How to Pay Off Credit Card Debt: Avalanche vs Snowball Method

Struggling with credit card debt? You're not alone—millions of Americans face this challenge every day, with average household debt hovering around $6,000 per card in 2026.Choosing between the avalanc...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Struggling with credit card debt? You're not alone—millions of Americans face this challenge every day, with average household debt hovering around $6,000 per card in 2026.Choosing between the avalanche and snowball methods can be your game-changer, helping you pay off debt faster while saving money on interest or building unstoppable momentum.

In this guide, we'll break down how to pay off credit card debt: avalanche vs snowball method, complete with step-by-step instructions, real-world examples, and tips tailored for U.S. households. Whether you're juggling high-interest Visa cards or store-branded Mastercards, these proven strategies from financial experts can get you debt-free.

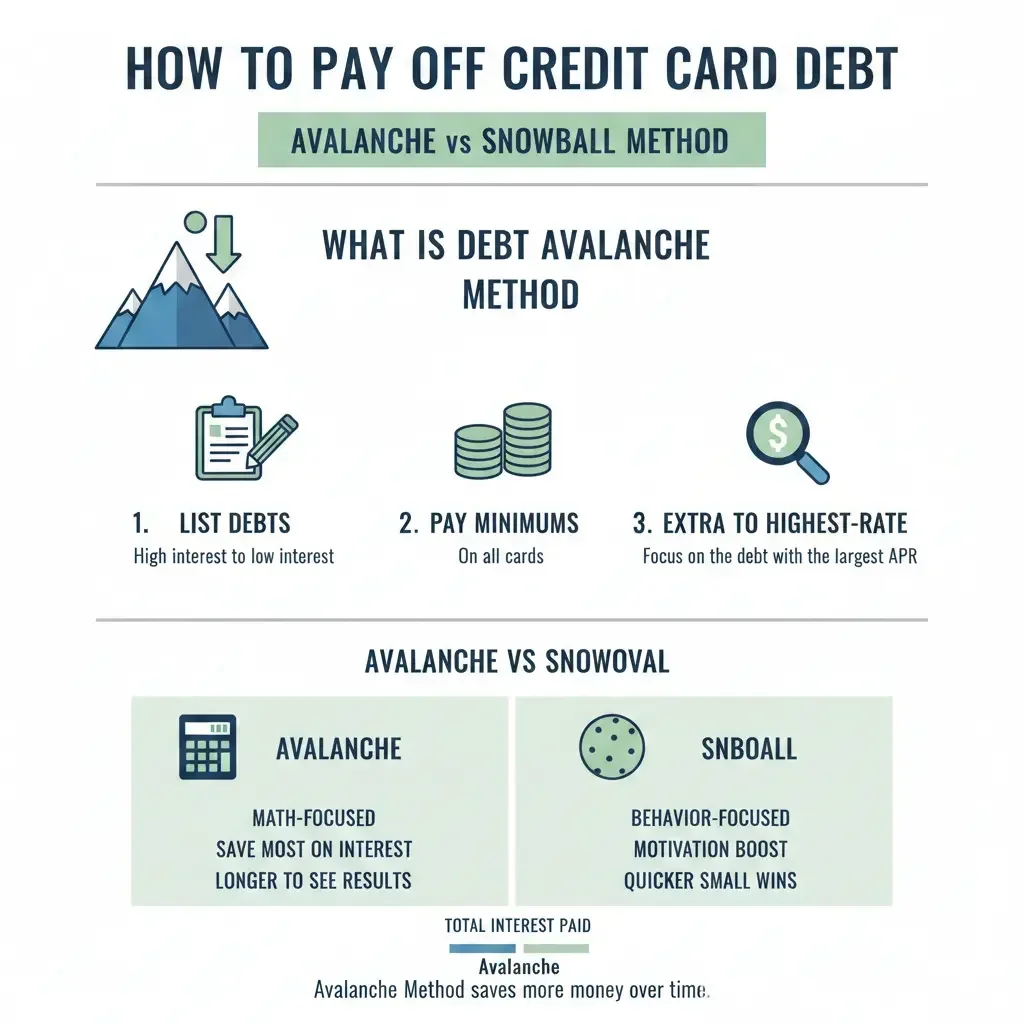

What Is the Debt Avalanche Method?

The debt avalanche method targets your highest-interest-rate debts first, minimizing the total interest you pay over time. This math-focused approach is ideal if you're analytical and want to save the most money.

How the Avalanche Method Works

- List all debts: Note balances, interest rates (APRs), and minimum payments. Credit cards often carry APRs of 20-30% in 2026.

- Make minimum payments: Cover the minimum on every account to avoid late fees and credit score damage.

- Attack the highest APR: Throw all extra cash at the debt with the top interest rate.

- Roll over payments: Once paid off, add that full payment (minimum + extra) to the next highest-APR debt. Repeat until debt-free.

