How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six months. It's not a pipe dream; with disciplined habits and smart strategies tailored for 2026, many Americans are doing exactly that. Boosting your credit score by 100 points in six months is achievable if you start with a score in the 500-600 range and focus on the biggest factors: payment history and credit utilization.

We'll break down proven, actionable steps grounded in how FICO and VantageScore models work in 2026. These tips draw from credit bureaus like Experian, TransUnion, and Equifax, plus real-world advice from financial experts. Whether you're prepping for a home purchase or just tired of rejection letters, this guide equips you with a six-month roadmap.

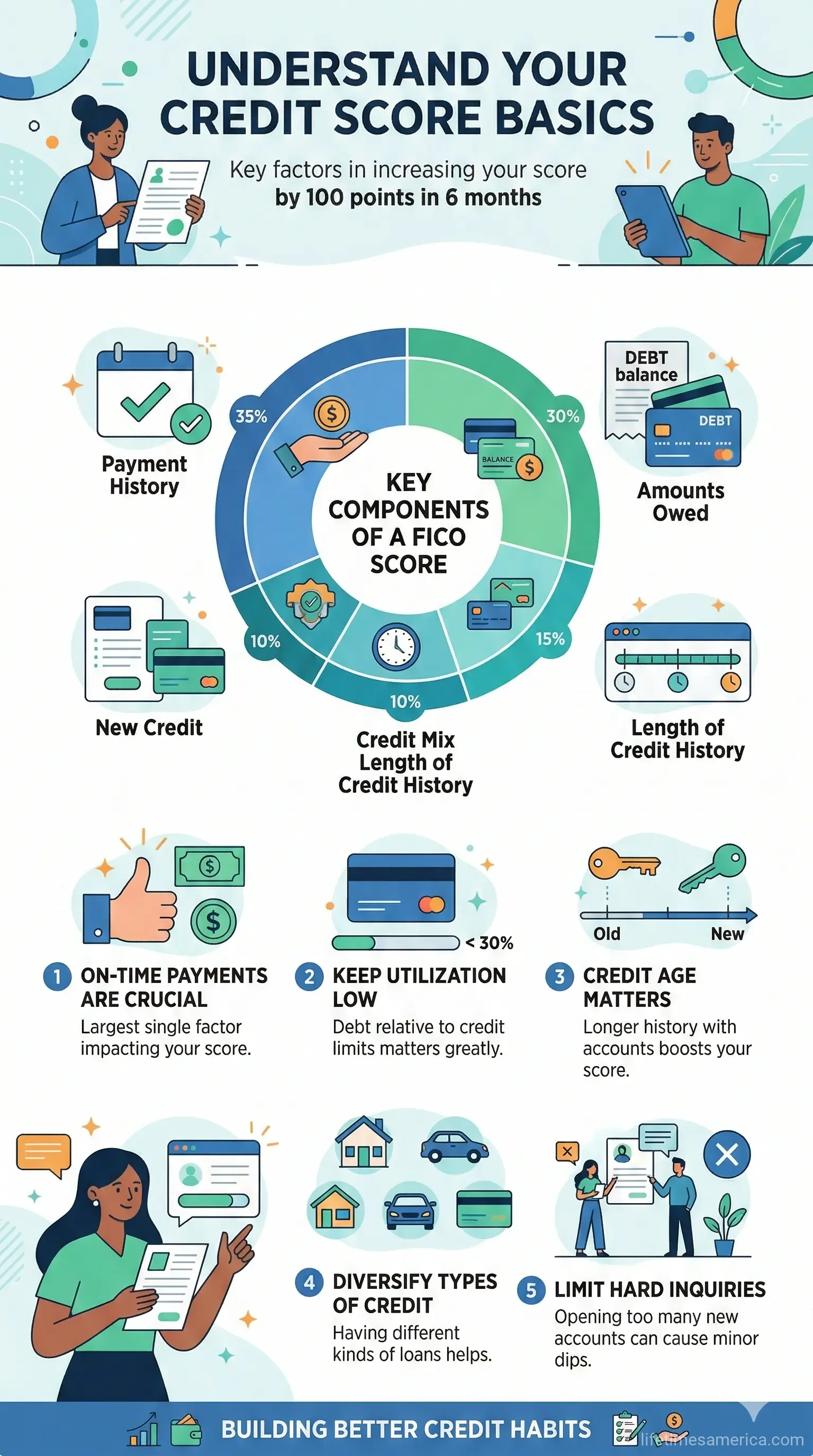

Understand Your Credit Score Basics

Before diving in, know what drives your score. Payment history makes up 35% of your FICO score, credit utilization 30%, length of credit history 15%, new credit 10%, and credit mix 10%. In 2026, models emphasize recent behavior, so consistent actions yield fast results. Free weekly reports from AnnualCreditReport.com (the official U.S. site authorized by federal law) let you check Equifax, Experian, and TransUnion without dinging your score.

