How to Build a Credit History as a New Immigrant in the USA

Moving to the United States as a new immigrant opens exciting doors, but establishing financial stability can feel daunting—especially when you have no U.S. credit history. Without it, renting an apar...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Moving to the United States as a new immigrant opens exciting doors, but establishing financial stability can feel daunting—especially when you have no U.S. credit history. Without it, renting an apartment, securing a car loan, or even getting a job might prove challenging, as landlords, lenders, and employers often check your credit report.Building credit from scratch is possible with the right steps, and it typically takes just six months to generate your first U.S. credit score.

Whether you're on a work visa, student visa, or pursuing permanent residency, this guide walks you through practical strategies tailored for immigrants. You'll learn how to leverage your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), choose the best credit products, and adopt habits that boost your FICO Score—the key metric used by over 90% of lenders, ranging from 300 to 850. Let's dive in and get you on the path to financial independence.

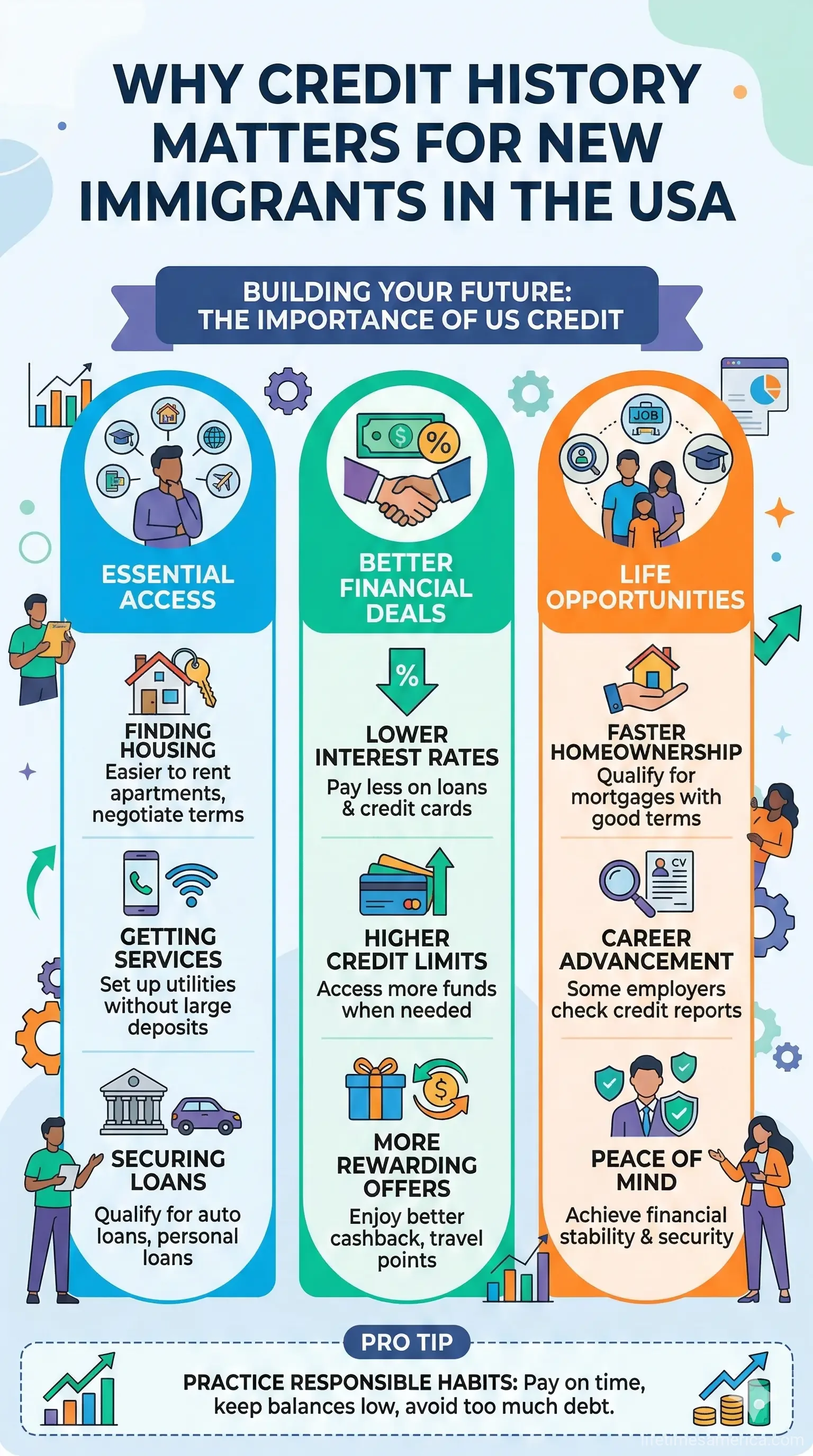

Why Credit History Matters for New Immigrants in the USA

Your U.S. credit history starts fresh upon arrival, regardless of your financial track record abroad. This leaves many newcomers "credit-invisible," meaning no score exists yet, which can hinder everyday needs like housing or utilities. Lenders evaluate creditworthiness based on factors like payment history (35%), amounts owed (30%), credit history length (15%), credit types (10%), and new credit (10%).

