What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over your financial life than you might realize. In the USA, understanding what counts as a good credit score can open doors to better rates, approvals, and opportunities, saving you thousands in interest over time.

Whether you're building credit from scratch, recovering from setbacks, or just curious about where you stand, this guide breaks it all down. We'll cover the ranges, what they mean for everyday Americans, and practical steps to boost your score in 2026.

What Is a Credit Score?

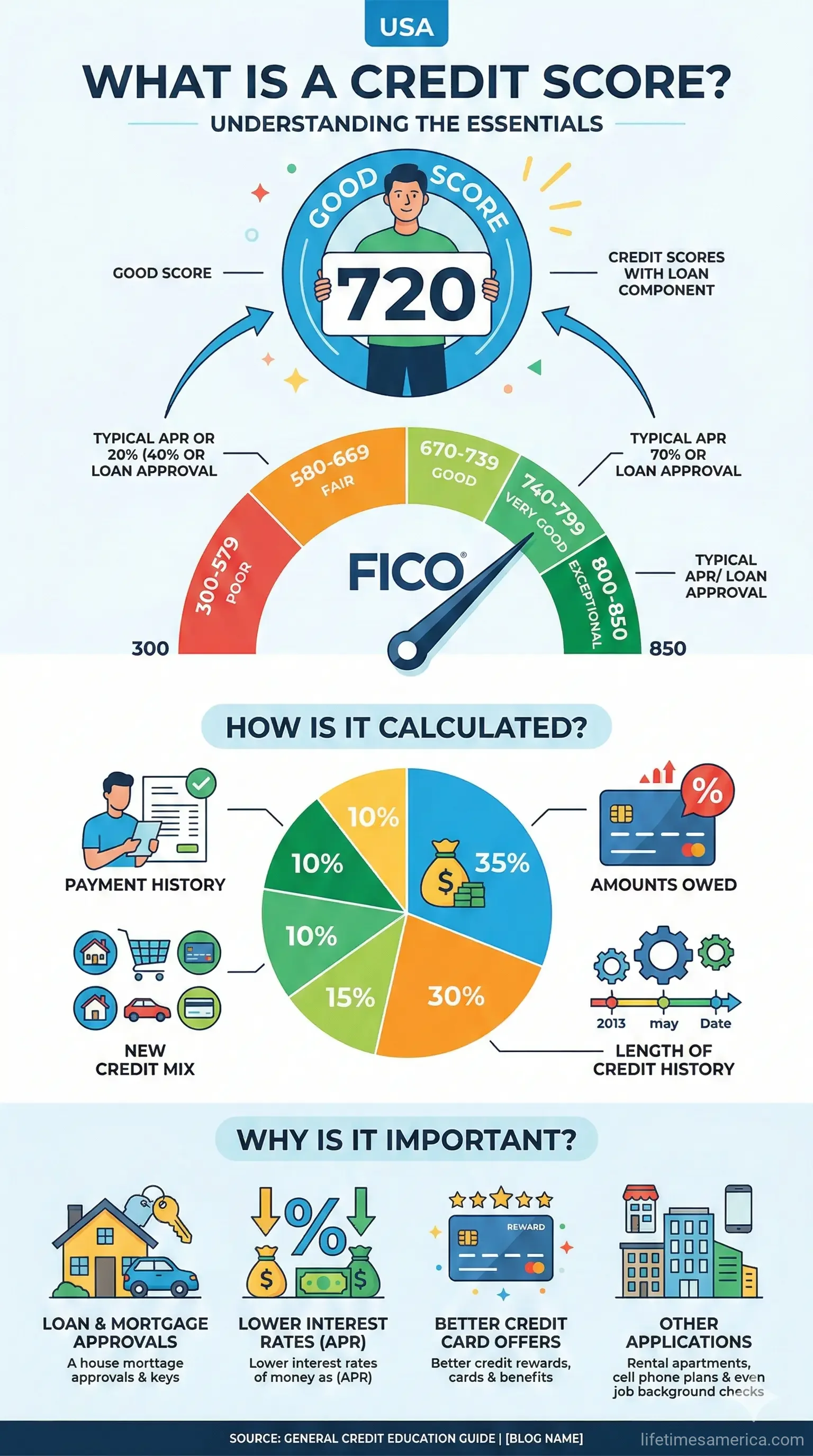

A credit score is a three-digit number, typically ranging from 300 to 850, that summarizes your creditworthiness based on your credit history. Lenders like banks, credit card issuers, and mortgage companies use it to decide if you'll get approved for loans and at what interest rate. It's calculated from data in your credit reports provided by the three major bureaus: Equifax, Experian, and TransUnion.

The two dominant models are FICO® Scores, used by 90% of top lenders, and VantageScore, favored by the credit bureaus. Both pull from five key factors: payment history (35% of FICO), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%).

Why Your Credit Score Matters in the USA

Beyond loans, your score affects apartment rentals, utility deposits, job applications (especially in finance), and even insurance premiums. For instance, a strong score can qualify you for premium rewards credit cards or favorable terms on a 401(k) loan from your employer plan. In 2026, with inflation cooling but rates still elevated, a good score means real savings—think hundreds less per month on a mortgage.

Credit Score Ranges: What Counts as Good?

There's no universal "good" score— it depends on the model—but consensus points to the mid-600s and up as solid territory. Here's the breakdown for the most common scales used in the USA today.

