How to Check Your Credit Score for Free in the USA

Ever stared at a "declined" message on your credit card application or wondered why your dream home loan came with sky-high interest rates? Your credit score is the silent gatekeeper to your financial...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever stared at a "declined" message on your credit card application or wondered why your dream home loan came with sky-high interest rates? Your credit score is the silent gatekeeper to your financial future in America, influencing everything from mortgage approvals to job offers. The good news? Checking it doesn't have to cost a dime. In 2026, federal law makes it easy to access your credit information for free—weekly, even—straight from the source.

This guide walks you through how to check your credit score for free in the USA, step by step, with tips to avoid scams and maximize your financial health. Whether you're buying a home, applying for a car loan, or just staying on top of your credit, you'll have everything you need to take control today.

Understanding Credit Scores and Reports: The Basics

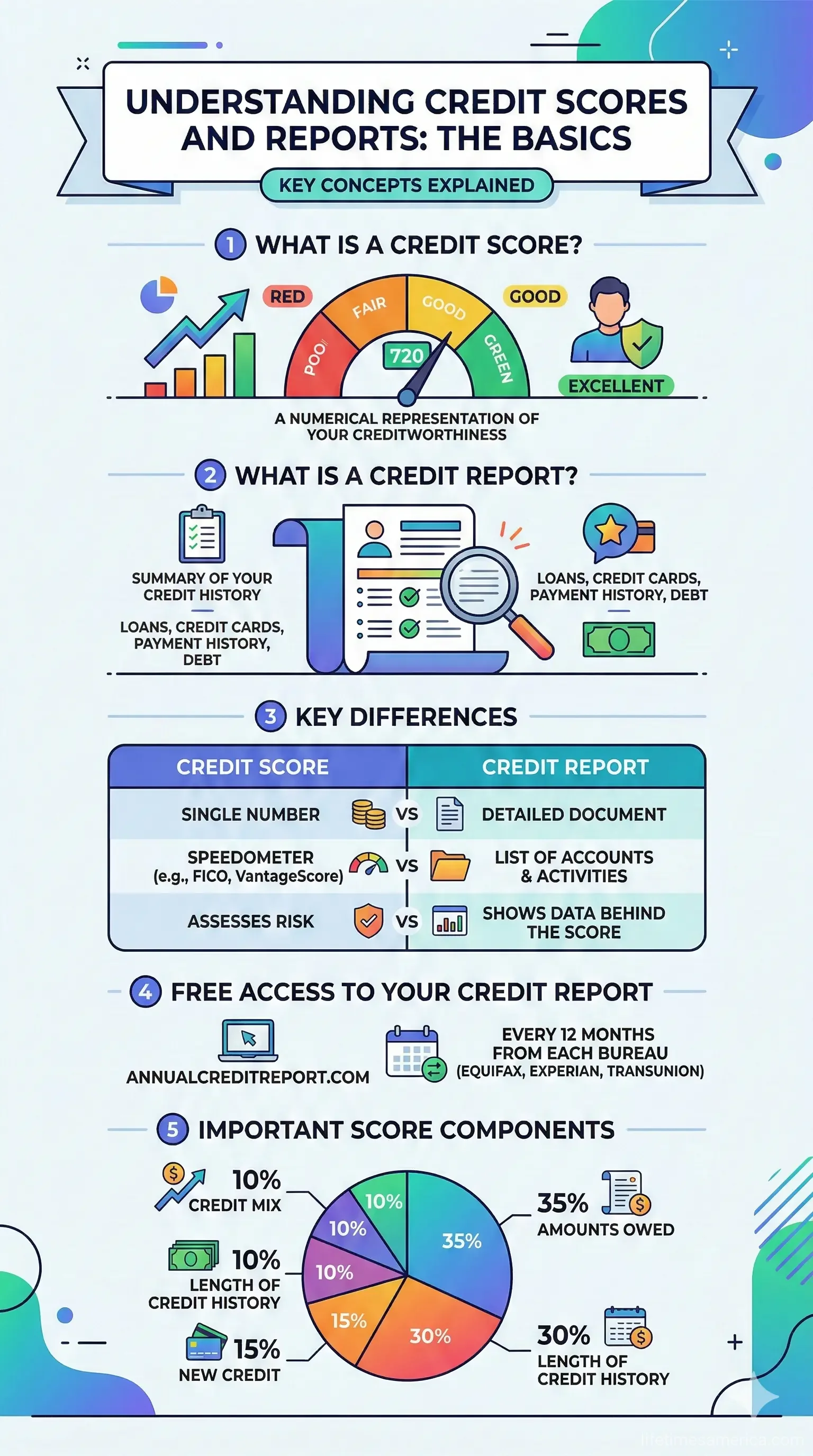

Before diving into free access methods, let's clarify the difference: a credit report is a detailed record of your financial history, while a credit score is a three-digit number (typically 300-850) summarizing your creditworthiness. Lenders use scores like FICO® or VantageScore to decide if you'll get approved and at what rate.

