When Can You Retire in the USA? Understanding Retirement Age Rules

Imagine clocking out for the last time, sipping coffee on your porch without a worry about the next paycheck. For millions of Americans, that dream hinges on knowing when you can retire in the USA—a q...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine clocking out for the last time, sipping coffee on your porch without a worry about the next paycheck. For millions of Americans, that dream hinges on knowing when you can retire in the USA—a question tied to Social Security rules, savings, and personal goals. With 2026 marking a key milestone for full retirement age (FRA), understanding these rules is crucial to avoid benefit cuts or financial shortfalls.

This guide breaks down retirement age rules, from Social Security basics to strategies for maximizing your benefits. Whether you're a baby boomer eyeing 2026 or a Gen Xer planning ahead, you'll find practical steps tailored to U.S. laws and resources.

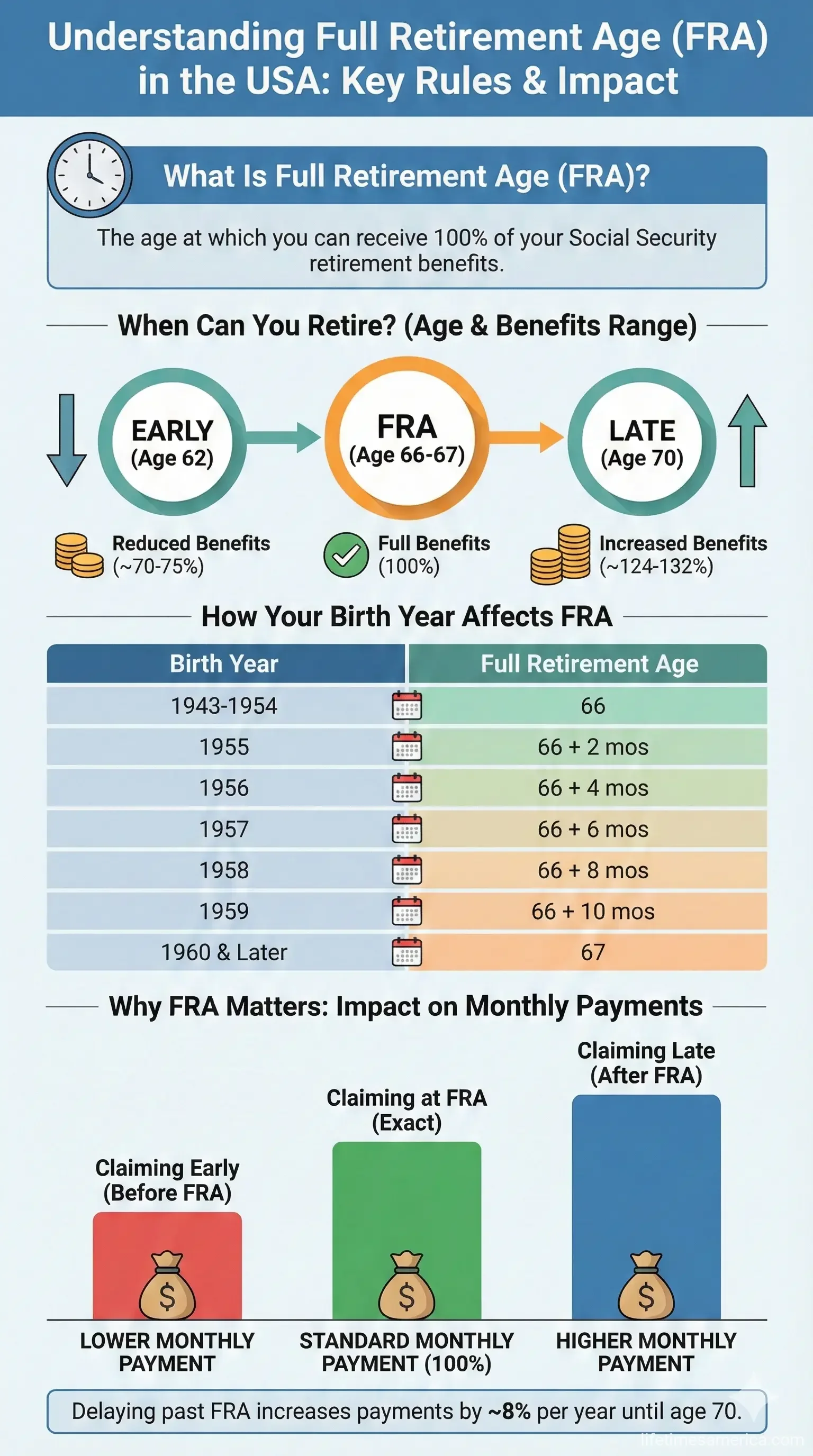

What Is Full Retirement Age (FRA) and Why Does It Matter?

