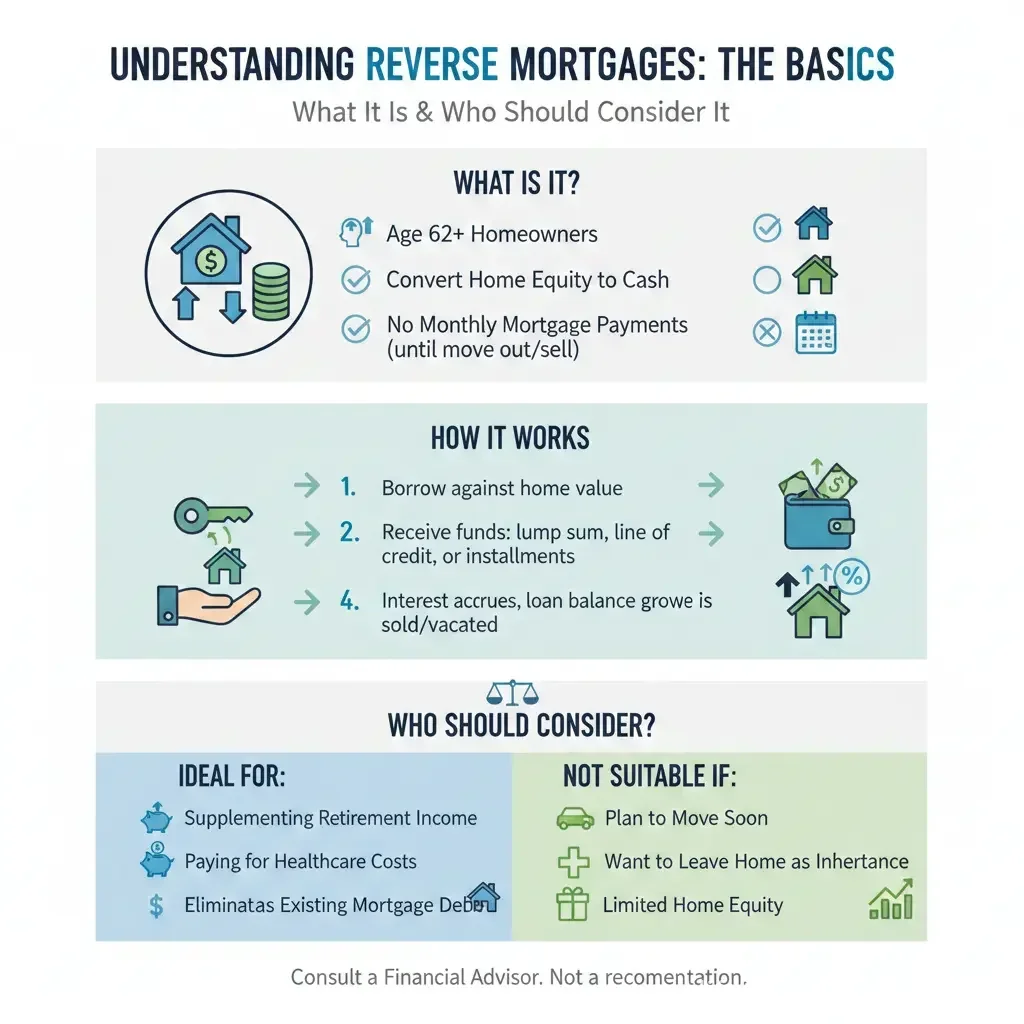

What Is a Reverse Mortgage and Who Should Consider It?

If you're 62 or older and looking for ways to tap into your home's value without selling it, a reverse mortgage might be worth exploring. Unlike traditional mortgages where you make monthly payments,...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're 62 or older and looking for ways to tap into your home's value without selling it, a reverse mortgage might be worth exploring. Unlike traditional mortgages where you make monthly payments, a reverse mortgage flips the script—your lender pays you. This financial tool can provide much-needed cash for retirement expenses, home repairs, or medical bills, but it's not right for everyone. Understanding how reverse mortgages work, what they cost, and whether you qualify is essential before making this significant decision.

Understanding Reverse Mortgages: The Basics

A reverse mortgage is a loan that allows homeowners age 62 or older to borrow against the equity in their home. Instead of making monthly mortgage payments to a lender like you would with a traditional mortgage, the lender makes payments to you. You're essentially converting a portion of your home's equity into cash without having to sell the property.

Here's the key difference: with a forward (traditional) mortgage, you borrow money upfront and pay it back over time. With a reverse mortgage, you receive payments from the lender, and the loan balance grows as interest accrues. The loan becomes due when you sell your home, move out permanently, or pass away.

How Home Equity Works in a Reverse Mortgage

Home equity is simply the difference between what your home is worth and what you still owe on it. For example, if your home is valued at $350,000 and you owe $100,000 on your mortgage, you have $250,000 in equity. However, lenders won't let you borrow against all of your equity—you'll typically be able to borrow a percentage of that amount, leaving some equity in the home.

Most reverse mortgages require that your existing mortgage be paid off first using the loan proceeds. After that's handled, any remaining funds go to you.

How You Receive Your Money

When you take out a reverse mortgage, you have flexibility in how you receive the funds. You can choose to get your money as a:

- Lump sum (all at once)

- Monthly payments

- Line of credit (draw as needed)

- Combination of these options

Your choice depends on your financial needs and preferences. Some people prefer a lump sum for a major expense, while others want steady monthly income to supplement retirement. A line of credit gives you the flexibility to access funds when you need them.

