Cash-Out Refinance: How It Works and When It Makes Sense

If you're a homeowner sitting on equity, a cash-out refinance might be your ticket to funding major expenses, consolidating debt, or tackling that kitchen renovation you've been dreaming about. This s...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're a homeowner sitting on equity, a cash-out refinance might be your ticket to funding major expenses, consolidating debt, or tackling that kitchen renovation you've been dreaming about. This strategy lets you replace your current mortgage with a larger loan and pocket the difference in cash. But before you dive in, it's important to understand how it works, what it costs, and whether it's the right move for your financial situation.

What Is a Cash-Out Refinance?

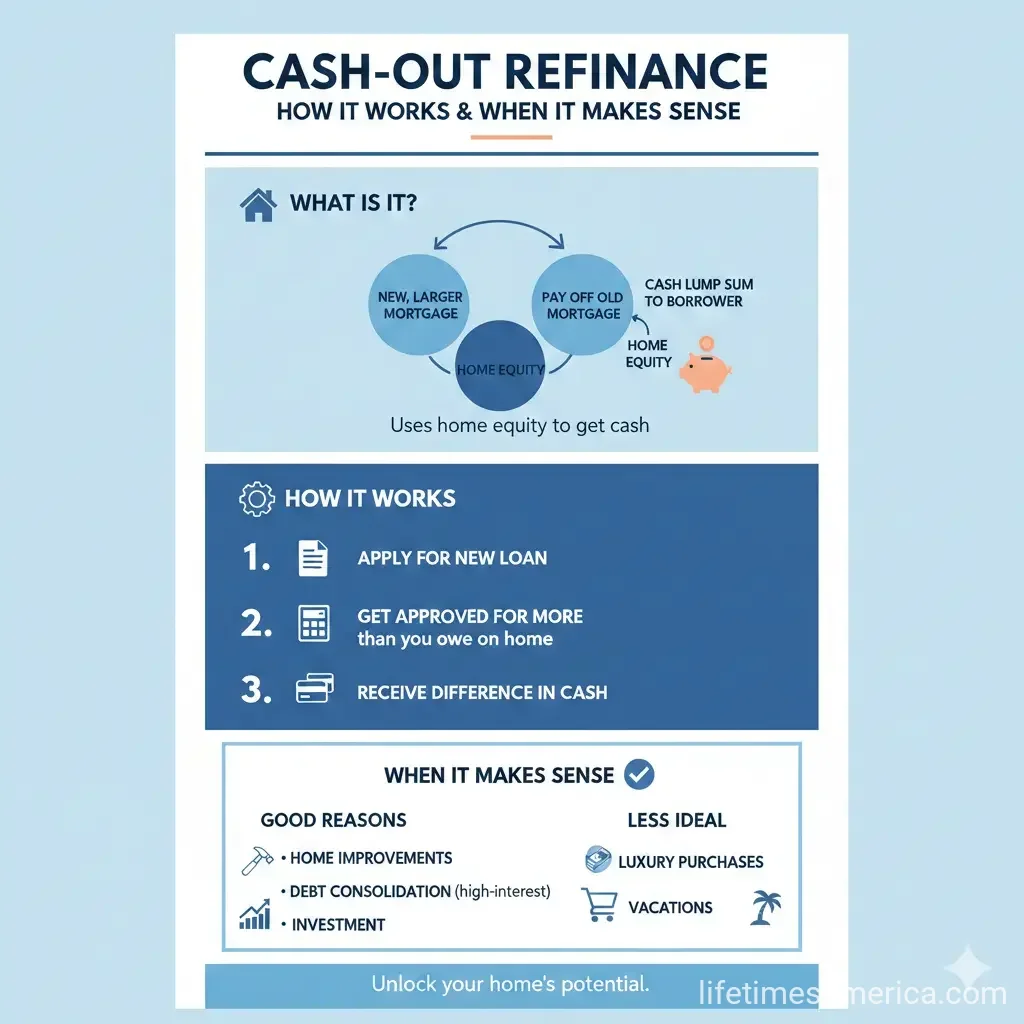

A cash-out refinance replaces your existing mortgage with a new, larger loan. You'll receive the difference between your new loan amount and what you still owe on your current mortgage as a lump sum of cash. This cash comes directly from your home's equity—the difference between what your home is worth and what you owe on it.

Here's a straightforward example: Let's say your home is worth $400,000 and you owe $250,000 on your current mortgage. You have $150,000 in equity. With a cash-out refinance, you might take out a new loan for $320,000. After paying off your existing $250,000 mortgage and closing costs, you'd receive roughly $70,000 in cash.

Unlike a standard refinance (called a "rate-and-term" refi), which simply replaces your existing loan at a new interest rate and term, a cash-out refinance gives you access to cash while also potentially adjusting your interest rate and loan duration.

How the Cash-Out Refinance Process Works

The process is similar to getting your original mortgage, but with a few key steps:

Step 1: Determine Your Available Equity

Your lender will order a professional appraisal to determine your home's current market value. Lenders typically allow you to borrow up to 80% of your home's appraised value for a primary residence, or 75% for investment properties or second homes.