Your credit report includes personal details (name, SSN, addresses), account info (credit cards, loans, balances), payment history, and public records like bankruptcies. Scores factor in payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%).

Why Check Regularly?

- Catch errors or fraud early: One in five Americans has incorrect info on their report, which could tank your score.

- Monitor identity theft: Spot unauthorized accounts before they spiral.

- Prepare for big moves: Homebuying? Job hunting? Know your score to negotiate better terms.

- Track progress: See how payments or debt reduction boost your score over time.

Regular checks—self-inquiries—won't hurt your score. It's when lenders pull your report (hard inquiry) that it might dip slightly.

Your #1 Free Resource: AnnualCreditReport.com

Congress mandated this under the Fair Credit Reporting Act (FCRA). It's the only federally authorized site for truly free credit reports from all three major bureaus: Equifax, Experian, and TransUnion. No credit card needed, no upsells—just facts.

Step-by-Step: How to Get Free Weekly Reports

- Visit AnnualCreditReport.com: The official hub. Avoid imposters like "freecreditreport.com"—they're private sites pushing paid services.

- Verify your identity: Enter name, address, SSN, and answer questions about your credit history. Takes 5-10 minutes.

- Select bureaus: Grab all three at once or space them out (e.g., one every four months) for year-round monitoring.

- Review online or download: Free weekly access online in 2026—staggered pulls keep you vigilant without limits.

- Phone or mail alternative: Call (877) 322-8228 or mail to Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281.

Pro tip: Set a calendar reminder every four months. Checking weekly via the site helps spot changes fast, like new inquiries or missed payments.

Federal law allows you to get a free copy of your credit report every 12 months from each credit reporting company—and more frequently online.

Free Credit Scores: Beyond the Reports

Free reports from AnnualCreditReport.com don't include scores—that's a paid add-on elsewhere. But several legit services offer free credit scores updated regularly, no card required.

Top Free Score Options in 2026

- Experian: Free FICO® Score 8 (most lender-used model), daily updates, no impact. See factors hurting your score and simulate changes like paying off debt.

- Equifax myEquifax: Free annual reports plus score monitoring. Sign up for alerts on changes.

- TransUnion (via Credit Karma or similar): VantageScore 3.0 for free, though not always identical to FICO. Great for trends.

- Bank perks: Many like Capital One, Discover, or American Express offer free FICO scores to customers. Check your statements.

| Service | Score Type | Update Frequency | Key Perk |

|---|---|---|---|

| Experian | FICO® 8 | Daily | Score simulator |

| Equifax | FICO® | Weekly | Fraud alerts |

| AnnualCreditReport.com | Report only | Weekly | All 3 bureaus |

These are soft pulls—safe for you, revealing to lenders.

Extra Free Reports: Who Qualifies?

The FCRA gives more than one freebie yearly if you qualify. Request within 60 days of the event—no charge from bureaus.

- Denied credit/insurance/employment: Get reports from all three.

- Unemployed, job-hunting soon: Within 60 days of applying.

- On public assistance: Welfare recipients qualify.

- Fraud victim: Free report plus fraud alert (initial: 1 year; extended: 7 years).

- State laws: Some states like California offer extras—check AnnualCreditReport.com.

After your annual freebies, bureaus can charge up to $14.50 per report, but stick to free options first.

Avoid Scams and Imposter Sites

Beware flashy ads promising "free scores!" Many lead to subscriptions. Stick to: - AnnualCreditReport.com (reports only). - Official bureau sites (Experian.com, Equifax.com). - USAGov or CFPB recommendations.

Red flags: Requests for credit cards upfront, unrelated "free trial" pushes, or sites mimicking the official one.

Tips to Improve Your Score After Checking

Got your report? Act on insights:

- Dispute errors: Online via bureau sites or mail. FCRA requires 30-day investigation.

- Pay on time: Set autopay—35% of your score.

- Reduce utilization: Keep balances under 30% of limits.

- Build history: Secured cards or credit-builder loans if thin file.

- Limit apps: Too many inquiries hurt.

Track via free tools—many show "what's changed" like new debts or inquiries.

Next Steps to Own Your Credit

Head to AnnualCreditReport.com right now—grab your reports and scores from Experian. Review for errors, set alerts, and pay down high balances. In weeks, you'll see improvements impacting real-life wins like lower auto loan rates or better apartment approvals. Your financial freedom starts with knowledge—stay vigilant, and watch your score soar.

Frequently Asked Questions

Sources & References

-

1

Get a Free Credit Report | Equifax® — www.equifax.com

-

2

Get Your Free Credit Score (No Credit Card Required) - Experian — www.experian.com

-

3

How to Get Free Credit Reports | myFICO — www.myfico.com

-

4

How do I get a free copy of my credit reports? — consumerfinance.gov — www.consumerfinance.gov

-

5

Annual Credit Report.com - Home Page — www.annualcreditreport.com

-

6

How to get free credit reports - DFPI - CA.gov — dfpi.ca.gov

- 7

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...