What Is an HSA (Health Savings Account) and How Does It Work?

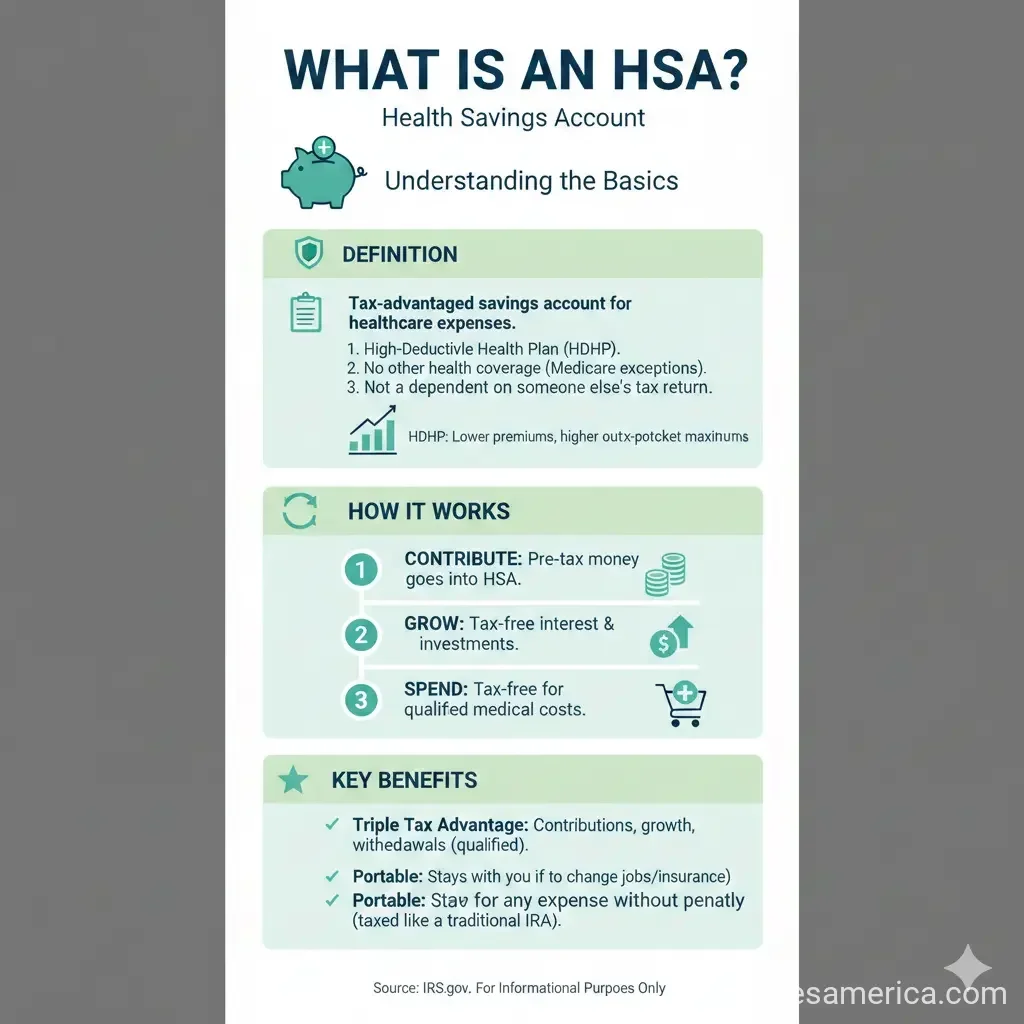

A Health Savings Account (HSA) is a powerful tax-advantaged tool that lets you set aside pre-tax money to pay for qualified medical expenses while building long-term savings for healthcare costs. If y...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

A Health Savings Account (HSA) is a powerful tax-advantaged tool that lets you set aside pre-tax money to pay for qualified medical expenses while building long-term savings for healthcare costs. If you're enrolled in a high-deductible health plan, an HSA can help you reduce your taxable income, earn interest tax-free, and withdraw funds penalty-free for medical expenses. With expanded eligibility rules in 2026, more Americans than ever can now take advantage of this triple-tax benefit.

Understanding the Basics of an HSA

An HSA is a federally tax-deductible savings account that works alongside an HSA-eligible high-deductible health plan (HDHP). Think of it as your personal healthcare savings account—you contribute pre-tax dollars, the money grows tax-free, and you can withdraw it tax-free for qualified medical expenses.

The key advantage is the triple-tax benefit:

- Your contributions are tax-deductible or made with pre-tax dollars

- Interest earned on your account balance is tax-free

- Withdrawals for qualified medical expenses are tax-free

Unlike flexible spending accounts (FSAs) that require you to "use it or lose it," HSA funds roll over indefinitely. Your money stays in the account year after year, making it an excellent long-term healthcare investment.

What Health Plans Qualify for an HSA?

To contribute to an HSA, you must be enrolled in an HSA-eligible health plan. As of 2026, your options include:

- Bronze or Catastrophic plans purchased through the health insurance Marketplace (exchange)

- Traditional high-deductible health plans that meet IRS guidelines with minimum deductibles and out-of-pocket caps

This expansion under the "One Big Beautiful Bill Act" (OBBBA) significantly broadened HSA eligibility starting in 2026, making it easier for Americans to qualify.

