How Much Should You Have in an Emergency Fund?

Most Americans aren't sure how much emergency savings they actually need, and that uncertainty often leads to inaction. The good news? You don't need to have the perfect amount to get started—even a s...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Most Americans aren't sure how much emergency savings they actually need, and that uncertainty often leads to inaction. The good news? You don't need to have the perfect amount to get started—even a small emergency fund can protect you from financial disaster. Here's what you need to know about building an emergency fund that works for your life in 2026.

The Standard Emergency Fund Rule

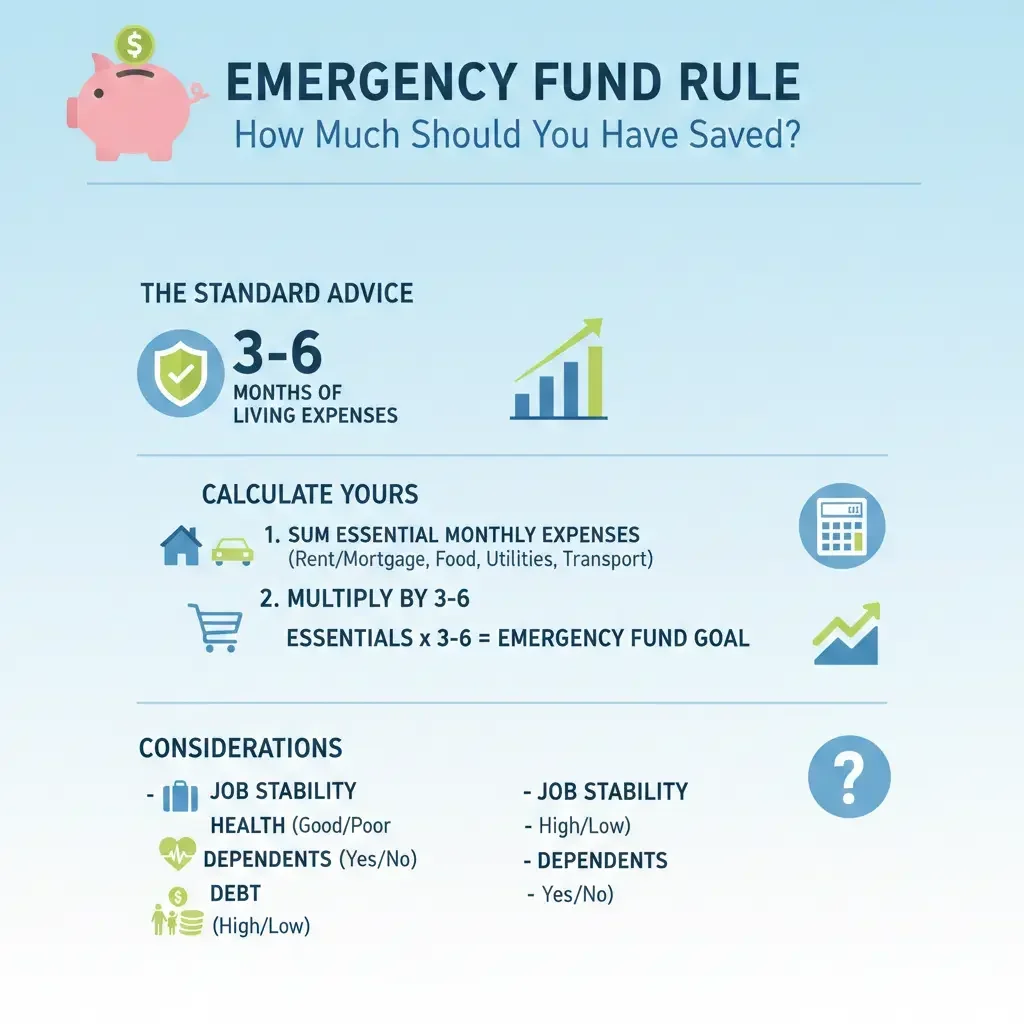

Financial experts have long recommended keeping three to six months of essential expenses in an easily accessible emergency fund. However, this isn't a one-size-fits-all rule—it's more of a starting point that should reflect your specific situation.

Here's how to calculate your target: Start by identifying your bare-bones monthly expenses—the essentials you absolutely need to cover, such as:

- Rent or mortgage payments

- Utilities

- Groceries

- Insurance premiums

- Minimum debt payments

- Transportation costs

Notice what's not on that list: dining out, entertainment, subscriptions, or luxury purchases. Your emergency fund covers necessities, not your normal lifestyle.

For example, if your essential monthly expenses total $4,000, you'd aim for $12,000 (three months) to $24,000 (six months). That's a significant amount, which is why many Americans struggle to reach it.

How Much Emergency Fund Do You Really Need?

