What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While people frequently mix them up, understanding what is a credit report and how is it different from a credit score can empower you to take control of your finances, snag better interest rates on everything from mortgages to car loans, and even land that dream job that checks credit.

In this guide tailored for Americans, we'll break it all down with practical steps, 2026 updates, and U.S.-specific resources like free annual reports from AnnualCreditReport.com. Whether you're building credit for the first time or fixing past mistakes, you'll walk away knowing exactly how these tools work and what to do next.

What Is a Credit Report?

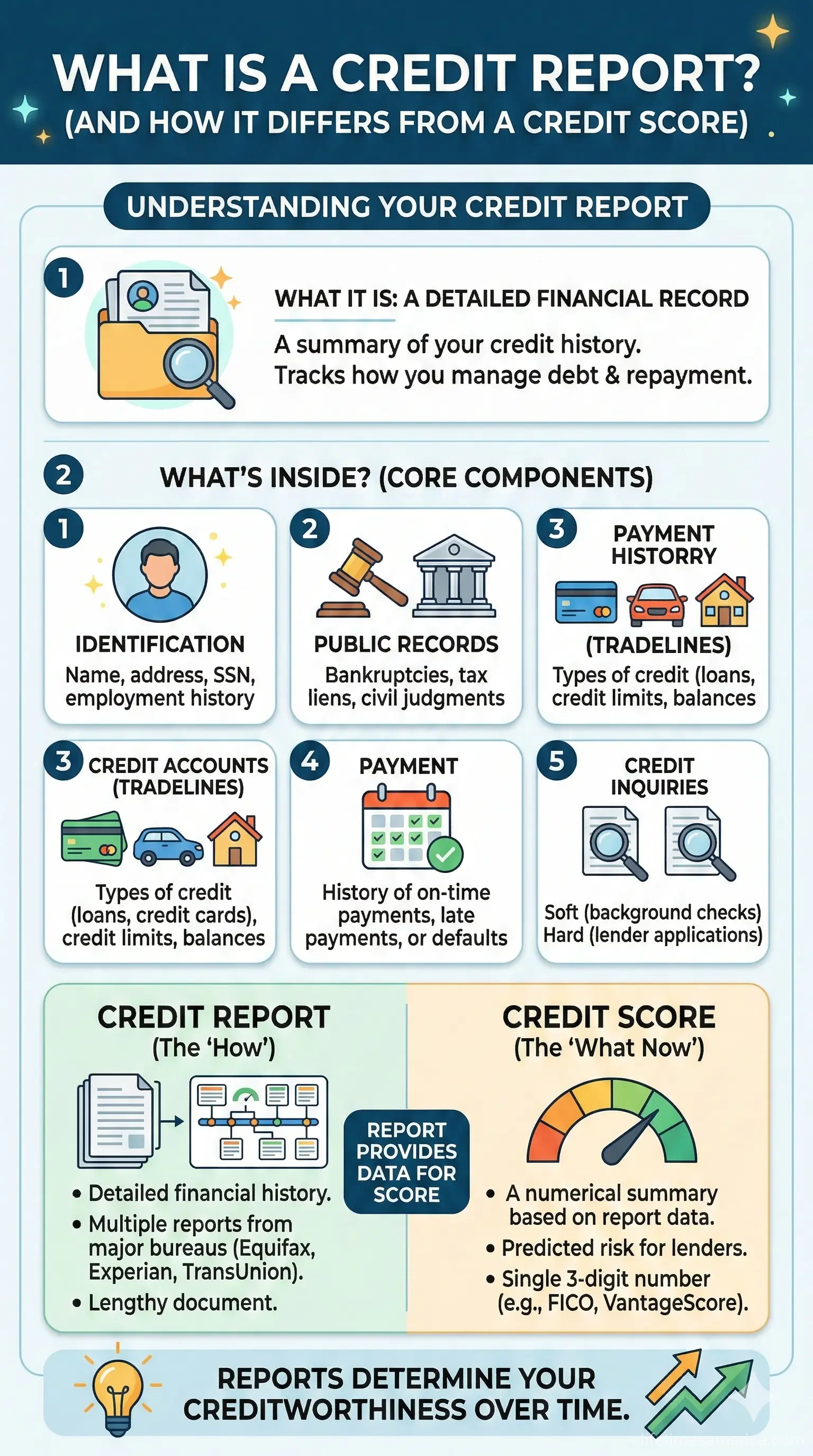

Your credit report is a detailed record of your credit history, acting like a financial resume that lenders review before approving loans, credit cards, or even rentals. Compiled by the three major nationwide consumer reporting agencies—Equifax, Experian, and TransUnion—it paints a full picture of your borrowing and repayment habits.

Think of it as a living document that updates whenever you open a new account, make a payment, or face collections. Unlike a simple number, it's pages long and includes granular details that directly feed into your credit score calculations.

What's Included in Your Credit Report?

Credit reports cover a wide range of information. Here's what you'll typically find:

- Personal information: Your name, address, Social Security number, and employment history.

- Credit accounts: Details on loans, credit cards, mortgages—including dates opened, balances, credit limits, and payment history.

- Payment history: Records of on-time payments, late payments, or defaults, which can stay for up to 7 years (or 10 for bankruptcies).

- Public records and collections: Bankruptcies, foreclosures, repossessions, charge-offs, and third-party collections.

