What Happens to Your 401(k) If You Change Jobs?

Changing jobs is a big step in your career, but it doesn't have to derail your retirement savings. Your 401(k) from your old employer stays intact, giving you several smart options to keep growing you...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Changing jobs is a big step in your career, but it doesn't have to derail your retirement savings. Your 401(k) from your old employer stays intact, giving you several smart options to keep growing your nest egg without missing a beat.

Whether you're climbing the corporate ladder, switching industries, or chasing a better work-life balance, understanding what happens to your 401(k) if you change jobs is crucial for Americans planning for a secure retirement. In 2026, with contribution limits rising to $24,500 for 401(k) plans, it's an ideal time to review your strategy. This guide breaks down your choices, tax implications, and practical steps tailored to U.S. workers.

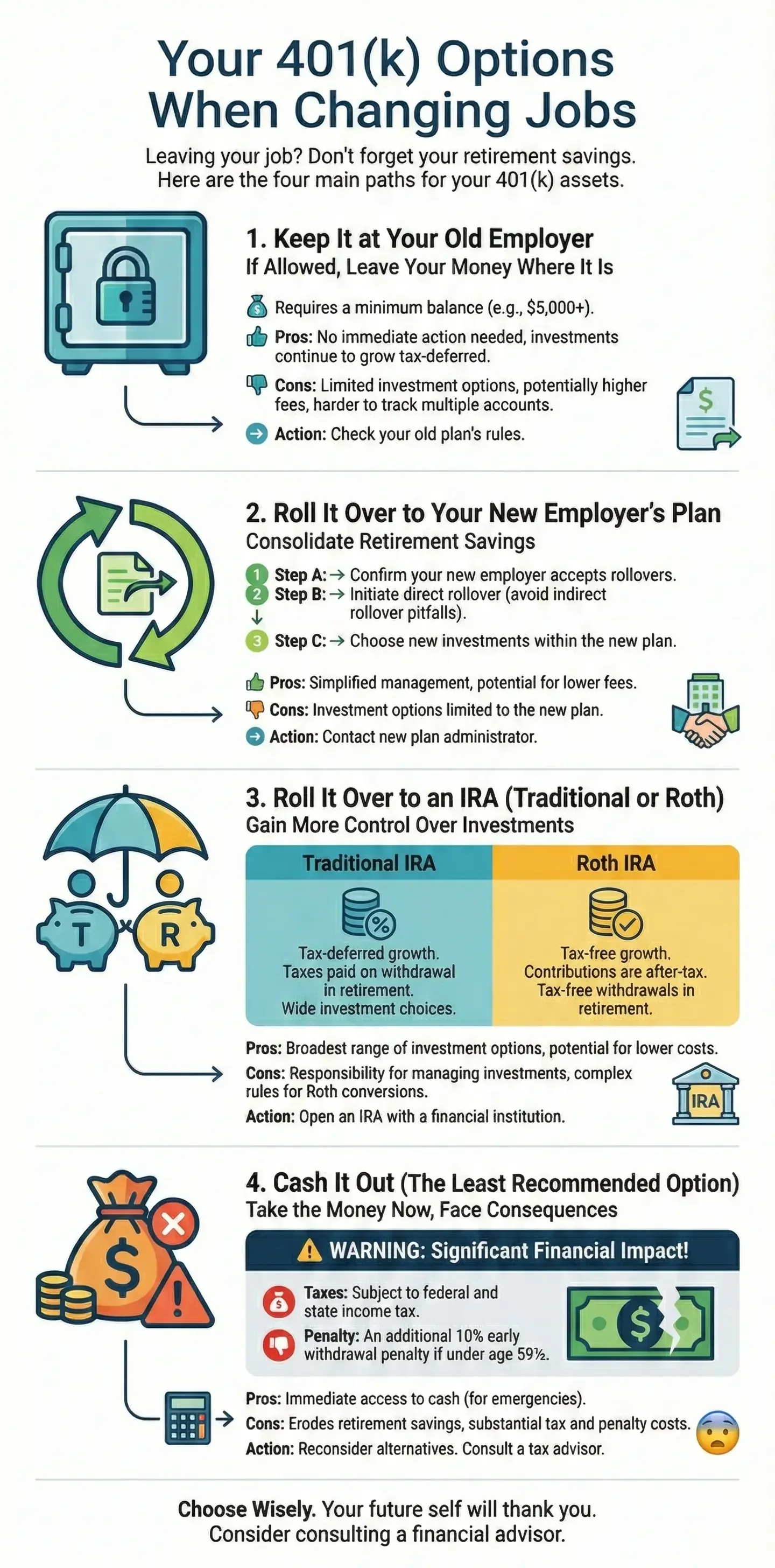

Your 401(k) Options When Leaving a Job

When you leave a job, your 401(k) balance doesn't vanish—it's protected under federal law. Employers can't seize it, and it continues to grow based on your investment choices. Here's what you can do:

1. Leave It Where It Is (Cash-Out Not Recommended)

The simplest choice: do nothing. Your old 401(k) remains with your former employer's plan, managed by the provider like Fidelity or Vanguard. Investments keep earning returns, and you're still the owner.

