0.5%-1% to annual housing costs for low-down-payment buyers.

Factors driving costs:

- Credit Score: 760+ gets lowest rates; below 620 pays more.

- Down Payment: 5% down = higher PMI than 15%.

- LTV & Loan Term: Shorter loans or low LTV lower premiums.

- Interest Rates: Market fluctuations indirectly affect via risk.

Pro tip: Shop lenders—rates differ, potentially saving thousands over the loan's life.

How to Avoid PMI: 7 Proven Strategies for Americans

You don't have to pay PMI forever—or at all. Here are actionable ways to sidestep it, tailored to U.S. borrowers in 2026:

1. Put 20% Down Upfront

The golden rule: Save 20% of the purchase price. On a $400,000 home, that's $80,000—no PMI required on conventional loans.

2. Use Low-Down-Payment Alternatives Without PMI

- VA Loans: Zero down, no PMI for eligible veterans/military (check VA eligibility at va.gov).

- USDA Loans: No down payment/PMI in rural areas (usda.gov).

- FHA Loans: 3.5% down, but MIP instead—avoid if planning long-term stay.

3. Piggyback Loans (80-10-10 or 80-15-5)

Finance 80% with a first mortgage, 10-15% second (HELOC), and pay 5-10% cash. Keeps first mortgage LTV under 80%—no PMI.

4. Lender-Paid MI (LPMI)

Lender covers PMI; you get a slightly higher rate (e.g., 0.25% bump). Calculate if it's cheaper long-term.

5. Build Equity Fast and Cancel

Once at 80% LTV, request cancellation in writing (track via annual statements). Automatic at 78%. Extra principal payments accelerate this.

6. Refinance When Eligible

Refi to a conventional loan after reaching 20% equity. Home value appreciation helps—median U.S. homes rose 5% yearly pre-2026.

7. Home Buyer Assistance Programs

State/local grants (hud.gov) boost down payments to 20%. FHA Streamline Refinance later swaps MIP for no-PMI conventional.

Run numbers with a mortgage calculator before deciding—tools at consumerfinance.gov help.

Next Steps to Ditch PMI and Save

Start by pulling your credit report (annualcreditreport.com) and crunching numbers for a 20% down scenario. Talk to three lenders for quotes, explore VA/USDA if eligible, and set up automatic extra payments to hit 20% equity faster. In today's market, skipping PMI could save you $100+ monthly—money better spent on your new home.

Ready to buy? Visit CFPB's owning a home resources or consult a HUD-approved counselor.

Frequently Asked Questions

Sources & References

-

1

Private Mortgage Insurance (PMI) Definition — dictionary.nolo.com

-

2

How to Avoid PMI Without a 20% Down Payment | 2026 — themortgagereports.com

-

3

What is Private Mortgage Insurance (PMI)? - Allstate — www.allstate.com

-

4

What Is PMI? How Private Mortgage Insurance Works - NerdWallet — www.nerdwallet.com

-

5

Understanding Private Mortgage Insurance (PMI) - FHA.com — www.fha.com

-

6

What is private mortgage insurance? - Consumerfinance.gov — www.consumerfinance.gov

Useful Tools

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...