Fixed-Rate vs Adjustable-Rate Mortgage: Which Is Better?

Imagine locking in your dream home only to watch your monthly mortgage payment skyrocket a few years later—or securing a low rate today that stays put through decades of family milestones. That's the...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine locking in your dream home only to watch your monthly mortgage payment skyrocket a few years later—or securing a low rate today that stays put through decades of family milestones. That's the high-stakes choice between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). In 2026's market, with rates hovering near three-year lows, understanding these options is crucial for American homebuyers and refinancers aiming to save thousands over time.

Fixed-rate mortgages offer unchanging payments, while ARMs start lower but can fluctuate. We'll break down the differences, pros, cons, current rates, and real-world scenarios to help you decide which fits your life—whether you're a first-time buyer in Texas, a growing family in California, or eyeing a refinance via FHA or VA loans.

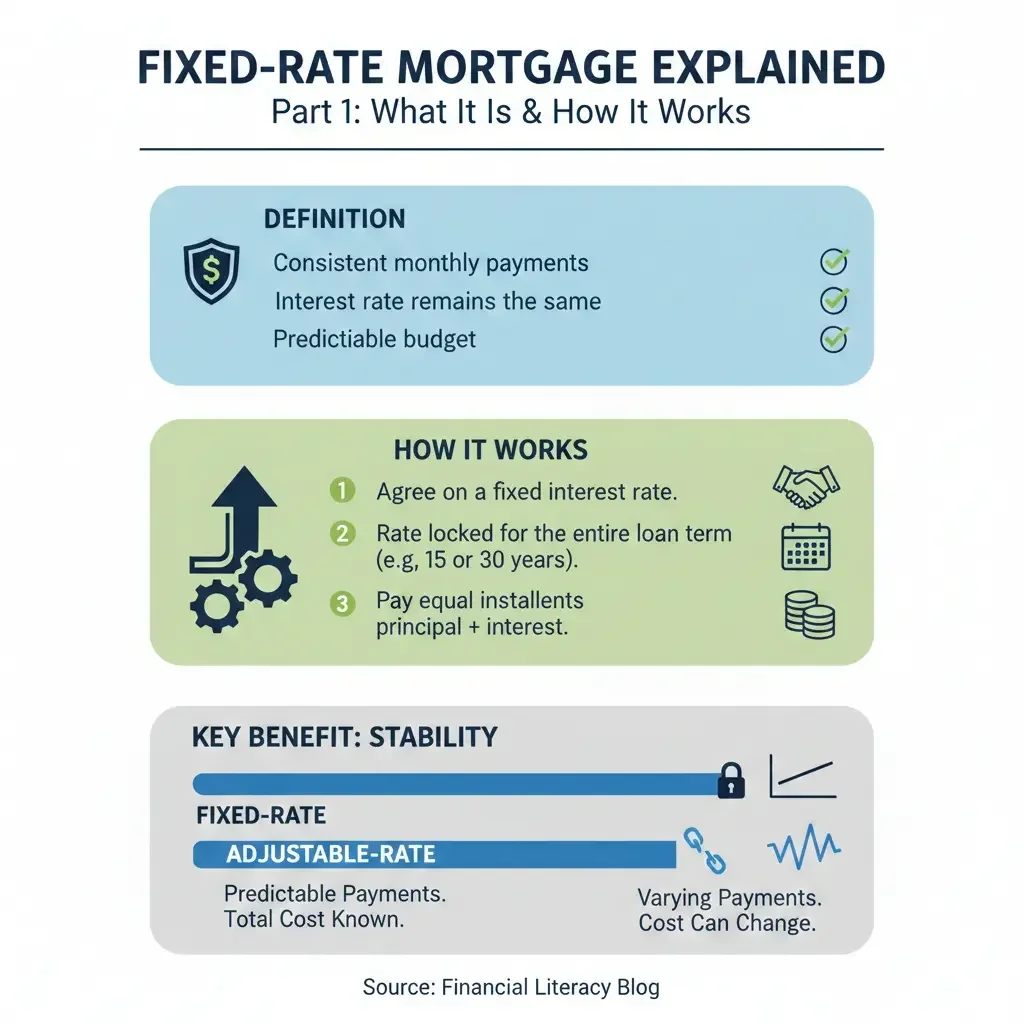

What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage keeps your interest rate—and thus your principal and interest payment—the same for the entire loan term, typically 15 or 30 years. This predictability shields you from market shifts, Federal Reserve decisions, or inflation spikes.

Key Features of Fixed-Rate Loans

- Term lengths: Common options include 15-year (lower rates, higher payments) and 30-year (more affordable monthly costs).

- Stability: No surprises—your budget stays steady even if rates rise to 7% or higher.

- Popularity: They make up about 92% of U.S. home loans, thanks to their reliability.