- Pros: No immediate taxes or fees; stays invested for compound growth.

- Cons: Limited investment options; forgotten accounts risk high fees; no new contributions possible.

Many Americans leave small balances (under $1,000) behind, but check your plan's rules—some auto-rollovers kick in for balances under $7,000 to avoid orphan plans.

2. Roll It Over to Your New Employer's 401(k)

Transfer your old 401(k) directly into your new job's plan. This consolidates accounts, simplifies tracking, and lets you resume contributions right away.

- Pros: One login for all savings; potential for better matching at the new job; creditor protection under ERISA.

- Cons: New plan might charge higher fees or limit investments; not all plans accept rollovers.

In 2026, combining plans means you can hit the $24,500 employee limit across both without double-counting.

3. Roll It Over to an IRA (Often the Best Choice)

A direct rollover to a Traditional IRA (or Roth IRA if converting) gives you full control. Open an IRA with providers like Charles Schwab or Fidelity, and move funds tax-free.

- Pros: Thousands of investment options; lower fees; easier consolidation; Roth conversion for tax-free growth.

- Cons: Loses some 401(k) protections; must handle paperwork yourself.

IRAs shine for long-term growth—2026 IRA limits are $7,500 ($8,600 with catch-up), complementing your new 401(k).

4. Cash Out (Avoid If Possible)

You can withdraw the money, but Uncle Sam takes a big bite: 20% federal withholding upfront, plus 10% early penalty if under 59½, and state taxes. A $50,000 cash-out might net just $30,000 after taxes—losing decades of growth.

Real example: Cashing out $100,000 at age 40 with 7% annual returns could cost you over $760,000 by age 65.

Step-by-Step: How to Handle Your 401(k) Rollover

Moving funds is straightforward but requires care to avoid taxes. Always use a direct rollover—never receive a check yourself.

- Contact your old plan administrator for a rollover form. Confirm balance and fees.

- Open a new account: IRA at Vanguard or new 401(k) via HR.

- Request direct transfer: Funds go straight from old to new custodian.

- Verify receipt: Check statements; it takes 2-4 weeks.

- Invest wisely: Choose low-cost index funds for your risk tolerance.

Pro tip: Time it near payday to avoid gaps in contributions at your new job.

Tax Rules and Penalties to Watch in 2026

Rollovers are tax-free if direct, preserving your pre-tax status. Indirect rollovers give you 60 days to deposit full amount (including withheld taxes) or face taxes/penalties.

| Option | Tax Impact | Penalty (Under 59½) |

|---|---|---|

| Direct Rollover | None | None |

| Cash-Out | Income tax + 20% withholding | 10% |

| Indirect Rollover (missed) | Full income tax | 10% |

For Roth conversions in 2026, pay taxes now for tax-free withdrawals later—smart if you expect higher brackets in retirement.

2026 Contribution Limits and Job Change Impacts

Job changes don't reset limits; they're annual per person. Max $24,500 employee deferrals across all 401(k)s, plus employer matches up to $72,000 total.

Catch-Up Changes for Age 50+

Those 50+ get $8,000 extra, totaling $32,500. Big update: If you earned $150,000+ in 2025 (FICA wages), 2026 catch-ups must be Roth—after-tax but tax-free later.

"Starting in 2026 higher earners making catch-up contributions to a 401(k) will have to make these contributions to a Roth 401(k)."

Plan ahead: Review 2025 W-2s; adjust if nearing the threshold.

Practical Tips for Americans Changing Jobs

- Consolidate early: Fewer accounts mean less hassle at tax time.

- Check fees: Old plans average 1.5%; IRAs can drop to 0.1%.

- Use employer matches: Free money—new jobs often boost this.

- Hardship exceptions: Loans or withdrawals possible but derail growth.

- Veterans/Small balances: Military spouses get special rollover protections; tiny accounts may roll to Safe Harbor IRA.

Resources: IRS.gov for forms; DOL.gov for fiduciary rules; usa.gov/retirement for planning tools.

Next Steps for Your 401(k)

Don't let a job change pause your retirement progress. Log into your old 401(k) portal today, compare fees, and initiate a direct rollover to an IRA or new plan. Max contributions in 2026—aim for that $24,500 plus catch-up if eligible. Consult a fiduciary advisor via NAPFA.org or use free tools at IRS.gov. Your future self will thank you for these moves toward a worry-free retirement.

Frequently Asked Questions

Sources & References

- 1

-

2

Understanding new Roth 401(k) catch-up rules - Fidelity Investments — www.fidelity.com

-

3

2026 Retirement Plan Contribution Limits (401k, 457(b) & More) — www.missionsq.org

-

4

Navigating New 401(k) Catch-Up Contribution Rules - Brighton Jones — www.brightonjones.com

- 5

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...