To calculate your maximum loan amount:

- Home value: $400,000

- Maximum loan (80%): $320,000

- Current mortgage balance: $250,000

- Potential cash-out: $70,000 (before closing costs)

Step 2: Apply and Submit Documentation

You'll need to provide proof of income, employment, and financial stability. Be prepared to submit:

- Recent pay stubs

- Tax returns (especially if self-employed)

- W-2s

- Bank statements

- Current mortgage statement

- Proof of homeowner's insurance

Step 3: Get Approved and Review Terms

Your lender will review your financials, credit score, and debt-to-income ratio. Most lenders want to see a debt-to-income ratio of no more than 43% to 50%. You'll receive a loan estimate detailing your new interest rate, loan term, and closing costs before you commit.

Step 4: Close the Loan

Once you've reviewed and accepted the terms, you'll sign the final paperwork at closing. Your new loan will fund after a mandatory 3-day rescission period, during which you can back out if needed.

Step 5: Receive Your Cash

After the rescission period ends, your cash is typically wired directly to your bank account. The entire process from application to funding usually takes 15 to 30 days, though it can extend to 45 days depending on your property's complexity and appraisal timeline.

How Much Cash Can You Actually Get?

Your actual cash-out amount depends on several factors:

Maximum loan amount: Up to 80% of your home's appraised value (for primary residences)

Subtract your current balance: The amount you still owe on your existing mortgage

Subtract closing costs: Expect to pay 2% to 5% of your new loan amount in closing costs

Using our earlier example with a $400,000 home, $250,000 mortgage, and 3% closing costs:

- Maximum loan (80%): $320,000

- Minus current mortgage: -$250,000

- Minus closing costs ($320,000 × 3%): -$9,600

- Net cash received: Approximately $60,400

Good news: The cash you receive from a cash-out refinance isn't taxed. It's a loan against your home's equity, not income.

What Can You Use the Cash For?

One of the biggest advantages of a cash-out refinance is flexibility. You can use the funds for virtually any purpose, including:

- Home improvements and renovations

- Debt consolidation (paying off credit cards or personal loans)

- College tuition or education expenses

- Down payment on a second home

- Emergency expenses or medical bills

- Starting a business

Pros and Cons of Cash-Out Refinancing

Advantages

- Access to large amounts of cash: You can tap into your home equity without selling your home

- Potentially lower interest rates: Home equity loans often have lower rates than credit cards or personal loans

- Flexible use of funds: Use the money for any purpose

- Possible interest rate improvement: If current rates are lower than your original mortgage, you might reduce your overall interest rate

- Debt consolidation opportunity: Combine multiple debts into one monthly payment

Disadvantages

- Increased debt: You're borrowing more money against your home

- Closing costs: Plan on paying 2% to 5% of your new loan amount upfront or rolling them into your loan

- Risk to your home: Your home serves as collateral; failure to pay could result in foreclosure

- Longer loan term: If you extend your loan term to lower monthly payments, you'll pay more interest over time

- PMI if high LTV: If you borrow more than 80% of your home's value, you'll pay mortgage insurance

- Reset amortization schedule: You'll start over with a new 15, 20, or 30-year loan term

When Does a Cash-Out Refinance Make Sense?

A cash-out refinance can be a smart financial move if you meet these criteria:

- You have significant equity: Most lenders want to see at least 15% to 20% equity in your home

- Your credit score is solid: A higher credit score (typically 620+) helps you qualify and get better rates

- Your income is stable: Lenders want to see steady employment and reliable income

- Interest rates are favorable: Ideally, current rates should be competitive with or lower than your current rate, especially if you're extending your loan term

- You have a specific use for the funds: Using the cash for debt consolidation, home improvements, or education typically provides better long-term value than using it for discretionary spending

- Your loan is at least 6 to 12 months old: Most lenders require you to have had your current mortgage for at least 6 to 12 months before allowing a cash-out refi

Cash-Out Refinance vs. Other Options

Before you commit to a cash-out refinance, consider how it compares to other ways to access your home's equity:

| Option | How It Works | Best For |

|---|---|---|

| Cash-Out Refinance | Replaces existing mortgage with larger loan; you get lump sum at closing | Large one-time expenses; potentially lower rates |

| HELOC | Second lien; acts like credit card; draw funds as needed | Ongoing expenses; flexibility; keeping original mortgage |

| Home Equity Loan | Second lien; fixed loan with set payments | Predictable payments; keeping original mortgage |

| Personal Loan | Unsecured debt; no collateral needed | Smaller amounts; don't want to risk home |

Key Takeaways

A cash-out refinance can be a powerful financial tool if you need access to a large amount of cash and you have built-up home equity. It replaces your current mortgage with a larger one, letting you pocket the difference. The process typically takes 15 to 30 days, and you can borrow up to 80% of your home's value (minus what you owe and closing costs).

Before moving forward, make sure you have a clear purpose for the funds, stable income, and a solid credit score. Compare a cash-out refinance to other options like HELOCs or home equity loans to ensure you're choosing the best strategy for your financial goals.

Ready to explore your options? Start by contacting a few lenders to get quotes and loan estimates. This will give you a clear picture of your available cash, interest rates, and closing costs—helping you make an informed decision about whether a cash-out refinance makes sense for you right now.

Frequently Asked Questions

Sources & References

-

1

Cash-Out Refinancing: What It Is, How It Works — Bankrate — www.bankrate.com

-

2

Cash-Out Refinance: What You Need to Know — Navy Federal — www.navyfederal.org

-

3

How to do a Cash Out Refinance in Texas in 2026 — AsertaLoans — www.asertaloans.com

-

4

Cash-Out Refinance | Requirements & Limits 2026 — The Mortgage Reports — themortgagereports.com

-

5

Cash-out refinance | How does it work? — U.S. Bank — www.usbank.com

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...