The amount that makes sense for you depends on several factors. Rather than a single target, think about emergency savings in "risk bands":

Three Months of Expenses

This amount may be sufficient if you:

- Have a stable, secure job

- Have dual household income

- Have minimal dependents

- Live in a low-cost area

Six Months of Expenses

This is a safer target if you:

- Work in a volatile industry

- Have variable income (freelance, commission-based, seasonal work)

- Support dependents or aging parents

- Have significant medical expenses

- Live in a high-cost area

Nine to Twelve Months of Expenses

This makes sense if you:

- Work in a field with long job searches (specialized professions)

- Have multiple dependents

- Are self-employed or own a business

- Have health conditions requiring ongoing care

The Reality Check: Where Americans Stand in 2026

Let's be honest about the current situation. According to a January 2026 Bankrate survey, only 47% of Americans have enough emergency savings to cover a $1,000 expense. Even more concerning, the average emergency expense is almost $1,700.

The numbers get worse when you look at broader trends:

- More than 33% of Americans don't have an emergency fund at all

- Of those who do have one, the median amount saved is just $500

- 56% of Americans have more credit card debt than emergency savings

- 58% of Americans say their emergency savings haven't increased in the past year

If these statistics describe your situation, you're not alone—and you're not failing. Building an emergency fund while managing rising costs for housing, groceries, and insurance is genuinely difficult for many households.

Why Emergency Funds Matter More in 2026

Emergency funds aren't just for job loss anymore. Today's financial shocks include:

- Unexpected medical bills or health emergencies

- Major home or car repairs

- Temporary income loss or reduced hours

- Job transitions or career changes

- Family emergencies requiring travel

- Childcare disruptions

Without an emergency fund, you're likely to turn to credit cards. Consider this real scenario: A $2,000 emergency on a credit card with a 19.99% APR and $50 minimum monthly payment means you'll pay $3,321.85 total—over $1,300 in interest alone. An emergency fund saves you money and stress.

Getting Started: A Practical Approach

If the idea of saving $12,000 to $24,000 feels impossible, here's the truth: you don't need to have the exact right amount before you start protecting yourself. Even $1,000 to $2,500 can stop a short-term emergency from derailing your finances.

Step 1: Start with a Starter Emergency Fund

Begin with a $1,000 starter fund. This covers many common surprises like minor car repairs or unexpected medical expenses. This first step is crucial because it creates the habit and removes the psychological barrier of "I haven't started yet."

Step 2: Automate Your Savings

Set up automatic transfers from your checking account to a dedicated savings account right after payday. You won't miss money you never see in your checking account, and consistency matters more than the amount.

If you have a $400 monthly surplus between income and spending, consider putting $300 toward your emergency fund.

Step 3: Capture Windfalls

Don't wait for perfect circumstances. Use financial windfalls to accelerate your emergency fund:

- Tax refunds: If you're expecting a refund in 2026, use it to jump-start your savings

- Bonus paychecks: In months where you receive three paychecks instead of two, save one of them

- Tax refunds and recent legislation: Many people may be getting larger refunds due to recent tax legislation

- Gifts or unexpected income: Bonuses, inheritance, or side gig earnings

Step 4: Build Gradually

You don't need to save $5,000 right away—that's not realistic for most people. Even saving a couple hundred dollars over the rest of 2026 "infinitely decreases the likelihood that you would have to go into debt if you had some sort of unexpected expense".

At just $2 per day, you'll save over $600 by the end of the year. At $50 per day, you can build a $6,000 fund in four months.

Step 5: Choose the Right Account

Keep your emergency fund in a separate, easily accessible account—ideally a high-yield savings account. This keeps the money separate from your spending money and earns you interest while you're saving.

Special Considerations for Different Situations

Variable Income

If your income is irregular (freelance work, commission-based, seasonal jobs), automation and visibility matter more. Build flexibility into your target amount and contributions. You might aim for six months rather than three.

Living Paycheck to Paycheck

If you're living paycheck to paycheck, focus on saving extra income rather than trying to carve out money from your regular budget. This might mean directing tax refunds, bonuses, or side gig earnings entirely to your emergency fund until you reach your starter goal.

Households with Dependents

Single-income households with dependents should aim for six months of expenses rather than three, as you have less income flexibility.

The Bottom Line

You don't need to be perfect to be prepared. Whether you're aiming for three months, six months, or starting with just $1,000, the most important step is beginning today. Your emergency fund creates slack in your financial system, giving you time and space to think instead of just reacting when unexpected expenses happen.

Start with a realistic goal based on your situation. Automate your savings. Capture windfalls. Build gradually. In 2026, with 58% of Americans saying that growing their emergency savings is a priority, you're not alone in recognizing this need. The difference between those who succeed and those who don't is action—and you can start today.

Frequently Asked Questions

Sources & References

- 1

-

2

How to Build an Emergency Fund in 2026: A Step-by-Step Guide — useorigin.com

- 3

-

4

Yes, You Need An Emergency Fund. Here's How To Start In 2026 — hermoney.com

-

5

How Americans are prioritizing money goals in 2026: survey — www.livenowfox.com

-

6

How to build an emergency fund for 2026 — www.rocketloans.com

-

7

Your 2026 Financial Roadmap — www.ithinkfi.org

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...