What Is a Mortgage and How Does It Work?

Imagine standing in front of your dream home, keys in hand, but without enough cash to buy it outright. That's where a mortgage steps in—a powerful financial tool that makes homeownership possible for...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine standing in front of your dream home, keys in hand, but without enough cash to buy it outright. That's where a mortgage steps in—a powerful financial tool that makes homeownership possible for millions of Americans every year. Whether you're a first-time buyer or looking to upgrade, understanding what a mortgage is and how it works empowers you to make smart decisions in today's market.

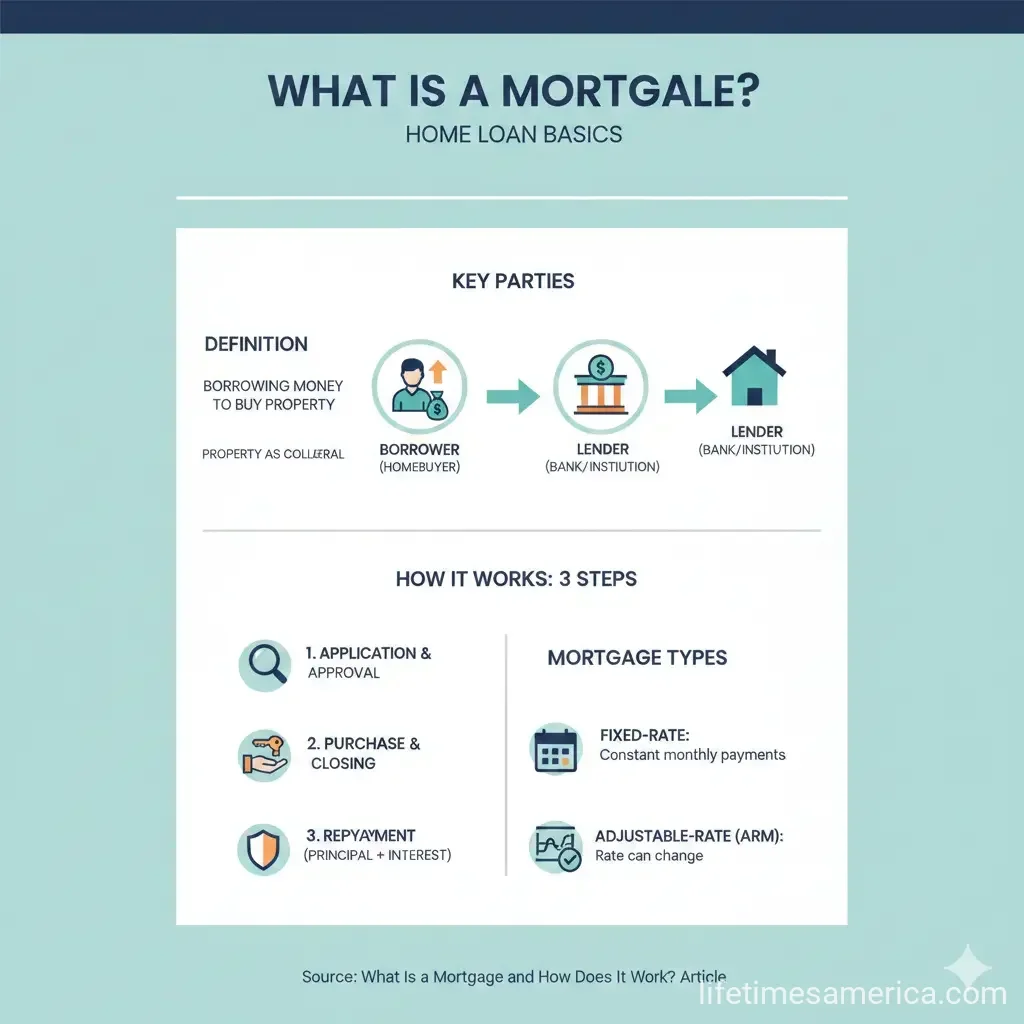

What Is a Mortgage?

A mortgage is a long-term loan specifically designed to help you purchase real estate, such as a single-family home, condo, or duplex. Unlike a personal loan or credit card, the property itself serves as collateral, meaning the lender can claim it if you fail to repay. In legal terms, it's a promissory note—a binding agreement where you, the borrower (also called the mortgagee), promise to repay the lender (the mortgagor) over time, typically 15 or 30 years.

The lender provides the funds to buy the home, and you make regular monthly payments that cover the borrowed amount plus interest. Until the loan is fully repaid, the lender holds the property title, but you get to live there and build equity—your ownership stake—as you pay down the principal. In 2026, with median home prices hovering around $400,000 in many U.S. markets, mortgages remain essential for most buyers.

Key Players in a Mortgage

- Borrower: You or a group (like a couple) who signs the loan and makes payments.

- Lender: Banks, credit unions, or online lenders like Rocket Mortgage that provide the funds.