Full retirement age is the point when you qualify for 100% of your Social Security retirement benefits, based on your lifetime earnings. Claiming earlier reduces your monthly check permanently; waiting longer boosts it.

Historically, FRA was 65, but the 1983 Social Security Amendments gradually raised it to address longer lifespans and program solvency. By 2026, FRA reaches 67 for everyone born in 1960 or later—a final step in that schedule.

Full Retirement Age by Birth Year

Here's the official SSA chart for clarity:

- Born 1943-1954: 66

- 1955: 66 and 2 months

- 1956: 66 and 4 months

- 1957: 66 and 6 months

- 1958: 66 and 8 months

- 1959: 66 and 10 months

- 1960 and later: 67

If you were born in 1960, your FRA hits in 2027, not 2026. Use the SSA's online calculator at ssa.gov to confirm your exact date.

2026 Changes: What Americans Need to Know

January 1, 2026, finalizes FRA at 67 for those born 1960 or later. This affects youngest boomers (1960-1964) and Gen Xers first. Early claiming at 62 still slashes benefits by about 30%—five-ninths of 1% per month for the first 36 months early, plus five-twelfths of 1% beyond that.

Other 2026 updates include a 2.8% COLA, bumping average retirement benefits from $2,015 to $2,071 monthly. Workers 50-59 and 64+ get an $8,000 catch-up 401(k) limit (up from $7,500), maxing contributions at $32,500.

Earnings Limits Before FRA

If you work before FRA, earnings above limits trigger benefit reductions—but only temporarily. In 2026:

- Under FRA all year: $2,040/month or $24,480/year. Above this? Benefits withheld for excess months.

- Reach FRA in 2026: $5,430/month allowed before your FRA month.

- At or after FRA: No earnings limit.

Example: John earns over the annual limit but keeps monthly earnings under $2,040 in summer months—he gets benefits then, but not if he exceeds in fall.

When Should You Actually Retire? Beyond Social Security

Social Security is just one piece. True retirement readiness blends benefits, savings, health, and lifestyle. Only 4 in 10 Americans feel on track to maintain their lifestyle, per Vanguard research.

Key Factors to Consider

- Savings Benchmarks: Aim for 10-12x your final salary by 67, per Fidelity guidelines. Use 401(k)s, IRAs, and Roth accounts.

- Medicare Enrollment: Starts at 65, three months before your birthday month. Delaying past FRA grows Social Security by 8% yearly until 70.

- Spousal and Survivor Benefits: Spouses get up to 50% of your FRA benefit; survivors up to 100%.

- Health and Longevity: Average U.S. life expectancy is 76 for men, 81 for women—plan for 20-30 post-retirement years.

Tax Perks in 2026

A temporary extra standard deduction helps seniors: up to $6,000 single/$12,000 joint for those 65+, phasing out above $75,000/$150,000 MAGI. Ends 2028.

Strategies to Maximize Your Retirement

Don't let FRA dictate your timeline—optimize it.

- Delay Claiming: Wait to 70 for maximum benefits (8% annual credits post-FRA).

- Work Part-Time: Stay under earnings limits to collect reduced benefits while saving more.

- Diversify Income: Build 401(k) (2026 max $23,500 base + catch-up), pensions, rentals.

- Bridge with Savings: Claim at 62 if needed, but have 3-5 years' expenses liquid.

- Check Statements: Create/log into mySocialSecurity account for personalized estimates.

"We'll add 8% to your benefit for each full year you delay receiving Social Security benefits beyond full retirement age."— Social Security Administration

Common Retirement Scenarios for Americans

- Born 1959: FRA at 66 years, 10 months (2026 if birthday early enough). Claim 62 for ~30% cut or delay for growth.

- Born 1960: FRA 67 in 2027. Perfect for part-time work in 2026.

- High Earner: Max taxable earnings may hold steady 2025-2026, affecting credits.

- Couple Planning: Coordinate claims—one delays, other claims spousal.

Plan Your Retirement Today: Next Steps

Retirement isn't a one-size-fits-all date—it's when your income, health, and dreams align. Start by:

- Logging into mySocialSecurity for your benefit estimate.

- Running numbers with SSA's Quick Calculator or Retirement Estimator.

- Consulting a fiduciary advisor via NAPFA.org or using free IRS VITA for taxes.

- Boosting savings: Max 401(k)/IRA now, eyeing 2026 catch-up limits.

- Reviewing Medicare at medicare.gov if nearing 65.

With FRA at 67 for most post-1960 births, you've got time to build security. Act now—your future self will thank you.

Frequently Asked Questions

Sources & References

- 1

-

2

Social Security Full Retirement Age Changes for January 2026 — downslawfirm.com — www.downslawfirm.com

-

3

US. The Full Retirement Age Hits 67 in 2026–Here's How To Avoid a ... — pensionpolicyinternational.com — www.pensionpolicyinternational.com

- 4

- 5

- 6

- 7

Useful Tools

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...