2026 HDHP Requirements

If you're considering an HSA-eligible plan for 2026, here are the IRS requirements:

- Minimum annual deductible: $1,700 for self-only coverage or $3,400 for family coverage

- Out-of-pocket maximum (including deductible): $8,500 for self-only coverage or $17,000 for family coverage

Your health plan must also not pay for any non-preventive services before your deductible is met.

HSA Contribution Limits for 2026

The IRS sets annual limits on how much you can contribute to an HSA. For 2026, the contribution limits are:

- Self-only coverage: $4,400 per year

- Family coverage: $8,750 per year

You can make contributions until the tax filing deadline (roughly April 15 of the following year), just like IRAs. If you're 55 or older, you can make an additional "catch-up" contribution of $1,000 per year.

What Can You Use HSA Funds For?

HSA funds can cover a wide range of qualified medical expenses. You can use pre-tax savings to pay for:

- Doctor visits and hospital costs

- Deductibles, copayments, and coinsurance

- Prescription drugs

- Acupuncture

- Ambulance services

- Hearing aids

- Psychological therapy and psychiatric care

- Qualified long-term care services

You can also spend HSA funds on similar medical expenses for your spouse or dependents.

Important note: Health insurance premiums generally aren't considered qualified medical expenses, with some exceptions like COBRA continuation coverage or premiums while receiving unemployment benefits.

Who Can Contribute to an HSA?

To be eligible to contribute to an HSA, you must meet all of these requirements:

- Be enrolled in an HSA-eligible health plan

- Not be enrolled in any other non-HSA-eligible health plan

- Not have a general-purpose health care flexible spending account (FSA)

- Not be enrolled in Medicare

- Not be claimed as a dependent on someone else's tax return

If you're self-employed, you can still contribute to an HSA as long as you have an eligible health plan.

How to Open and Manage Your HSA

HSAs are offered through banks, credit unions, and other financial institutions. When you enroll in an HSA-eligible health plan, your insurance provider will help you set up an account or direct you to available HSA providers.

Once opened, you can:

- Make contributions through payroll deduction (pre-tax)

- Make direct contributions and claim a deduction on your tax return

- Earn interest on your account balance

- Invest your HSA funds in certain investment options (depending on your provider)

- Carry over unused funds indefinitely

Your HSA is administered by a trustee or custodian, and importantly, you own the account and keep it even if you change jobs or retire.

HSA vs. Health Care FSA: What's the Difference?

While both HSAs and health care FSAs let you use tax-advantaged dollars for medical expenses, they work differently:

| Feature | HSA | Health Care FSA |

|---|---|---|

| Requires HDHP | Yes | No |

| Funds roll over | Yes, indefinitely | No (use-it-or-lose-it) |

| Ownership | You own it | Employer owns it |

| Portability | Yours to keep when changing jobs | Stays with employer |

| 2026 Contribution Limit | $4,400 (self) / $8,750 (family) | $3,300 |

You can actually contribute to both an HSA and a health care FSA, but your FSA must be "HSA-compatible," meaning it's a limited-purpose FSA that covers only specific expenses like vision or dental care.

New HSA Changes in 2026

The One Big Beautiful Bill Act brought significant changes to HSA eligibility and benefits starting in 2026:

- Expanded plan eligibility: Bronze and Catastrophic plans from the health insurance Marketplace now qualify for HSA contributions

- Direct primary care options: Individuals enrolled in certain direct primary care (DPC) service arrangements may now contribute to an HSA

- Broader access: More Americans can now take advantage of HSA tax benefits, even if they don't have a traditional HDHP

These changes make HSAs more accessible for people seeking affordable healthcare coverage through the Marketplace.

Making the Most of Your HSA

An HSA is more than just a way to pay for immediate medical expenses—it's a powerful long-term savings tool. Here's how to maximize its benefits:

- Contribute the maximum: If you can afford it, contribute the full annual limit to build your healthcare nest egg

- Pay out-of-pocket when possible: Consider paying for current medical expenses with after-tax dollars and letting your HSA grow through investments

- Keep receipts: Save documentation of medical expenses; you can withdraw HSA funds tax-free for past qualified expenses even years later

- Invest strategically: If your HSA offers investment options and you don't need the funds immediately, consider investing for long-term growth

- Plan for retirement: Your HSA can become a valuable healthcare fund in retirement when medical expenses typically increase

Next Steps

If you're interested in opening an HSA, start by reviewing your current health insurance options. Check whether your plan qualifies as HSA-eligible—especially if you're shopping on the health insurance Marketplace, since Bronze and Catastrophic plans now qualify as of 2026. Once you've enrolled in an eligible plan, your insurance provider can direct you to HSA providers. Consider working with a tax professional to understand how an HSA fits into your overall financial and tax strategy.

For more information about HSA options available through the Marketplace, visit HealthCare.gov or contact your state's health insurance marketplace directly.

Frequently Asked Questions

Sources & References

-

1

What is a health savings account (HSA)? - Healthinsurance.org — www.healthinsurance.org

- 2

- 3

-

4

HSA contribution limits 2025 and 2026 - Fidelity Investments — www.fidelity.com

- 5

-

6

Key changes to HSAs and (potentially) HRAs in 2026 and beyond - HealthEquity — blog.healthequity.com

Useful Tools

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...