- Co-signer: Someone with strong credit who agrees to cover payments if you can't—often needed for low credit scores.

- Servicer: The company that collects your payments and manages the escrow account.

How Does a Mortgage Work?

Getting a mortgage involves several steps, from pre-approval to closing. First, you apply and get pre-approved, which shows sellers you're serious and gives you a clear borrowing limit based on your income, credit, and debts. Lenders assess your debt-to-income (DTI) ratio—ideally under 43%—and credit score (aim for 620+ for conventional loans).

Once approved, you make a down payment, and the lender covers the rest. Your loan is secured by the home, creating a lien. Monthly payments follow an amortization schedule, where early payments go mostly to interest, shifting toward principal over time. If you miss payments, foreclosure is possible, but U.S. laws like the CARES Act provide protections during hardships.

Breaking Down Your Monthly Mortgage Payment: PITI

Your payment isn't just principal and interest—it's PITI: Principal, Interest, Taxes, and Insurance. Here's how it breaks down:

- Principal: The loan amount you borrowed, reducing your balance over time.

- Interest: The lender's fee for the money, calculated as a percentage of the remaining balance.

- Taxes (T): Local property taxes, often escrowed and paid annually by your servicer.

- Insurance (I): Homeowners insurance, required by lenders to protect against damage.

For example, on a $300,000 home with 20% down ($60,000), your $240,000 loan at 6.5% interest (2026 average) might yield a PITI payment of about $1,800 monthly on a 30-year term.

Types of Mortgages Available in 2026

Choosing the right type depends on your finances and risk tolerance. Common options include:

Fixed-Rate Mortgages

These lock in your interest rate for the entire term—usually 15, 20, or 30 years—offering payment stability. A 30-year fixed is popular for lower monthly costs, while 15-year builds equity faster but has higher payments. In 2026, expect rates around 6-7% amid steady Fed policies.

Adjustable-Rate Mortgages (ARMs)

ARMs start with a fixed rate for 5-10 years, then adjust based on market indexes like SOFR. They're ideal if you plan to sell or refinance before adjustments, but payments can rise.

Government-Backed Loans

- FHA Loans: Low down payments (3.5%) for credit scores as low as 580; great for first-timers.

- VA Loans: No down payment for eligible veterans, backed by the U.S. Department of Veterans Affairs.

- USDA Loans: For rural buyers with zero down, income limits apply.

Conventional loans require 3-20% down and stronger credit.

Mortgage Qualification: What Lenders Look For

To qualify, prepare these essentials:

| Factor | Ideal Range | Why It Matters |

|---|---|---|

| Credit Score | 620-740+ | Higher scores mean better rates. |

| Down Payment | 3-20% | Less than 20% often requires PMI. |

| DTI Ratio | Under 43% | Shows you can afford payments. |

| Loan-to-Value (LTV) | 80% or less | Lower LTV avoids extra insurance. |

Private Mortgage Insurance (PMI) protects the lender if you put less than 20% down; it costs 0.5-1% of the loan annually and drops off once you reach 20% equity.

Steps to Get a Mortgage in the U.S.

- Check Your Credit: Get free reports from AnnualCreditReport.com.

- Save for Down Payment: Aim for 3-20%; use FHA for less.

- Get Pre-Approved: Shop lenders for the best rate—compare via sites like Bankrate.

- Find a Home: Work with a real estate agent; get a home inspection.

- Apply and Close: Submit docs; closing costs average 2-5% of the loan.

Pro Tip: Lock in your rate during application to hedge against 2026 rate fluctuations.

Common Mortgage Costs and Fees

Beyond PITI, watch for:

- Origination fees (0.5-1% of loan)

- Appraisal ($300-500)

- Closing costs ($5,000+ average)

- PMI if down payment <20%

Shop around—lenders must provide a Loan Estimate within 3 days of application per TRID rules.

Next Steps to Secure Your Mortgage

Ready to move forward? Pull your credit report today, calculate your budget using online tools from Freddie Mac, and get pre-approved from 3 lenders. Compare rates on LendingTree or consult a HUD-approved counselor at no cost. With preparation, you'll navigate the process confidently and own your piece of the American dream sooner. Start small—your future home awaits.

Frequently Asked Questions

Sources & References

-

1

How Do Mortgages Work? | City National Bank — www.cnb.com

-

2

What is a mortgage? Meaning and steps | Rocket Mortgage — www.rocketmortgage.com

-

3

What Is a Mortgage Loan (& How Do They Work)? | NBC Banking — www.nbcbanking.com

-

4

How does a mortgage work? (2026) | ConsumerAffairs — www.consumeraffairs.com

-

5

[2026] What is a Mortgage? Everything You Need to Know Here | BlueRate — www.bluerate.ai

-

6

Understanding Mortgage Terms in 2026: The Complete Guide | Amerisave — www.amerisave.com

-

7

What is a mortgage? | U.S. Bank — www.usbank.com

Useful Tools

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...