What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you'll make in the home-buying process. Understanding what a down payment is, how it works, and how much you actually need can save you thousands of dollars and help you make a smarter financial decision.

What Is a Down Payment?

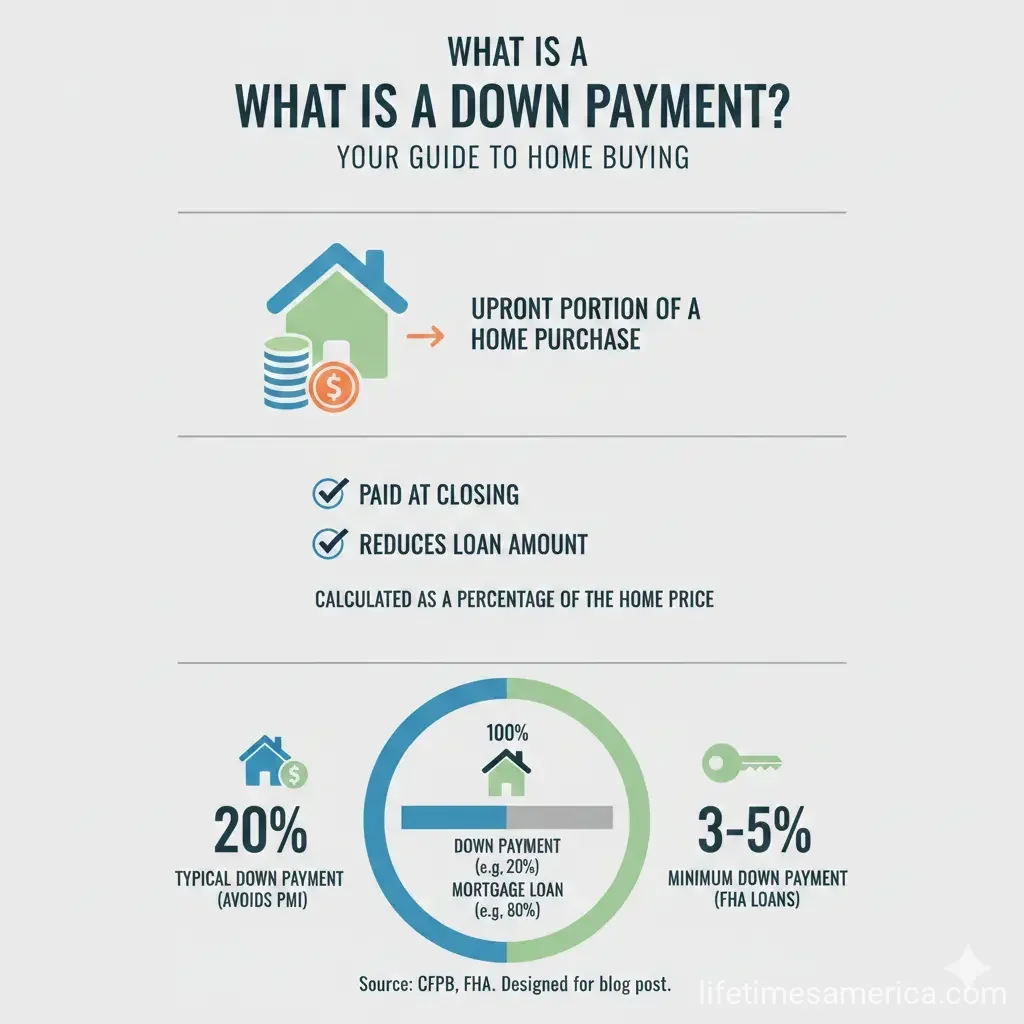

A down payment is an upfront lump sum of cash you pay toward the purchase price of a home. It's separate from closing costs and represents your initial investment in the property. Instead of financing the entire home purchase with a mortgage, you pay a portion of the price upfront, and the lender finances the rest.

Here's how it works in practice: if you're buying a $400,000 home and putting down 10%, you'll pay $40,000 upfront. The lender then provides a mortgage for the remaining $360,000. Your down payment is typically expressed as a percentage of the total purchase price, and it directly affects how much you'll need to borrow and what your monthly payments will look like.

The down payment you make at closing gets transferred through an escrow account managed by a real estate attorney or settlement officer, who then disburses the funds to the seller. If you've already made an earnest money deposit (a good faith deposit when your offer was accepted), that amount gets applied toward your down payment.

How Much Down Payment Do You Actually Need?

Here's the good news: you don't need to put down 20%. While that's been the traditional benchmark, the average down payment for first-time homebuyers is between 6% and 13%, and you can qualify for mortgages with as little as 3% down—or even zero down, depending on your loan type.

The minimum down payment requirements vary by mortgage type:

- Conventional Loans: 3% minimum

- FHA Loans: 3.5% minimum (with a credit score of at least 580)

- VA Loans: No down payment required

- USDA Loans: No down payment required

If you have an FHA loan and your credit score is below 580, you'll need to compensate with at least a 10% down payment. For conventional loans, some lenders may require a higher down payment if your income or credit score are lower than ideal.