Avalanche Example for Americans

Imagine Sarah from Texas with three cards: $3,000 at 26% APR ($90 min), $5,000 at 18% APR ($150 min), and $2,000 at 15% APR ($60 min). She has $400 extra monthly beyond minimums.

- Month 1-8: $490 ($400 extra + $90 min) obliterates the 26% card.

- Next: $640 ($490 rolled + $150) hits the 18% card in 9 months.

- Final: $790 clears the 15% card quickly.

Total interest saved: Up to thousands compared to minimum payments alone. In one scenario, avalanche cut interest by nearly $12,000 and shaved years off payoff.

Pros and Cons of Avalanche

- Pros: Saves most on interest; faster overall payoff if rates vary widely.

- Cons: Slower initial wins if high-rate debts are large balances.

What Is the Debt Snowball Method?

The debt snowball method orders debts from smallest to largest balance, ignoring interest rates. Popularized by experts like Dave Ramsey, it builds psychological momentum through quick victories—perfect for motivation.

How the Snowball Method Works

- List debts by balance: Smallest to largest, noting minimums.

- Minimums everywhere: Pay required amounts on all but the smallest.

- Extra on smallest: Devote all surplus funds to wipe it out fast.

- Snowball effect: Roll the full payment into the next debt, growing your firepower.

Snowball Example for Americans

Take Mike in Florida: $500 store card (25% APR, $25 min), $2,500 Visa (22% APR, $75 min), $8,000 Mastercard (20% APR, $240 min). $300 extra monthly.

- Months 1-2: $325 ($300 + $25) kills the $500 card.

- Next: $400 ($325 rolled + $75) clears $2,500 in 7 months.

- Final: $640 snowballs the $8,000 in under two years.

Those early "wins" keep you going, even if interest paid is slightly higher.

Pros and Cons of Snowball

- Pros: Quick wins boost morale; great for multiple small debts.

- Cons: Potentially more interest if small debts have low rates and big ones high.

Avalanche vs Snowball: Key Differences Compared

Which is better for how to pay off credit card debt: avalanche vs snowball method? It depends on your personality and debt profile. Here's a side-by-side:

| Feature | Avalanche | Snowball |

|---|---|---|

| Priority | Highest interest rate first | Smallest balance first |

| Best For | Math whizzes, high-rate debts | Motivation seekers, many small debts |

| Interest Savings | Highest (e.g., $12K less) | Lower, but faster feels |

| Time to First Win | Slower if big high-rate debt | Fastest possible |

If rates are similar (all under 20%), difference is minimal—pick for motivation. High rates? Avalanche wins mathematically.

Which Method Should You Choose in 2026?

Assess your debts via AnnualCreditReport.com (free weekly from U.S. bureaus). If high-APR cards dominate, go avalanche to combat 2026's average 22.83% rates. Need wins? Snowball.

Test both: Use free calculators from NerdWallet or Credit Karma. Analytical types save more with avalanche; others stick longer with snowball's dopamine hits.

Practical Tips to Supercharge Either Method

Maximize success with these U.S.-specific steps:

- Negotiate rates: Call issuers—1-2% drops save big. "Even a small reduction cuts costs meaningfully."

- Pay more than minimum: Minimums barely dent principal amid high APRs.

- Keep utilization under 30%: Protects FICO score for future loans like mortgages.

- Automate payments: Avoid misses that tank scores and add fees.

- Boost income/cut spending: Side gigs via Upwork or trim subscriptions—funnel to debt.

- Balance transfer cards: 0% intro APR offers (12-21 months) from Chase or Citi, but watch fees.

- Debt management plans: Non-profits like NFCC.org negotiate lower rates.

- Track progress: Apps like Undebt.it visualize your path.

Under Fair Credit Billing Act, dispute errors promptly. For hardship, explore 0% hardship programs from issuers.

Your Next Steps to Debt Freedom

Grab a notebook or spreadsheet today: List debts, pick your method, and commit extra dollars. Track monthly—celebrate milestones. If overwhelmed, contact NFCC.org for free counseling. You've got this—consistent action turns overwhelming balances into zero. Start now, and picture the financial freedom ahead: emergency funds, 401(k) contributions, and stress-free vacations.

Frequently Asked Questions

Sources & References

-

1

Avalanche vs Snowball Method: Which Debt Payoff Method is Best? — www.caminofcu.org

-

2

What to know about the debt snowball vs avalanche method — www.wellsfargo.com

-

3

Debt snowball method vs. debt avalanche method: Which is right for you? — www.fidelity.com

- 4

- 5

-

6

The Debt Snowball Method & How To Use It in 2026 — financialfootwork.com

-

7

6 Smart Ways to Manage Your Credit Balance in 2026 — www.yendo.com

-

8

How to Pay Off Debt: Top Strategies for 2026 — www.nerdwallet.com

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...