Student Loans in the USA: Federal vs Private Explained

Navigating student loans can feel overwhelming, especially when deciding between federal and private options. With total U.S. student debt exceeding $1.7 trillion in 2026, understanding the key differ...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Navigating student loans can feel overwhelming, especially when deciding between federal and private options. With total U.S. student debt exceeding $1.7 trillion in 2026, understanding the key differences helps you borrow smarter and repay easier.

Federal loans offer flexible repayment, forgiveness programs, and borrower protections that private loans often lack. Private loans, while sometimes necessary, come with stricter terms and higher risks. This guide breaks down student loans in the USA: federal vs private explained, with 2026 updates, so you can make informed choices.

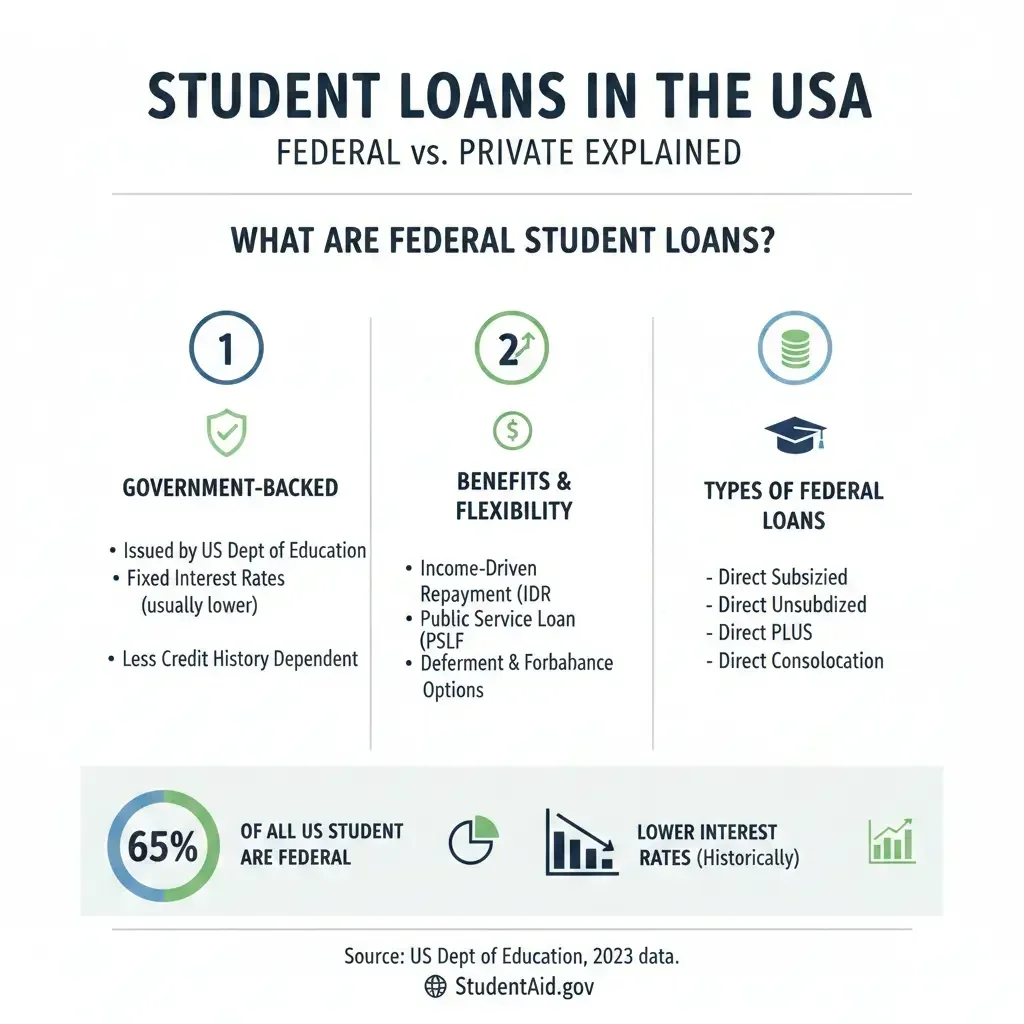

What Are Federal Student Loans?

Federal student loans are funded by the U.S. Department of Education and provide the most accessible financing for college. They're available through the Free Application for Federal Student Aid (FAFSA) and include Direct Subsidized Loans (for undergrads with financial need), Direct Unsubsidized Loans (for undergrads and grads), Direct PLUS Loans (for parents and grad students), and Direct Consolidation Loans.

In 2026, major changes from the One Big Beautiful Bill Act reshape federal loans. Starting July 1, new borrowers face only two repayment plans: a standard plan or the Repayment Assistance Plan (RAP). Graduate PLUS Loans are eliminated for new borrowers, and loan limits now include annual and lifetime caps for grad/professional students and Parent PLUS borrowers.

Key Benefits of Federal Loans

- Lower, fixed interest rates: For 2026-2027, undergrad Direct Subsidized/Unsubsidized rates start at 5.50%, with grad rates up to 7.05%—far below many private options.

- Income-driven repayment (IDR) plans: Payments based on 10-20% of discretionary income, with forgiveness after 20-25 years.

- No credit check: Eligibility based on FAFSA, not credit score (except PLUS loans).