As of February 19, 2026, the national average 30-year fixed rate is around 6.01%–6.18%, down from last week, while 15-year fixed averages 5.42%–5.56%. For FHA loans, expect about 6.10%, and VA loans around 6.11%—ideal for eligible veterans or low-down-payment buyers.

What Is an Adjustable-Rate Mortgage (ARM)?

An ARM starts with a fixed introductory rate for a set period (e.g., 5, 7, or 10 years), then adjusts periodically based on an index like SOFR plus a margin. The "5/1" label means fixed for 5 years, then annual adjustments; "7/6" means 7 years fixed, then every 6 months.

How ARM Adjustments Work

- Initial teaser rate: Often 0.4%–0.6% lower than fixed loans, easing qualification.

- Caps protect you: Federal regulations limit increases—typically 2% per adjustment, 5% lifetime—to prevent extreme "payment shock."

- Adjustment triggers: Tied to market rates; if they fall, your payment could drop too.

Current 2026 ARM rates are attractive: 5/1 ARMs average 5.36%–6.21%, 7/6 ARMs from major lenders like Bank of America at 5.250% interest (6.017% APR), U.S. Bank at 5.375%–5.500%, and Zillow at 5.500%–5.625%.

Fixed-Rate vs Adjustable-Rate Mortgage: Head-to-Head Comparison

Neither is universally "better"—it depends on your timeline, risk tolerance, and plans. Fixed suits long-term stability; ARMs favor short-term affordability. Here's a 2026 market snapshot:

| Feature | 30-Year Fixed | 7/6 or 10/6 ARM |

|---|---|---|

| Typical Rate (Feb 2026) | 6.01%–6.18% | 5.25%–5.91% (intro) |

| Payment Stability | Lifetime fixed | Fixed 7–10 years, then variable |

| Risk Level | Zero rate risk | Moderate post-intro |

| Best For | Forever homes, 10+ years | Relocations, refinances in <10 years |

Monthly Payment Example

On a $300,000 loan:

- 30-year fixed at 6.18%: ~$1,828/month.

- 7/6 ARM at 5.25% intro: ~$1,657/month—saving $171 initially, but could rise later.

Pros and Cons: Fixed-Rate Mortgages

Pros

- Total predictability for budgeting and long-term planning.

- Protection from rate hikes amid 2026 inflation concerns.

- Easier mental peace—no watching market news.

Cons

- Higher starting rate than ARMs (e.g., 0.5%+ more).

- Miss out if rates drop (refinance needed).

- Less affordable upfront for some budgets.

Pros and Cons: Adjustable-Rate Mortgages

Pros

- Lower intro rates boost buying power—qualify for bigger homes.

- Potential savings if rates fall post-adjustment.

- Flexibility for moves or refinances before adjustments.

Cons

- Payment uncertainty after intro period.

- Risk of sharp increases if rates rise.

- Not ideal for long-term stays without refinancing.

Which Is Better for You? Real Scenarios for Americans

Choose fixed if: You're settling in for 10+ years, like families in stable suburbs. With 92% market share, it's the default for peace of mind.

Choose ARM if: Planning a job move, upsizing soon, or flipping in hot markets like Florida. Short-term savers thrive here.

Run numbers with the CFPB's mortgage calculator at consumerfinance.gov. Factor in property taxes, insurance, and HOA fees. For low-income buyers, explore FHA ARMs or USDA loans via hud.gov.

Refinancing? 2026's near three-year lows make it timely—check eligibility on irs.gov for deductions.

Current 2026 Mortgage Rates and Trends

Rates edged up slightly but remain low: 30-year fixed at 6.01%, ARMs starting under 5.5%. Fed moves and labor strength keep them contained—watch Freddie Mac weekly updates.

Next Steps: Make Your Best Mortgage Choice

Compare quotes from at least three lenders today—use tools at usa.gov. Pre-approve to strengthen offers, and consult a HUD-approved counselor for free advice. Whether fixed for security or ARM for savings, align with your 5–10 year horizon to potentially save $50,000+ in interest. Start calculating now and own your future confidently.

Frequently Asked Questions

Sources & References

-

1

Mortgage Rates Rise | Today, February 17, 2026 — themortgagereports.com

-

2

Current refi mortgage rates report for Feb. 19, 2026 — fortune.com

-

3

ARM vs. Fixed-Rate Mortgage: 2026 Comparison & KC Guide — www.emetropolitan.com

- 4

-

5

Current ARM mortgage rates report for Feb. 18, 2026 — fortune.com

-

6

Current ARM mortgage rates report for Feb. 19, 2026 — fortune.com

-

7

Compare Today's Mortgage Rates | Thursday, February 19, 2026 — www.nerdwallet.com

-

8

Mortgage Rates Steady | Today, February 19, 2026 — themortgagereports.com

-

9

Current ARM Mortgage Rates | Bankrate — www.bankrate.com

-

10

Mortgage Rates - Freddie Mac — www.freddiemac.com

Useful Tools

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...