FICO Score Ranges

FICO, the gold standard for lenders, defines ranges like this:

- 800-850: Excellent – Best rates, highest approval odds. Only about 23% of Americans hit this in recent data.

- 740-799: Very Good – Strong terms, easy approvals. Represents 27.5% of consumers.

- 670-739: Good – Acceptable to lenders, qualifies for most credit. About 20.4% fall here.

- 580-669: Fair – Higher rates, tougher approvals (14.9%).

- 300-579: Poor – High-risk, limited options (14.2%).

The average FICO score in the USA as of January 2026 is 705, up slightly from prior years, reflecting improved payment behaviors post-pandemic.

VantageScore Ranges

VantageScore, used by many credit card companies, has a similar 300-850 scale but tweaks the bands:

- 781-850: Super Prime – Top-tier perks.

- 661-780: Prime (Good) – Strong approvals, good rates.

- 601-660: Near Prime – Most credit available, but watch rates.

- 300-600: Subprime – Higher costs, fewer options.

In 2025 data (carrying into 2026), the average VantageScore was 701. About 61% of Americans have a Good or better VantageScore.

| Score Range | FICO Label | VantageScore Label | % of Americans (FICO) |

|---|---|---|---|

| 800-850 | Excellent | Super Prime | 23% |

| 740-799 | Very Good | Prime | 27.5% |

| 670-739 | Good | Prime | 20.4% |

| 580-669 | Fair | Near Prime/Subprime | 14.9% |

| 300-579 | Poor | Subprime | 14.2% |

Note: Industry-specific FICO scores (e.g., for auto or cards) range 250-900 but keep the same "good" band of 670-739.

What Does a Good Credit Score Get You?

A score of 670+ signals reliability, unlocking perks like:

- Lower APRs on credit cards (e.g., 12-15% vs. 20%+ for fair scores).

- Better mortgage rates—saving $200+/month on a $300,000 home loan.

- Easier auto financing; scores above 700 often get prime rates.

- Rental approvals without deposits; some landlords check FICO.

- Job edges in banking or government roles via background checks.

For example, on a $10,000 personal loan, a 670 score might cost $1,200 more in interest over 3 years than a 739. Experts say 700+ is ideal for negotiating power, as lenders compete for low-risk borrowers.

Average Credit Scores by Age and State

Scores rise with age due to longer histories. Here's 2026 data:

- 18-24: ~680 (building phase)

- 25-34: ~690

- 35-44: ~710

- 45-54: ~730

- 55+: ~750+

State averages vary: Highest in Minnesota (740+), lowest in Mississippi (680ish). Check your state's trends via AnnualCreditReport.com.

How to Check and Monitor Your Credit Score

- Get free weekly reports: Visit AnnualCreditReport.com, authorized by federal law (FACTA), for Equifax, Experian, TransUnion reports. Scores aren't free here, but reports show factors.

- Free scores: Use Credit Karma (VantageScore), Credit Sesame, or bank apps like Ally. FICO via myFICO or your credit card issuer.

- Paid monitoring: myFICO Advanced ($30+/month) for all models.

- Dispute errors: File free with bureaus; fixes can boost scores 20-100 points.

Practical Tips to Improve Your Credit Score in 2026

Aim for 670+ with these actionable steps, tailored for busy Americans:

Pay Bills on Time (35% Impact)

Set autopay for everything—mortgage, utilities, cards. Even one late payment dings you for 7 years. Use apps like Mint for reminders.

Lower Utilization (30% Impact)

Keep balances under 30% of limits (ideal: <10%). Pay down debt aggressively; consider balance transfers.

Build History Length (15%)

Keep old accounts open. Add a secured card if new to credit.

Limit New Credit (10%)

Space applications 6+ months. Multiple inquiries hurt short-term.

Diversify Mix (10%)

Balance revolving (cards) and installment (loans) debt responsibly.

"On-time payments still matter most. Lower balances relative to limits are key in 2026."

Pro tip: Enroll in Experian Boost for utility/phone payments to add positive history instantly.

Common Mistakes to Avoid

- Closing old cards (hurts history/utilization).

- Maxing cards before applying.

- Ignoring medical debt (now factors less, but still reportable).

- Co-signing without understanding risks.

Next Steps to Boost Your Score Today

Pull your free credit reports now at AnnualCreditReport.com. Calculate utilization, set autopay, and track monthly. If in debt, explore nonprofit counseling via NFCC.org or IRS-referred programs. Small habits compound—many hit "good" territory in months. You've got this; a stronger score means financial freedom ahead.

Frequently Asked Questions

Sources & References

-

1

Think your credit score is 'good'? Experts break down what the ... — the-independent.com — www.the-independent.com

-

2

What Is A Good Credit Score? | Equifax® — equifax.com — www.equifax.com

- 3

-

4

What Is a Good Credit Score? - Experian — experian.com — www.experian.com

- 5

-

6

What Is a Good Credit Score? | Kiplinger — kiplinger.com — www.kiplinger.com

- 7

-

8

Your 2026 Credit Score Playbook: The Biggest Changes — my100bank.com — www.my100bank.com

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

How to Check Your Credit Score for Free in the USA

Ever stared at a "declined" message on your credit card application or wondered why your dream home loan came with sky-high interest rates? Your credit score is the silent gatekeeper to your financial...