- Protections: Deferment, forbearance, and disability discharge options, though limited post-2026.

What Are Private Student Loans?

Private student loans come from banks, credit unions, or online lenders like Citizens Bank or SoFi. They're credit-based, often requiring a cosigner, and fill gaps after exhausting federal aid.

Unlike federal loans, private options don't qualify for government forgiveness or IDR. Interest rates vary widely—fixed from 4% to 15% or variable up to 18%—depending on credit. In 2026, with federal limits tightening, more students may turn to private loans, but experts caution against it due to risks.

Key Features of Private Loans

- Higher borrowing limits: Up to full cost of attendance, no federal caps.

- Variable or fixed rates: Can start lower but rise with market changes.

- Cosigner release possible: After 24-48 on-time payments.

- Fewer protections: Limited deferment; refinancing may lower rates but forfeits federal benefits.

Federal vs Private Student Loans: Side-by-Side Comparison

Here's a clear breakdown to highlight why federal loans are usually first choice for most Americans.

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Interest Rates (2026) | Fixed: 5.50%-8.05% | Fixed/Variable: 4%-18% (credit-based) |

| Forgiveness Options | Yes: PSLF, IDR, Teacher Loan Forgiveness | No federal programs |

| Repayment Plans | Standard, IDR (RAP post-2026) | Lender-specific; no IDR |

| Credit Check | No (except PLUS) | Yes, often needs cosigner |

| Deferment/Forbearance | Limited post-2026 (9 months max/2 years) | Lender-dependent |

| 2026 Changes | Fewer plans, no Grad PLUS, caps | Unaffected, but refinancing risks |

Federal Loan Repayment and Forgiveness Options in 2026

Federal loans shine in repayment flexibility. Over $183 billion in debt has been forgiven via programs like PSLF and IDR.

Public Service Loan Forgiveness (PSLF)

PSLF forgives Direct Loans after 120 qualifying payments (10 years) while working full-time for government or nonprofits. Over 7 million borrowers pursue it, but thousands face delays in 2026 due to buyback processing—where you "buy back" deferment months.

2026 Updates: New rules effective July 1 limit eligibility; parent loans no longer qualify, and the Department can disqualify employers with "substantial illegal purpose." Tax-free through 2025, but PSLF forgiveness remains nontaxable post-2025.

Income-Driven Repayment (IDR) Forgiveness

- IBR: Forgiveness after 20-25 years; eligible for Direct, FFEL, Perkins.

- PAYE: 20 years for new borrowers; no new apps post-changes.

- ICR: 25 years; limited to consolidated parent PLUS.

Post-2026, RAP replaces most IDR for new borrowers.

Other Federal Forgiveness

- Teacher Loan Forgiveness: Up to $17,500 for low-income schools.

- Total/Permanent Disability Discharge.

- SCRA: Caps interest at 6% for active military.

- NHSC Loan Repayment: Up to full repayment for health professionals in underserved areas (apps open through March 2026).

Private Loan Repayment: What to Expect

Private loans lack federal perks, so focus on shopping rates. Refinancing into a private loan can lower payments but ends forgiveness eligibility—avoid if pursuing PSLF.

Practical Tip: Use federal loans first (up to limits), then private only if needed. Track via StudentAid.gov.

2026 Changes: How They Impact Your Loans

New federal rules hit July 1, 2026:

- No economic hardship deferments for loans after July 1, 2027.

- Forbearance capped at 9 months/2 years.

- PSLF tweaks: Stricter employer rules, no parent loans.

- IDR forgiveness may become taxable (except PSLF).

- New RAP plan for income-based payments.

Actionable Advice: Existing borrowers—consolidate now for PSLF. New borrowers—max federal aid, minimize private debt.

Practical Tips for Managing Student Loans

- Complete FAFSA annually: Access federal grants/loans first.

- Choose Direct Loans: Only these qualify for PSLF without consolidation.

- Enroll in IDR early: Use StudentAid.gov calculator.

- Track PSLF payments: Submit Employment Certification Form yearly.

- Avoid private unless essential: Compare via Credible or NerdWallet.

- Prepare for taxes: Forgiven amounts may be taxable in 2026.

Next Steps to Tackle Your Student Loans

Log into StudentAid.gov to review loans, certify PSLF employment, or switch to IDR/RAP. Use the Loan Simulator tool for personalized plans. If in public service, apply for buybacks before delays worsen. Consult a financial advisor or non-profit credit counselor via NFCC.org. Borrowing wisely today sets you up for debt-free tomorrow—start with federal, stay informed on 2026 changes.

Frequently Asked Questions

Sources & References

-

1

Student-loan borrowers in public service are in a growing debt relief bind — www.businessinsider.com

-

2

143 Student Loan Forgiveness Programs (2025) — educationdata.org

-

3

A Complete List of Student Loan Forgiveness Programs — www.credible.com

-

4

Update on Federal Loan Changes Beginning in 2026 — financialaid.tcnj.edu

-

5

Loan Forgiveness and Discharge Programs - StudentAid.gov — mohela.studentaid.gov

-

6

Public Service Loan Forgiveness — finaid.org

-

7

Federal Student Loans in 2026: What the One Big Beautiful Bill Act Affects — www.citizensbank.com

-

8

NHSC Loan Repayment Program — nhsc.hrsa.gov

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...