Types of Reverse Mortgages Available

There are three main types of reverse mortgages in the United States:

Home Equity Conversion Mortgages (HECMs)

The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration (FHA). In 2026, the maximum you can borrow with a HECM is $1,249,125. These loans are federally regulated, which provides consumer protections. Eligible properties include single-family homes, HUD-approved condominiums, and manufactured homes that meet FHA standards.

With an HECM, heirs are protected from having to pay back more than the home's value when the loan becomes due. The debt will be either the mortgage balance or 95% of the home's appraised value—whichever is less.

Proprietary Reverse Mortgages

These are private loans not insured by the FHA, typically offered by banks or mortgage companies. They work similarly to HECMs but may have different terms and potentially higher lending limits for expensive homes.

Single-Purpose Reverse Mortgages

These loans are designed for specific purposes like paying property taxes or funding home repairs. They're typically the least expensive option, though they're less commonly available.

Who Qualifies for a Reverse Mortgage?

To qualify for a reverse mortgage, you generally need to meet these requirements:

- Be at least 62 years old

- Own your home outright or have significant equity (typically 50-55% or more)

- Use the home as your primary residence

- Be able to pay property taxes, homeowners insurance, and maintain the home

If you still have a traditional mortgage, the reverse mortgage proceeds will first pay off that existing loan. After that's done, you won't have monthly mortgage payments, which can free up significant cash flow in retirement.

Understanding the Costs and Interest

Reverse mortgages aren't free. Interest and fees are added to your loan balance each month, which means your debt grows over time. As you borrow more money, your home equity decreases.

Interest rates for reverse mortgages can be either variable or fixed. Fixed rates are typically only available for lump-sum payments, while variable rates apply to other payment options. Generally, reverse mortgage interest rates are higher than traditional mortgage rates.

Here's a real-world example: if you own a $500,000 home free and clear and take out a reverse mortgage for $250,000 (50% of the value) at a 10% interest rate, after 10 years you'd owe $676,760. This illustrates how important it is to understand that your debt will grow substantially over time.

When You'll Need to Repay the Loan

Unlike a traditional mortgage with a fixed repayment schedule, a reverse mortgage becomes due when certain events occur:

- You sell the home – The lender requires the loan to be paid off from your sale proceeds

- You move out permanently – If you stop using the home as your primary residence for more than 12 months, repayment is required

- You pass away – The loan becomes due, and your heirs can either sell the home to repay it or make a cash payment

- You fail to meet loan requirements – This could include not paying property taxes or homeowners insurance, or failing to maintain the home

When repayment is due, you or your heirs typically sell the home and use those proceeds to pay back the lender. With federally-insured reverse mortgages, your heirs won't owe more than the home's value, providing important protection.

Who Should Consider a Reverse Mortgage?

A reverse mortgage might be a good fit if you:

- Are 62 or older and want to stay in your home

- Have substantial home equity but limited other retirement income

- Need funds for medical expenses, home repairs, or living expenses

- Want to supplement Social Security or other retirement income

- Don't plan to move or leave the home to your heirs as a major asset

A reverse mortgage is probably not right for you if you:

- Plan to move or sell your home soon

- Want to preserve your home as an inheritance for your children

- Have minimal equity in your home

- Can't afford to maintain the property or pay property taxes

- Receive need-based government benefits that could be affected by additional income

Important Considerations Before You Apply

Impact on Government Benefits

Before taking out a reverse mortgage, understand how it might affect your eligibility for government assistance programs. Depending on how you receive the funds (lump sum, monthly payments, or line of credit), it could impact your Supplemental Security Income (SSI) or Medicaid eligibility. Consult with a benefits counselor before proceeding.

Tax Implications

Reverse mortgage proceeds are generally not considered taxable income, but they may affect your tax situation in other ways. It's wise to discuss this with a tax professional.

Maintenance and Property Obligations

You're still responsible for maintaining the home, paying property taxes, and keeping homeowners insurance current. Failing to do so could trigger early repayment of the loan.

Taking the Next Step

If you're interested in exploring whether a reverse mortgage makes sense for your situation, start by getting educated. Contact a HUD-approved reverse mortgage counselor—this is often required before you can apply anyway. They'll help you understand the pros and cons specific to your circumstances and answer detailed questions about costs and terms.

Compare offers from multiple lenders, ask about all fees and interest rates, and make sure you understand exactly when and how you'll need to repay the loan. A reverse mortgage can be a valuable financial tool in retirement, but only if it aligns with your long-term plans and financial goals.

Frequently Asked Questions

Sources & References

-

1

Rocket Mortgage - What is a Reverse Mortgage? — www.rocketmortgage.com

-

2

AmeriSave - Ultimate Guide to Reverse Mortgages in 2025 — www.amerisave.com

-

3

Fortune - What is a Reverse Mortgage? Everything to Know — fortune.com

-

4

CGP Real Estate Consulting - The 2026 Easy Guide to Reverse Home Mortgages — www.cgprealestateconsulting.com

-

5

The Maryland Peoples Law Center - Reverse Mortgages — www.peoples-law.org

-

6

Nolo - What You Need to Know About Reverse Mortgages in 2026 — www.nolo.com

Useful Tools

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...