How Long Does Negative Information Stay on Your Credit Report?

Your credit report is like a financial report card, and negative items on it can feel like they'll haunt you forever. The good news? They won't. Most negative information stays on your credit report f...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Your credit report is like a financial report card, and negative items on it can feel like they'll haunt you forever. The good news? They won't. Most negative information stays on your credit report for seven years, but understanding the specifics can help you plan your financial recovery and know when you'll see improvement.

Understanding Negative Information on Your Credit Report

Negative information includes anything that reflects poorly on your credit history—late payments, collections accounts, foreclosures, charge-offs, and bankruptcies. When these items appear on your credit report, they can significantly impact your credit score and make it harder to qualify for loans, credit cards, or even favorable interest rates.

The Fair Credit Reporting Act (FCRA), a federal law that governs how the three major credit bureaus (Equifax, Experian, and TransUnion) operate, sets strict limits on how long negative information can remain on your report. Understanding these timelines is crucial because it gives you a roadmap for credit recovery.

How Long Different Negative Items Stay on Your Credit Report

The length of time negative information stays on your credit report depends on the type of derogatory item. Here's the breakdown:

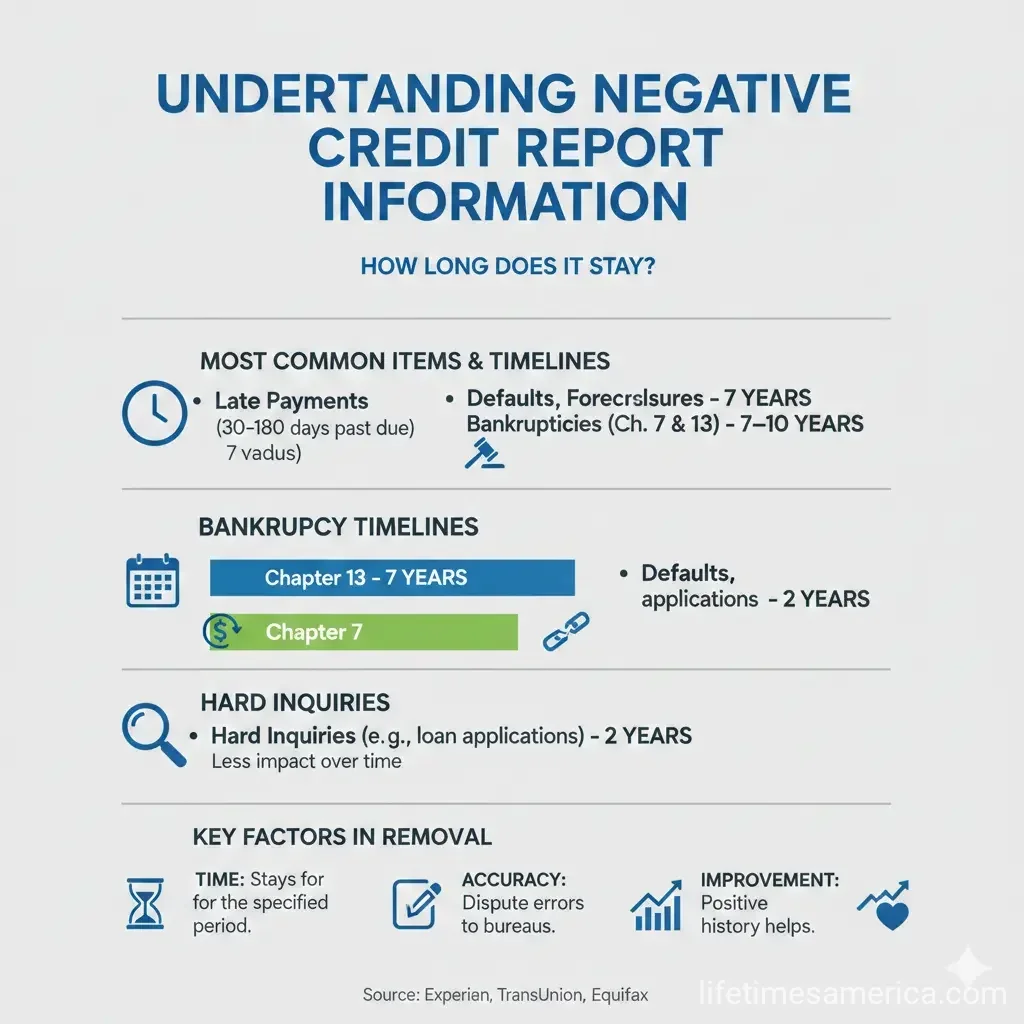

Seven-Year Items

Most negative credit items remain on your report for seven years from the date of the original delinquency (the first missed payment):

- Late payments: Seven years from the missed payment date

- Collections accounts: Seven years from the original delinquency date

- Foreclosures: Seven years from the original delinquency date

- Charge-offs: Seven years from the original delinquency date

- Chapter 13 bankruptcy: Seven years from the filing date

- Defaults: Seven years from the original delinquency date

For accounts sent to collections, the clock starts from when you first missed the payment, not when the collection agency took over the account. This is an important distinction because it means the seven-year countdown may have already begun before you even hear from a collector.