A strong credit score unlocks better interest rates on loans, higher credit limits, and even job opportunities. For instance, auto insurance premiums and apartment approvals often hinge on it. The good news? Consistent, responsible actions can build a solid score quickly.

Common Challenges and Realistic Timelines

- No carryover from home country: Foreign credit doesn't transfer automatically, though programs like Nova Credit or American Express Global Transfer can help for specific cards.

- Building time: FICO requires at least one account open for six months with activity reported to bureaus (Experian, Equifax, TransUnion).

- Impact on settling: Without credit, you might face higher deposits for rentals or limited cell phone plans.

Step-by-Step Guide: How to Build Credit from Zero

Start with foundational steps, then layer on credit-building tools. Prioritize official U.S. resources like the Social Security Administration (SSA) and IRS for eligibility.

Step 1: Obtain an SSN or ITIN

If authorized to work by the Department of Homeland Security (DHS) or enrolled in school, apply for a free SSN online via the SSA website. It's essential for most credit applications. Ineligible? Request an ITIN from the IRS for tax purposes—resident aliens, nonresidents, spouses, and dependents qualify. Cards from issuers like Zolve, Petal, and Neu accept ITINs, passports, or visas.

Pro tip: Visit your local SSA office with immigration documents for faster processing. An SSN verifies identity and unlocks banking.

Step 2: Open a U.S. Bank Account

Secure a checking or savings account at banks like Chase or Capital One, which often require just an SSN/ITIN and ID. This builds a financial footprint and may report positive activity to credit bureaus via services like Experian Boost. Direct deposits from employment further strengthen your profile.

Step 3: Become an Authorized User on a Credit Card

Ask a trusted family member or friend with good credit to add you as an authorized user on their card. Their positive history—on-time payments and low utilization—can appear on your report, jumpstarting your score. Ensure the issuer reports to all three bureaus.

Step 4: Apply for Beginner-Friendly Credit Products

Once basics are in place, target these options designed for immigrants:

| Product | Best For | Key Features | Examples |

|---|---|---|---|

| Secured Credit Cards | No credit history | Refundable deposit sets limit; builds history fast | Discover it Secured, Capital One Secured |

| Credit-Builder Loans | Steady income | Loan held in savings; payments reported | Self or local credit unions |

| Non-Traditional Cards | ITIN users | Uses income/banking history | Petal, Zolve, Neu |

| Global Transfer Cards | Existing Amex abroad | Imports foreign history | American Express Global Transfer |

Use cards responsibly: Pay on time (builds 35% of score) and keep utilization under 30% (e.g., $300 balance on $1,000 limit). Avoid multiple applications to minimize hard inquiries.

Step 5: Report Rent and Utilities (Alternative Data)

Services like Experian Boost or rental reporting apps (e.g., RentTrack) add on-time rent and bill payments to your file. This can boost scores by 10-40 points instantly for eligible users. Check eligibility via annualcreditreport.com—free weekly reports from all bureaus.

Step 6: Monitor and Maintain Progress

Track via free tools: Credit Karma, annualcreditreport.com, or bureau apps. Dispute errors promptly. Aim for six months of history before major applications like mortgages, where thin credit might still qualify with larger down payments.

Best Practices for Long-Term Credit Success

- Pay everything on time—set autopay.

- Limit new applications to 1-2 per year.

- Diversify: Mix cards and loans after one year.

- Keep old accounts open to lengthen history (15% of score).

- Avoid maxing out—low utilization signals responsibility.

For homebuyers, note that some lenders accept foreign credit checks or manual underwriting for mortgages. Public charge rules don't penalize credit-building; focus on self-sufficiency.

Next Steps to Secure Your Financial Future

Today, gather your documents and apply for an SSN/ITIN via ssa.gov or irs.gov. Open a bank account, then a secured card—track monthly via free reports. Within a year, you'll qualify for better rates on apartments, cars, and loans. Stay consistent; your U.S. dream includes financial freedom. For personalized advice, consult non-profits like those at usa.gov/immigration or local credit unions.

Frequently Asked Questions

Sources & References

-

1

Credit Building for Immigrants: A Step-by-Step Guide - Experian — www.experian.com

- 2

-

3

Building Credit as a New Immigrant in the U.S. - Chase Bank — www.chase.com

-

4

New U.S. Immigrants with No Credit Can Establish Good Credit - LawHelpCA — www.lawhelpca.org

-

5

How Can Immigrants Build Credit? - Capital One — www.capitalone.com

- 6

-

7

Credit Building Essentials for Immigrants - Majority — majority.com