The Real Cost: 5% Down vs. 20% Down

Let's look at a real-world example with a $300,000 home to understand how your down payment affects your monthly costs:

| Factor | 5% Down Payment | 20% Down Payment |

|---|---|---|

| Down Payment Amount | $15,000 | $60,000 |

| Loan Amount | $285,000 | $240,000 |

| Monthly Mortgage Payment (Principal + Interest) | $1,896 | $1,597 |

| PMI (Private Mortgage Insurance) | $274 | $0 |

| Total Monthly Payment | $2,170 | $1,597 |

As you can see, putting down just 5% instead of 20% increases your monthly payment by $573 (before property taxes and homeowners insurance). However, if you don't have $60,000 saved, a 5% down payment allows you to become a homeowner sooner rather than waiting years to save.

Why Down Payments Matter

Protection for Lenders (and You)

Lenders require a down payment primarily as a hedge against risk. If they have to foreclose and sell the property, they're not on the hook for the entire purchase price. Your down payment represents your skin in the game—if you stop making mortgage payments, you're walking away from thousands of dollars you've already invested.

Your Loan-to-Value Ratio (LTV)

Your down payment determines your loan-to-value ratio, which is the amount you're borrowing compared to the appraised value of your home. Lenders use this to assess their risk. Here's how it works:

- 20% down payment = 80% LTV

- 10% down payment = 90% LTV

- 40% down payment = 60% LTV

The lower your LTV, the lower the perceived risk to the lender, which often results in better interest rates for you.

Benefits of a Larger Down Payment

While you don't need to put down 20%, there are real financial advantages to saving for a larger down payment if you can:

- Lower Interest Rates: A larger down payment reduces lender risk, often resulting in better interest rates

- Lower Monthly Payments: Financing a smaller portion of the home's price leads to lower monthly mortgage payments

- No Mortgage Insurance: Putting 20% or more down eliminates the need for private mortgage insurance (PMI), which can save you hundreds of dollars annually

- More Equity Immediately: A bigger down payment means more equity right away, offering financial security and flexibility for refinancing or selling later

- Better Debt-to-Income Ratio: A larger down payment reduces your monthly mortgage payment, improving your debt-to-income ratio and making it easier to qualify for future loans

- Competitive Advantage: A large down payment can make your offer more attractive to sellers, especially in a competitive housing market

- Afford More Home: With a larger down payment, you can afford a more expensive home while keeping your monthly payments manageable

The Drawback: Private Mortgage Insurance (PMI)

Here's an important detail: any down payment under 20% normally requires mortgage insurance. This is private mortgage insurance (PMI), and it protects the lender if you default on your loan. PMI gets added to your monthly mortgage payment and can be expensive.

In the example above with a 5% down payment, the PMI was $274 per month. Over a 30-year mortgage, that's more than $98,000 in insurance costs. However, PMI isn't permanent—once you've paid down enough of your mortgage principal, you can request to have it removed.

How Down Payments Benefit You

Beyond helping lenders manage risk, down payments benefit you in several important ways:

- Reduces Debt: A down payment reduces the amount of debt you're borrowing with a mortgage, helping prevent you from overextending yourself financially

- Saves on Interest: Less borrowed means less interest paid over the life of the loan

- Builds Equity: Your down payment gives you immediate equity in the home—a tappable asset you can leverage later

- Improves Financial Stability: A smaller mortgage payment makes it easier to manage your budget and save for other financial goals

What if You Don't Have a Large Down Payment?

The reality is that most Americans don't have 20% saved for a down payment, and that's okay. You have options:

- FHA Loans: Designed for borrowers with lower credit scores and smaller down payments, FHA loans allow you to put down as little as 3.5%

- VA Loans: If you're a veteran or active military, VA loans require no down payment

- USDA Loans: If you're buying in a rural area and meet income requirements, USDA loans require no down payment

- Conventional Loans with 3% Down: Many conventional lenders now offer mortgages with just 3% down if you have stable income and a solid credit history

- Gift Funds: Many loan programs allow you to use gift funds from family members toward your down payment

- Down Payment Assistance Programs: Some states and local governments offer down payment assistance for first-time homebuyers

The Bottom Line

Your down payment is one of the most important decisions in the home-buying process, but it doesn't have to be 20%. Most Americans put down between 6% and 13%, and you can qualify for mortgages with as little as 3% down or even zero down with certain loan programs.

The key is understanding the trade-offs: a smaller down payment gets you into a home sooner, but you'll pay more in monthly mortgage payments and PMI. A larger down payment reduces your monthly costs and eliminates PMI, but requires more upfront savings.

Start by calculating what you can afford to save, research loan programs that match your financial situation (FHA, VA, USDA, or conventional), and use a mortgage calculator to see how different down payment amounts affect your monthly payment. Consider talking to a mortgage lender who can review your specific situation and help you find the right balance between your down payment and monthly affordability.

Frequently Asked Questions

Sources & References

-

1

What is a down payment and how does it work? — Rocket Mortgage — www.rocketmortgage.com

-

2

What is a down payment? How do they work? — Bankrate — www.bankrate.com

-

3

What Is a Down Payment on a Home Loan? — Assurance Mortgage — assurancemortgage.com

-

4

How Much Should You Put Down on a House? — The Mortgage Reports — themortgagereports.com

-

5

How Much Down Payment Do You Need To Buy A Home in 2026? — AmeriSave — www.amerisave.com

-

6

The Math Behind Putting Down Less Than 20% — Freddie Mac — myhome.freddiemac.com

-

7

Down payment pros and cons — Citizens Bank — www.citizensbank.com

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is PMI (Private Mortgage Insurance) and How Do You Avoid It?

Buying your first home is exciting, but those extra mortgage costs can quickly dampen the thrill. If you've heard whispers about Private Mortgage Insurance (PMI) sneaking into your monthly payments, y...