Ten-Year Items

Chapter 7 bankruptcy is the notable exception to the seven-year rule. Chapter 7 bankruptcies remain on your credit report for ten years from the filing date. This longer reporting period reflects the more severe nature of Chapter 7, where most debts are discharged rather than repaid.

Special Cases: Student Loans and Child Support

Most federally insured or federally-issued student loans follow the standard seven-year rule for negative information. However, Perkins loans are an exception and can be reported indefinitely if they're in default. Private student loans are treated like other credit accounts, with negative information staying for seven years or seven years and 180 days if sent to collections.

Overdue child support can be reported for seven years on your credit report.

The Impact of Age on Your Credit Score

Here's something encouraging: even though negative items stay on your report for seven to ten years, their impact on your credit score diminishes significantly over time. A collection account that's five years old will hurt your score much less than one that's five months old.

Two factors determine how much damage a negative item causes:

- Recency: More recent negative items have a greater impact on your score. A late payment from last month will hurt you more than one from three years ago.

- Severity: A 90-day late payment is more damaging than a 30-day late payment. Similarly, a bankruptcy is more severe than a single missed payment.

This means that even if negative information is still technically on your report, its damage to your creditworthiness decreases as time passes. Many lenders focus more on recent credit behavior than ancient history.

When Does the Clock Start?

Understanding when the seven or ten-year countdown begins is critical for planning your credit recovery. The clock generally starts from the original delinquency date—the date of the first missed payment that led to the negative item.

For bankruptcy, the countdown starts from the date you file the petition with the court, not when your case is discharged.

This distinction matters because if you miss a payment in January 2026 and it goes to collections in March 2026, the seven-year clock started in January 2026, not March. Mark your calendar: that negative item should fall off in January 2033.

Can You Remove Negative Information Before Seven Years?

While negative items generally stay on your report for seven to ten years, you have options to address them sooner:

Dispute Inaccurate Information

If any negative information on your credit report is incorrect, you have the right to dispute it with the credit bureaus. You can file a dispute directly with Equifax, Experian, or TransUnion, or work with a consumer protection attorney. If you can prove the information is wrong, it can be removed immediately, regardless of age.

Pay for Delete (Risky Strategy)

Some people attempt to negotiate a "pay for delete" agreement with creditors or collection agencies, where you pay the debt in exchange for removal from your credit report. However, this practice is controversial and not guaranteed to work. Many creditors won't agree, and such agreements may violate Fair Debt Collection Practices Act guidelines.

Goodwill Deletion

If you've had an isolated late payment but otherwise maintained good credit, you can try writing a goodwill letter to your creditor requesting they remove the negative item. There's no guarantee they'll comply, but it's worth attempting if you have a reasonable explanation for the late payment.

Your Rights Under Federal Law

The FCRA protects your rights as a consumer. If a credit bureau violates the law by reporting incorrect information or keeping negative items on your report longer than allowed, you may be entitled to compensation, including:

- Up to $1,000 for a violation, regardless of actual damages

- Actual damages you've suffered (financial losses or emotional distress)

- Reasonable attorney's fees and court costs

- Punitive damages if willful violation can be proven

If you believe a credit bureau has violated your rights, consider consulting with a consumer protection attorney.

Monitoring Your Credit Report

You're entitled to a free credit report from each of the three major bureaus once per year through AnnualCreditReport.com, the official source authorized by the Federal Trade Commission. Regularly checking your reports helps you:

- Verify that negative items are being reported correctly

- Catch errors or fraudulent accounts

- Track when negative items will fall off

- Monitor your overall credit improvement progress

Consider spacing out your three free reports throughout the year—one from each bureau every four months—to keep a regular eye on your credit health.

Building Credit While Negative Items Remain

You don't have to wait seven years for your credit to improve. While negative items are still on your report, you can:

- Make all payments on time: Recent positive payment history is heavily weighted in credit scoring models

- Keep credit card balances low: Aim to use less than 30% of your available credit

- Don't close old accounts: Keeping older accounts open helps your credit history length

- Diversify your credit mix: Having different types of credit (cards, installment loans, etc.) can help

- Become an authorized user: If someone with good credit adds you to their account, it may boost your score

Frequently Asked Questions

Moving Forward: Your Path to Better Credit

Negative information on your credit report doesn't have to define your financial future. Most items disappear after seven years, and their impact diminishes much sooner. Focus on building positive credit habits now—making on-time payments, reducing debt, and monitoring your credit report regularly. These actions will help your credit score recover even while negative items remain on your report.

Start by getting your free annual credit report from AnnualCreditReport.com and reviewing it carefully for errors. If you find inaccuracies, dispute them immediately. Then commit to positive credit behavior moving forward. Your future self will thank you.

Sources & References

MyFICO — How Long Does Negative Information Stay on Credit Reports?

Katz Law Group — How Long Does Negative Information Stay on My Credit Report?

The Points Guy — How Long Negative Information Can Stay on Your Credit Report

Experian — How Long Can Negative Items Stay on Your Credit Report?

Nolo — How Long Does Negative Information Stay on a Credit Report?

University of Wisconsin Extension — How Long Does Information Stay In Your Credit Report?

Equifax — How Long Does It Take for Information to Fall Off Credit Reports?

Federal Trade Commission — Disputing Errors on Your Credit Reports

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...