- Inquiries: Hard inquiries from lenders when you apply for credit, and soft inquiries from your own checks.

Important note: You have three separate credit reports—one from each bureau—and they might differ slightly based on what creditors report. Negative items like late payments can linger, but under the Fair Credit Reporting Act (FCRA), you can dispute inaccuracies for free.

How to Get Your Free Credit Report

By law, you're entitled to one free credit report from each bureau every 12 months through AnnualCreditReport.com—the only official site authorized by federal law. In 2026, with ongoing economic shifts, checking weekly free reports is still available if you've experienced certain hardships, like unemployment or identity theft.

- Visit AnnualCreditReport.com.

- Provide your personal info and select which bureaus to pull from.

- Review for errors and dispute any issues online or by mail.

Pro tip: Stagger your requests—pull Equifax in January, Experian in May, TransUnion in September—to monitor year-round without cost.

What Is a Credit Score?

A credit score is a three-digit number (typically 300-850) that summarizes your credit risk based on the data in your credit report. Lenders use it as a quick gauge: higher scores signal reliability, unlocking lower rates on 401(k) loans, auto financing, or FHA mortgages.

It's not on your credit report itself—scores are calculated separately using models like FICO or VantageScore. FICO remains dominant, powering 90% of top lenders in 2026, with versions tailored for mortgages (FICO 8) or autos.

How Credit Scores Are Calculated

Scores aren't random; they're algorithms crunching report data. FICO weights factors like this:

- Payment history (35%): Your track record of paying on time.

- Amounts owed/credit utilization (30%): Debt vs. limits—aim under 30%.

- Length of credit history (15%): Average age of accounts; older is better.

- New credit (10%): Recent applications or accounts.

- Credit mix (10%): Variety of accounts like cards and installment loans.

Scores update when your report changes, like after a payment or new inquiry. In 2026, FICO models increasingly factor "trended data" (payment behavior over 24 months) for more accurate predictions.

FICO Score Ranges in 2026

| Range | Score | What It Means |

|---|---|---|

| Exceptional | 800+ | Best rates; prime borrower. |

| Very Good | 740-799 | Strong approvals, competitive rates. |

| Good | 670-739 | Qualified for most credit. |

| Fair | 580-669 | Higher rates; some approvals. |

| Poor | <580 | Challenges; focus on rebuilding. |

Higher scores in 2026 could save thousands—e.g., a 780 FICO on a $300,000 mortgage might drop your rate by 1%, cutting payments $200/month.

Key Differences: Credit Report vs. Credit Score

The core distinction? Your credit report is the raw data (detailed history), while your credit score is the snapshot summary. Like a report card vs. GPA: one lists every grade, the other averages them.

Side-by-Side Comparison

| Aspect | Credit Report | Credit Score |

|---|---|---|

| Format | Detailed pages of history | 3-digit number (300-850) |

| Source | Equifax, Experian, TransUnion | Calculated from report (FICO, VantageScore) |

| Free Access | Weekly/annual via AnnualCreditReport.com | Often paid; free via banks or Credit Karma |

| Contents | Accounts, payments, inquiries | Summarizes risk via algorithm |

| Changes | Updates with activity | Recalculates on report changes (53 FICO versions!) |

Key takeaway: Fix errors on your report first—it directly boosts scores. Lenders pull both during applications, but scores set terms like APRs on credit cards or HELOCs.

Why Both Matter for Americans in 2026

Beyond loans, credit reports/scores impact renting (many landlords check), utilities, jobs (especially finance/government), and insurance premiums. With inflation cooling but rates steady, a strong score in 2026 means better deals on everything from student loan refinances to cell plans.

Under FCRA, bureaus must provide accurate info; errors affect 1 in 5 reports. Identity theft spikes make regular checks essential—FTC reports 1.1M cases in 2025.

Practical Tips to Check, Improve, and Protect

Actionable Steps to Improve

- Pay bills on time—set autopay.

- Lower utilization: Pay down balances before statements close.

- Dispute errors via bureau sites (30-day response required).

- Build history: Use secured cards if thin file.

- Limit applications—space 6+ months apart.

Protect Against Fraud

Freeze your credit free at each bureau to block unauthorized pulls. Monitor via free tools like Credit Karma (VantageScore) or bank apps.

Take Control Today: Your Next Steps

Start by pulling your free reports at AnnualCreditReport.com and noting your scores via your bank app. Dispute errors, pay down debt, and track progress monthly. In months, you'll see improvements unlocking better financial opportunities—from lower mortgage rates to job offers. You're not just a number; arm yourself with knowledge and watch your future brighten.

Frequently Asked Questions

Sources & References

-

1

The Difference between Credit Report and Credit Score — nfmlending.com

-

2

What is the Difference Between a Credit Score and a Credit Report — www.equifax.com

-

3

Credit Score vs. Credit Report: What's the Difference? - NerdWallet — www.nerdwallet.com

- 4

-

5

Credit Report vs Credit Score - Financial Education — finances.extension.wisc.edu

- 6

- 7

-

8

Your 2026 Credit Score Playbook: The Biggest Changes — www.elgacu.com

-

9

Credit Reports and Credit Scores | FDIC.gov — www.fdic.gov

Useful Tools

Related Articles

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...

How to Check Your Credit Score for Free in the USA

Ever stared at a "declined" message on your credit card application or wondered why your dream home loan came with sky-high interest rates? Your credit score is the silent gatekeeper to your financial...