How to Invest Your First $1;000: A Beginner’s Guide to the S&P 500

Imagine turning your hard-earned $1,000 into a foundation for long-term wealth without needing a finance degree or Wall Street connections. For beginners in the United States, investing in the S&P 500...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine turning your hard-earned $1,000 into a foundation for long-term wealth without needing a finance degree or Wall Street connections. For beginners in the United States, investing in the S&P 500 through low-cost index funds or ETFs offers a simple, proven path to growth, backed by decades of market history.

This guide walks you through every step to invest your first $1,000 in the S&P 500, from building an emergency fund to automating contributions. You'll learn practical strategies tailored for Americans, including tax-advantaged accounts like IRAs and 401(k)s, using 2026's top options.

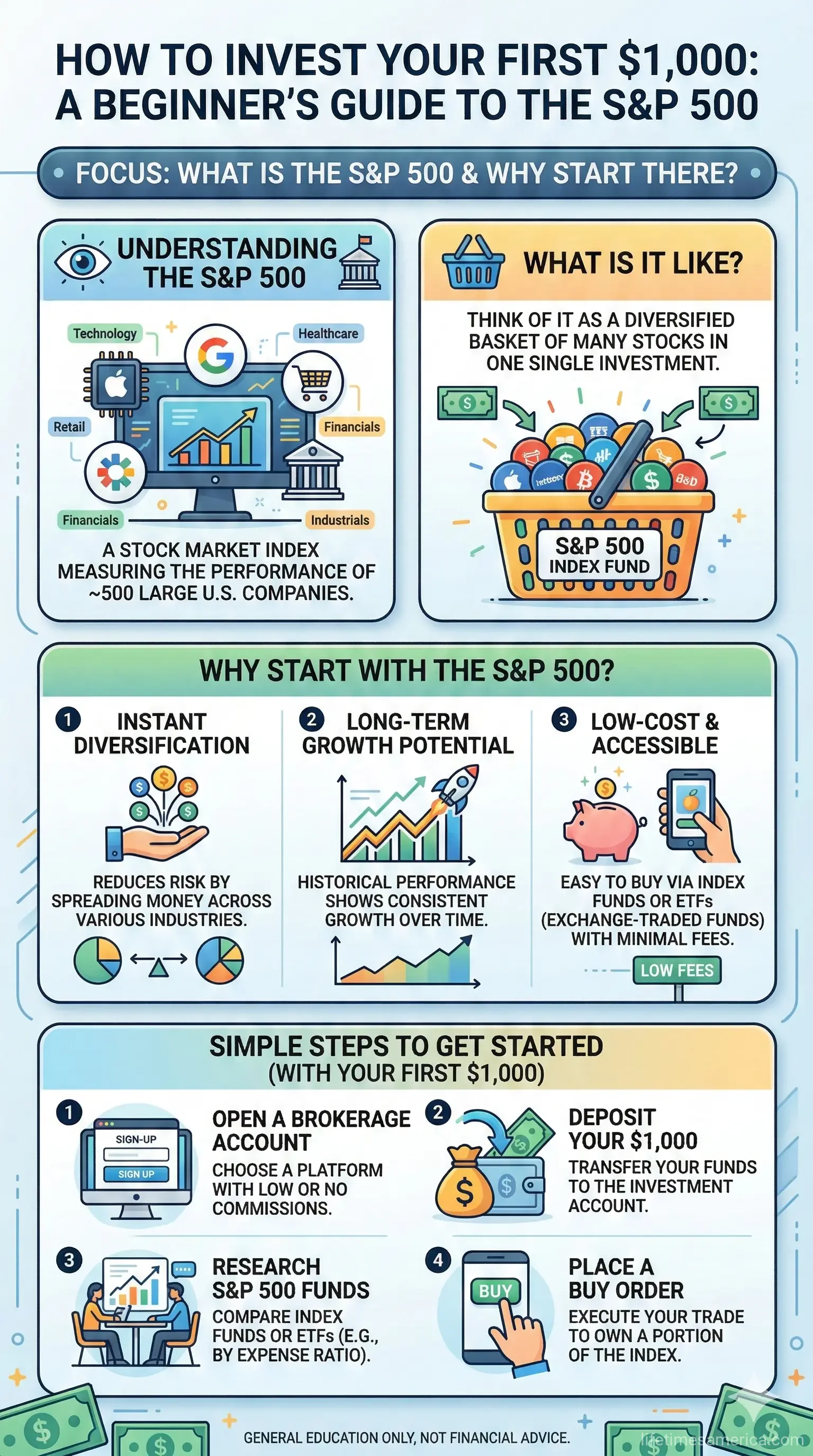

What Is the S&P 500 and Why Start There?

The S&P 500 is a market index tracking about 500 of the largest U.S. companies, representing roughly 80% of the total U.S. stock market. Think Apple, Microsoft, and Amazon—these "top dogs" drive economic growth. Investing in the S&P 500 doesn't mean buying the index itself; instead, you purchase an ETF or index fund that mirrors its performance, giving instant diversification across sectors like tech, healthcare, and finance.

