What Is Credit Utilization and How Does It Affect Your Score?

Your credit utilization ratio might be quietly dragging down your credit score without you even realizing it. Even if you pay your bills on time, this single factor can account for roughly 30% of your...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Your credit utilization ratio might be quietly dragging down your credit score without you even realizing it. Even if you pay your bills on time, this single factor can account for roughly 30% of your FICO score—making it one of the most influential elements lenders use to evaluate your creditworthiness. Understanding how credit utilization works and why it matters is essential if you want to build and maintain strong credit.

Understanding Credit Utilization

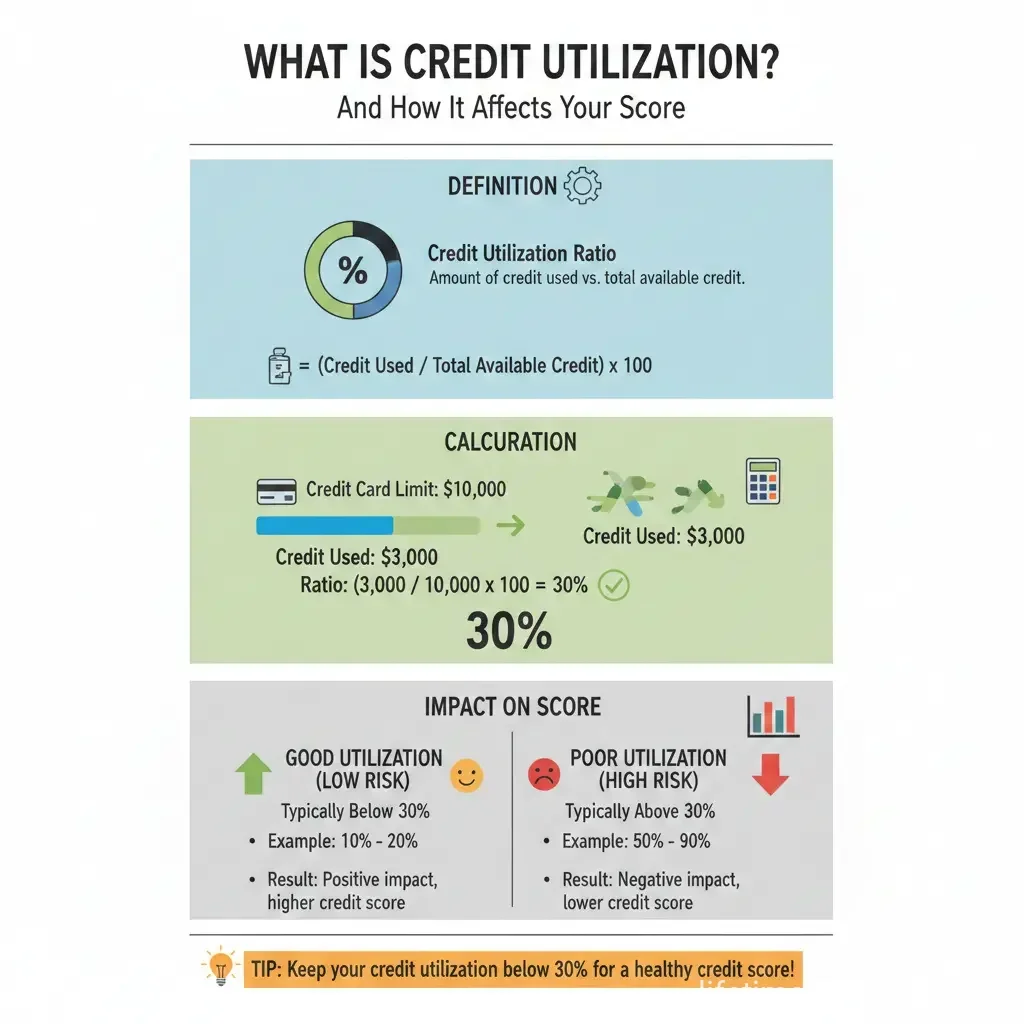

Credit utilization is the percentage of your available credit that you're currently using. Think of it as a snapshot of your credit card balances compared to your credit limits at a specific moment in time. For most Americans, this means the balances on your credit cards relative to your credit limits, though it can also include other revolving credit like home equity lines of credit (HELOCs).

Here's how to calculate your credit utilization ratio:

Your balance ÷ Your credit limit × 100 = Your credit utilization percentage

Example: If your credit card limit is $1,000 and you have a $300 balance, your credit utilization is 30%.

You actually have two types of utilization rates to consider: individual account utilization (for each card) and your overall utilization (across all your revolving credit accounts). Credit scoring models evaluate both, so managing each one matters.

Why Credit Utilization Matters to Your Score

Credit utilization is one of the biggest factors in your credit score calculation. It accounts for approximately 20% to 30% of your FICO score, depending on the scoring model. This makes it second only to payment history in terms of importance.