Get your baseline now: Pull reports from all three bureaus. Dispute errors online—fixing inaccuracies can add 20-50 points quickly.

Step 1: Master On-Time Payments (Months 1-2 Focus)

Payment history is king. One late payment can drop your score 100 points and linger for seven years, but on-time payments rebuild trust fast. Set up autopay for at least the minimum on all accounts—credit cards, loans, utilities, even rent if reported via services like Experian Boost.

Practical Tips for Bulletproof Payments

- Automate everything: Use your bank's bill pay or apps like Mint to cover minimums, then manually pay more.

- Pay early: Aim two days before due dates to dodge processing delays.

- Track with alerts: Apps from your card issuer notify you of due dates and score changes.

Experts report scores climbing 50+ points in three months with perfect payments alone.

Step 2: Slash Credit Utilization Below 30% (Months 1-3 Priority)

Credit utilization—your balances versus limits—is the quickest lever. Keep it under 30%; ideal is under 10% for max gains. A client dropping from 90% to under 30% utilization saw a 70-point jump. Pay balances before your statement closes, as that's what bureaus report.

Fast-Track Utilization Wins

- Request credit limit increases on low-utilization cards (if you've been responsible)—this lowers your ratio without new debt.

- Make multiple payments per month to keep reported balances tiny.

- Avoid closing old cards; it spikes utilization and shortens history.

In 2026, balance transfer cards with 0% APR for 12-18 months help—transfer high-interest debt, pay aggressively, but mind 3-5% fees.

Step 3: Tackle Debt with Proven Payoff Methods (Months 2-5)

High-interest revolving debt kills scores. Use the debt snowball (smallest balances first for motivation) or avalanche (highest interest first for savings). Personal finance expert Andrew Lokenauth notes 100+ point gains in six months via snowball.

Snowball vs. Avalanche: Which Fits You?

| Method | How It Works | Best For | Potential Impact |

|---|---|---|---|

| Debt Snowball | Pay minimums, extra on smallest debt. Roll payments to next. | Motivation seekers | 100+ points in 6 months |

| Debt Avalanche | Minimums, extra on highest interest. Saves most money. | Math-focused savers | Fast utilization drops |

Consider nonprofit credit counseling via NFCC.org for negotiated lower rates—they're legit, unlike scams promising "erase debt fast." Debt consolidation loans or home equity options work if your score allows.

Step 4: Build Positive Credit History (Months 3-6)

Lengthen your history by keeping old accounts open. Add a credit-builder loan from a credit union: Pay into savings for 6-24 months; on-time payments report positively. Experian Boost adds utility/rent payments for free points.

- Use one card for gas/groceries, pay in full monthly.

- Maintain mix: 1-2 cards + installment loan (auto, personal).

- Avoid new apps: Hard inquiries drop scores 5-10 points each; limit to one per need.

Step 5: Monitor and Protect Your Progress (Ongoing)

Track weekly via Credit Karma or bank apps, set alerts for drops. Freeze credit at bureaus to thwart fraud—free and easy in 2026. Budget via apps, allocating 10-20% income to debt—ties into IRS tax perks like student loan interest deductions.

Review annually; life changes like job switches require tweaks.

Your 6-Month Timeline to 100 Points

- Month 1: Check reports, automate payments, pay down to 50% utilization.

- Months 2-3: Hit <30% utilization, dispute errors.

- Months 4-5: Eliminate 1-2 cards via snowball, add credit-builder.

- Month 6: Perfect payments, celebrate under 10% utilization.

Track milestones: 30 points by month 2, 70 by month 4, 100 by end.

Next Steps to Launch Your 100-Point Climb

Today, pull your free reports at AnnualCreditReport.com and calculate utilization. Set autopay tonight. In six months, you'll access better rates—think 2026 mortgage refis saving thousands yearly. Consistency wins; you're building lifelong financial freedom. Share your progress in comments—we're in this together!

Frequently Asked Questions

Sources & References

-

1

25 Tips to Improve Credit in 2026 (and Beyond) - Lumina Solar — luminasolar.com

- 2

-

3

26 Tips to Improve Credit in 2026 - Experian — www.experian.com

-

4

How to Improve Your Credit Score in 2026 - American Bank — www.americanbankusa.com

- 5

-

6

How to Improve Your Credit Score in 2026 - Elevate Credit Union — elevatecu.com

-

7

5 Ways to Boost Your Credit Score in 2026 - Middlefield Bank — www.middlefieldbank.bank

-

8

Your 2026 Credit Score Playbook - ELGA Credit Union — www.elgacu.com

-

9

Understanding Your Credit Score in 2026 - CSEFCU — www.csefcu.com

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...

How to Check Your Credit Score for Free in the USA

Ever stared at a "declined" message on your credit card application or wondered why your dream home loan came with sky-high interest rates? Your credit score is the silent gatekeeper to your financial...