Historical Performance and Beginner Benefits

Over time, the S&P 500 has delivered average annual returns of around 10% before inflation, turning consistent investments into substantial wealth. For your first $1,000, this low-risk entry beats letting cash sit in a savings account earning minimal interest. Beginners benefit from its stability—no need to pick individual stocks, which carries higher risk and requires constant monitoring.

In 2026, experts forecast above-trend growth with easing policies, making it an ideal time for selective exposure via S&P 500 trackers.

Step-by-Step: How to Invest Your First $1,000

Follow these actionable steps to get started today. Most brokerages have no minimums, so your $1,000 goes straight to work.

Step 1: Build Your Emergency Fund First

Before investing, protect yourself from surprises. Calculate your monthly essentials—rent, groceries, transport, insurance, and debt payments—then multiply by three for a starter emergency fund. If you spend $2,500 monthly, aim for $7,500 in a high-yield savings account. Platforms like Moomoo offer up to 8.1% APY for new users on uninvested cash in 2026.

Step 2: Choose and Open the Right Account

Open a brokerage account—it's simple and often free. For retirement-focused investing, prioritize tax-advantaged options:

- Roth IRA: Contribute up to $7,000 in 2026 (or $8,000 if 50+). Earnings grow tax-free if rules are met. Ideal for beginners under income limits.

- Traditional IRA: Tax-deductible contributions now, taxed later.

- Brokerage Account: No contribution limits or income rules, perfect for flexibility.

- 401(k): If your employer offers one, max the match—it's free money.

Popular beginner-friendly brokers include Vanguard, Fidelity, Charles Schwab, and SoFi—no minimums for many S&P 500 funds.

Step 3: Pick Your S&P 500 Fund

Select a low-cost ETF or index fund tracking the S&P 500. Expense ratios under 0.05% keep more money invested. Here's a comparison of top 2026 options with no or low minimums:

| Fund | Ticker | Expense Ratio | Minimum | Why It's Great |

|---|---|---|---|---|

| Vanguard S&P 500 ETF | VOO | 0.03% | None | Largest fund, tracks precisely. |

| SPDR S&P 500 ETF Trust | SPY | 0.09% | None | Oldest ETF, high liquidity. |

| iShares Core S&P 500 ETF | IVV | 0.03% | None | Backed by BlackRock, reliable. |

| Schwab S&P 500 Index Fund | SWPPX | 0.02% | None | Lowest cost, no minimum. |

| Vanguard 500 Index Fund Admiral | VFIAX | 0.04% | $3,000 | Great for lump sums over minimum. |

ETFs trade like stocks all day; mutual funds at end-of-day prices. Start with VOO or IVV for your $1,000—they're ETF staples.

Step 4: Fund Your Account and Buy Shares

Link your bank, transfer $1,000, and place a buy order. Use dollar-cost averaging: Invest $200 weekly over five weeks to smooth volatility—buy more shares when prices dip. In SoFi or similar apps, choose dollar amounts (fractional shares) for precision.

Step 5: Automate and Diversify Later

Set recurring deposits to build habits. Once comfortable, add international or bond ETFs for balance, but keep 70-80% in S&P 500 for growth.

Key Strategies for Long-Term Success

Dollar-Cost Averaging: Your Volatility Shield

Invest fixed amounts regularly, regardless of market highs or lows. This buys more shares cheaply during dips, boosting returns over time without timing the market.

Avoid Common Beginner Mistakes

- Don't pick individual stocks—it's riskier than broad S&P 500 exposure.

- Ignore short-term news; focus on 5-10+ year horizons.

- Rebalance annually, but minimize trading to cut taxes and fees.

For taxes, hold in IRAs to defer gains. In taxable accounts, long-term capital gains rates (0-20%) apply after one year.

2026 Market Outlook for S&P 500 Investors

Analysts predict strong growth from productivity gains and policy easing, favoring S&P 500 trackers. AI themes persist, but diversification via broad indices reduces risk. With inflation cooling, real returns could shine brighter.

Next Steps to Launch Your Investment

1. Check your budget—ensure 3x monthly expenses saved.

2. Open a Roth IRA or brokerage at Vanguard/Fidelity/Schwab.

3. Deposit $1,000 and buy VOO or SWPPX.

4. Automate $50-100 monthly contributions.

5. Track quarterly, ignore daily noise.

Your first $1,000 is the spark—consistent action turns it into financial freedom. Start today; the market rewards patience.

Frequently Asked Questions

Sources & References

-

1

How to Invest in the S&P 500 (for Beginners) in 2026 - YouTube — www.youtube.com

- 2

-

3

The Best S&P 500 Index Funds and How to Start Investing — nerdwallet.com — www.nerdwallet.com

- 4

-

5

Best Index Funds In 2026 | Bankrate — bankrate.com — www.bankrate.com

-

6

How to start investing in 2026 - a comprehensive guide — investengine.com — blog.investengine.com

-

7

Investment Directions 2026 Outlook | iShares — ishares.com — www.ishares.com

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...