How to Improve Your Credit Score Fast

Struggling with a low credit score can feel like a roadblock to everything from buying a home to landing that apartment lease. The good news? You can take concrete steps right now to boost it quickly—...

Struggling with a low credit score can feel like a roadblock to everything from buying a home to landing that apartment lease. The good news? You can take concrete steps right now to boost it quickly—often seeing results in as little as 30 days—by focusing on proven strategies tailored for Americans in 2026.Improving your credit score fast is about smart, actionable moves like paying down balances and fixing errors, helping you unlock better loan rates and financial freedom sooner.

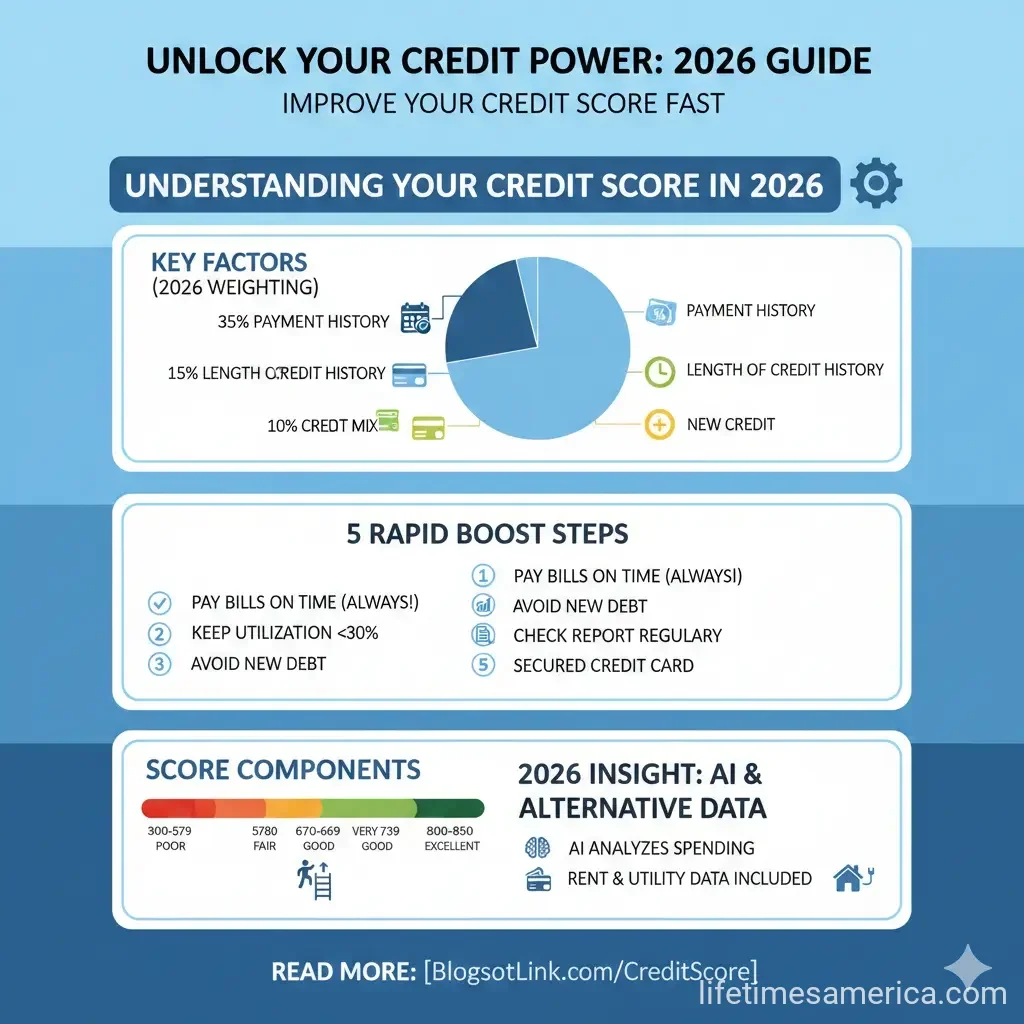

Understanding Your Credit Score in 2026

Before diving into fixes, know what drives your score. FICO and VantageScore models—used by most U.S. lenders—prioritize payment history (35%), amounts owed or credit utilization (30%), length of credit history (15%), new credit (10%), and credit mix (10%).[3][6] In 2026, updates like Buy Now, Pay Later (BNPL) reporting and reduced impact from small medical debts under $500 mean on-time payments and low utilization remain king.[6]

Check your free weekly reports at AnnualCreditReport.com, authorized by federal law for Americans. Spotting issues early can prevent fraud and speed up improvements.[6]

Top Ways to Improve Your Credit Score Fast

Focus on high-impact actions for quick wins. A 100-point jump is rare but possible with errors fixed or high balances paid down; aim for 30-60 points monthly through consistency.[1]

1. Pay Bills on Time—Every Time

Payment history is the biggest factor. Set up auto-pay for at least the minimum on credit cards and loans via your bank app. Pay a few days early around holidays when banks close.[2][4] Use phone reminders or bank email alerts. Even one late payment hurts, but months of on-time ones build it back fast.[1]

- Enroll in automatic bill pay with providers like your credit union.