Here's why lenders care so much about your utilization ratio:

- Risk assessment: A high credit utilization ratio signals to lenders that you might be overextended financially and at higher risk of defaulting on payments.

- Responsible borrowing: Low utilization demonstrates that you can borrow money and pay it back responsibly without maxing out your available credit.

- Financial stability: Lenders view a high utilization ratio as a sign of financial instability, making you appear to be a higher-risk borrower.

If you have high revolving credit limits and low balances, creditors interpret this as a sign that you know how to use credit wisely. Conversely, borrowing heavily against all your credit cards and revolving lines of credit can suggest you're not as financially responsible—or that you're under financial strain.

Credit Utilization Ranges and Their Impact

Not all utilization levels affect your credit score equally. Here's what different ranges mean for your creditworthiness:

- 0-10% Utilization: Excellent for your credit score, demonstrating strong financial management.

- 11-30% Utilization: Good, but slightly higher risk than the optimal range.

- 31-50% Utilization: An okay range, but it could start to negatively affect your score.

- Above 50% Utilization: Considered high and can significantly lower your credit score.

Most credit experts recommend keeping your utilization below 30% on each card and overall. However, there's an important caveat: a utilization rate of 0% is actually worse than 1%. Credit scoring models need some usage data to evaluate your credit habits, and zero utilization doesn't tell them much about how responsibly you use credit.

For optimal results, aim for a utilization rate under 10%. Those with the highest credit scores tend to have utilization in the low single digits.

How Utilization Is Calculated and Reported

Understanding when and how your utilization is calculated can help you manage it more effectively. Credit utilization is like a snapshot—each month, your credit card company reports your balance to the credit bureaus, usually right after your statement closes. This means your credit score reflects your balance at that moment, not whether you pay it off later.

This has an important implication: if you make a big purchase just before your statement closes—even if you plan to pay it in full—it could make your utilization look high and temporarily lower your score. However, the good news is that once that balance is paid down, your utilization and credit score can bounce back quickly.

It's also important to note that only the most recently reported numbers affect most credit scores. However, newer scoring models like VantageScore 4.0 and FICO 10 T consider trended data, including your average utilization ratio and credit card balances over time. This means maintaining low utilization consistently is becoming even more important.

Strategies to Lower Your Credit Utilization

If your credit utilization is higher than you'd like, you have several practical options to improve it:

Pay Down Your Balances

The most straightforward approach is to reduce your credit card balances. Even paying more than the minimum payment can help lower your utilization quickly. Since utilization is calculated based on your most recent reported balance, paying down your balance before your statement closes can have an immediate positive impact on your score.

Request Credit Limit Increases

Another strategy is to increase your credit limits responsibly. A higher credit limit means the same balance represents a lower utilization percentage. However, be cautious—some credit card issuers perform a hard inquiry when you request a limit increase, which can temporarily lower your score. Ask your issuer if they can increase your limit without a hard pull.

Open New Credit Accounts Strategically

Opening new credit accounts increases your total available credit, which can lower your overall utilization ratio. However, this approach comes with trade-offs. New credit applications trigger hard inquiries that temporarily lower your score, and new accounts reduce your average account age, which can also hurt your score. Only pursue this strategy if you're disciplined about not increasing your spending.

Monitor Your Utilization Regularly

Keeping track of your utilization across all your accounts helps you stay on top of your credit health. Many credit card issuers provide free credit monitoring tools, and you can also check your credit reports for free annually through AnnualCreditReport.com.

Credit Utilization in 2026 and Beyond

As we move further into 2026, credit utilization remains a critical factor in your credit score. While on-time payments still matter most, lower balances relative to your limits continue to be important for maintaining strong credit. The fundamentals haven't changed—what matters is keeping your utilization low and managing your credit responsibly.

The shift toward newer scoring models that consider trended data means your long-term utilization habits are becoming increasingly important. Rather than focusing on a single moment in time, these models reward consistent, responsible credit management over months and years.

Taking Control of Your Credit Health

Your credit utilization ratio is something you can control relatively quickly, making it one of the most actionable ways to improve your credit score. By keeping your balances low relative to your credit limits, you're sending a clear signal to lenders that you're a responsible borrower.

Start by calculating your current utilization on each credit card and your overall utilization across all accounts. If you're above 30%, prioritize paying down your highest-utilization cards first. Even small reductions can have a meaningful impact on your credit score, especially since utilization changes are reflected relatively quickly in your credit reports.

Remember that building strong credit is a marathon, not a sprint. Combine low credit utilization with on-time payments, a healthy mix of credit types, and a long credit history, and you'll be well on your way to excellent creditworthiness.

Frequently Asked Questions

Sources & References

-

1

Understanding Credit Utilization: How it impacts your score — www.lfcu.org

- 2

- 3

-

4

What Is a Credit Utilization Rate? — www.experian.com

-

5

Why Your Credit Utilization Ratio Matters — www.firstmutualholding.com

-

6

What is credit utilization? (and how to improve it) — www.lendingclub.com

- 7

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...