- Track due dates in a calendar app.

- Prioritize high-interest cards first.

2. Lower Your Credit Utilization Below 30%

Keep balances under 30% of your limits—ideally under 10% for top scores. If you have $10,000 total limits and owe $4,000, pay down to $3,000 or less.[1][4] Pay cards multiple times a month before statements close; scores update quickly.[1]

Request higher limits on existing cards (without hard inquiries) or add a card—but don't spend more. Example: Boosting from $30,000 to $36,000 total limits drops utilization from 37% to 31% instantly.[2]

3. Dispute Errors on Your Credit Reports

Errors like wrong late payments or duplicate accounts can tank your score. File free disputes online with Equifax, Experian, and TransUnion—they must investigate in 30-45 days.[1] Use their portals or mail certified letters. removals can cause fast jumps.[1][5]

"A mistake on one of your credit reports can lower your score. Disputing errors...can help you quickly improve your credit."[1]

4. Pay Off or Reduce High Balances Strategically

Tackle revolving debt first. Stop using cards temporarily, pay high-interest ones aggressively, and maintain minimums elsewhere. Zero balances monthly avoids interest and keeps utilization low.[3] For debt snowball fans, list cards by balance and crush smallest first for momentum.

5. Become an Authorized User

Ask a trusted family member with excellent credit (long history, low utilization) to add you to their card. Their positive history boosts yours fast, often within a month.[1] Confirm the issuer reports to all three bureaus.

6. Add Positive Payment History with Rent and Utilities

Services like Experian Boost or rent-reporting apps (e.g., RentTrack) add on-time rent/utilities to your file—free and quick for thin files.[1][7] Great for newcomers or rebuilders. In 2026, this pairs well with other habits.[1]

7. Consider Credit-Builder Loans

Credit unions offer these: Pay into a savings account monthly (6-24 months), get reported positively. Access funds at end. Ensure reporting to all bureaus (Experian, TransUnion, Equifax).[3] Ideal post-setback.

8. Limit New Credit Applications

Hard inquiries ding scores 5-10 points each, lasting 12 months. Space apps 6+ months apart. Confirm lender's model (FICO/VantageScore) first.[6]

9. Keep Old Accounts Open

Length of history matters. Close unused cards only if high fees; otherwise, use occasionally for small buys and pay off.[2][4]

2026 Credit Score Changes and How to Adapt

BNPL like Affirm now reports—pay on time to build credit, but misses hurt.[6] Paid medical collections and debts under $500 vanish faster, easing recovery for many.[6] Monitor via alerts at AnnualCreditReport.com.[6]

Common Mistakes to Avoid

- Closing paid-off cards (hurts history/utilization).

- Maxing new limits.[2]

- Ignoring all three reports.

- Applying everywhere (inquiry overload).

Practical Tips for Long-Term Success

Integrate into your 2026 budget: Track spending with apps like Mint, build emergency fund for 3-6 months expenses. Pair with debt payoff plans. Responsible use of 1-2 cards beats many.[4]

For cosigned loans (e.g., auto), on-time payments diversify mix positively.[3]

FAQ

How long does it take to improve my credit score?

30-60 points in a month is realistic with balances paid and errors fixed; full rebuild takes 3-6 months.[1]

What's a good credit score in 2026?

670-739 (good), 740-799 (very good), 800+ (excellent) for FICO/VantageScore. Lenders vary.[3]

Does paying rent build credit?

Yes, via services like Experian Boost—adds positive history fast if reported.[1]

Can I improve credit with no credit cards?

Yes, credit-builder loans or authorized user status work well.[3]

What if I have collections?

Negotiate pay-for-delete (not guaranteed), focus on utilization elsewhere. Small medical ones fade in 2026.[6]

Is credit repair worth it?

DIY disputes are free and effective; companies charge but can't do more than you.[1]

Your Next Steps to a Better Score

Today: Pull reports from AnnualCreditReport.com, dispute errors, pay down top balances. Set auto-pay. Track monthly via free scores from banks/credit cards. In 30 days, recheck—you'll see progress. Consistent habits turn quick wins into lasting financial strength for 2026 goals like homebuying or lower insurance.

Sources & References

- 9 Real Ways to Improve Your Credit Fast — NerdWallet — nerdwallet.com[1]

- Tips To Improve Your Credit Score in 2026 — Spencer Savings Bank — spencersavings.com[2]

- 26 Tips to Improve Credit in 2026 — Experian — experian.com[3]

- How to Improve Your Credit Score in 2026 — American Bank — americanbankusa.com[4]

- Your 2026 Credit Score Playbook — Elgacu — elgacu.com[5]

- Your 2026 Credit Score Playbook — MCF CU — mcfcu.org[6]

- 7 Tips for Improving Your Credit Score — American Bankers Association — aba.com[7]

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...