What Is a Pension vs a 401(k)? Key Differences Explained

When it comes to planning for retirement, understanding your options is crucial. Two of the most common retirement savings vehicles in the United States are pensions and 401(k) plans—but they work in...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

When it comes to planning for retirement, understanding your options is crucial. Two of the most common retirement savings vehicles in the United States are pensions and 401(k) plans—but they work in fundamentally different ways. If you're wondering which one you have, or how they compare, you're not alone. The choice between these two can significantly impact your financial security in retirement, and the differences go far deeper than just how much money you contribute.

Understanding the Basics: Pension vs. 401(k)

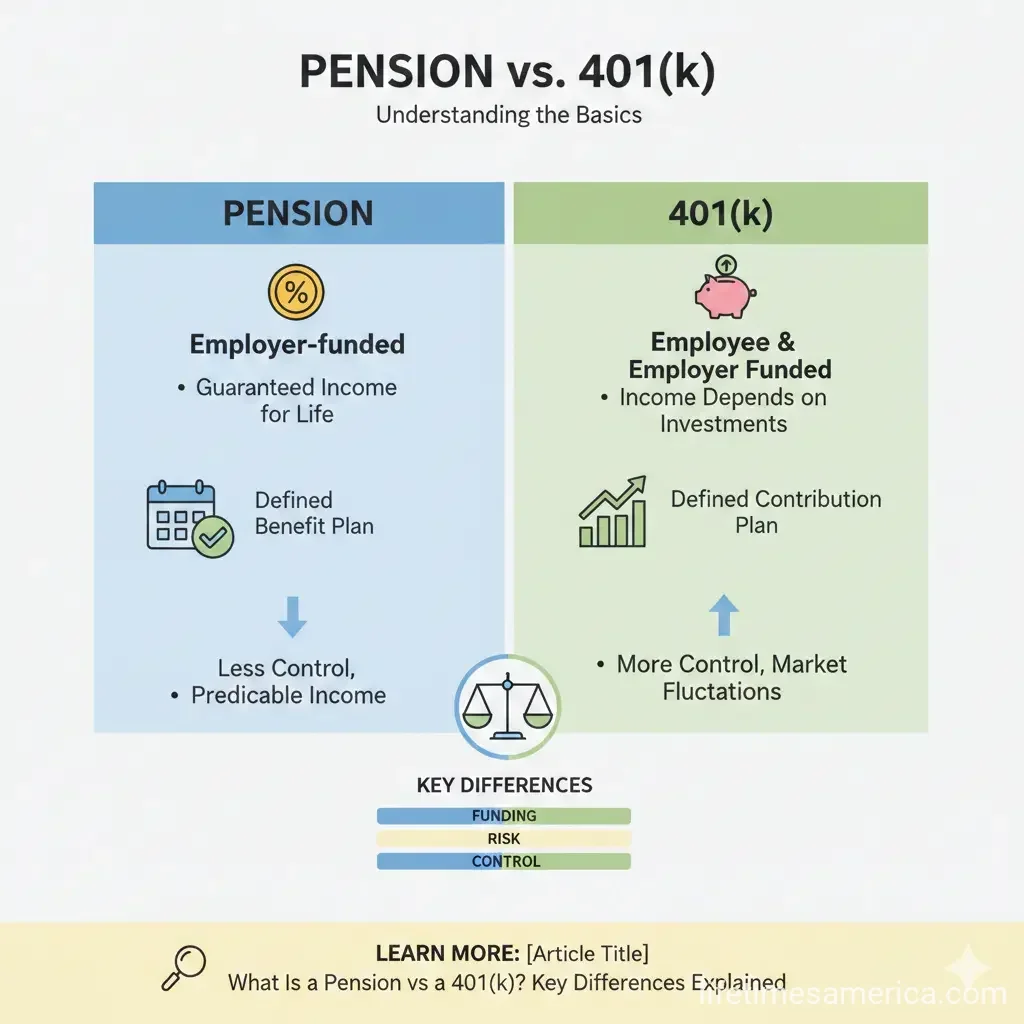

At their core, pensions and 401(k)s represent two distinct philosophies about retirement savings. A pension is a defined-benefit plan, meaning your employer promises you a specific monthly payment for life based on a formula that typically considers your salary and years of service. A 401(k) is a defined-contribution plan, where you and your employer contribute money to an individual account, and your retirement income depends on how much you've saved and how well your investments perform.

Think of it this way: with a pension, your employer bears the investment risk and guarantees your income. With a 401(k), you bear the risk and control the investment decisions.

How Funding Works: Who Pays Into These Plans?

Pension Plans

Pension plans are employer-funded. Your employer contributes money to a shared fund that covers all employees in the plan. As an employee, you typically don't contribute directly to a pension—your employer handles the entire funding responsibility. This means the company is betting that its contributions, combined with investment returns, will be enough to pay all promised benefits to all retirees.

Because the employer shoulders this burden, pensions have become less common over the past few decades. Many companies found the long-term financial commitment too risky or expensive, which is why they've shifted toward offering 401(k)s instead.

401(k) Plans

With a 401(k), the funding model flips. You contribute pre-tax dollars directly from your paychecks, and your employer may match a portion of your contributions as an incentive to save. For 2026, you can contribute up to $24,500 to your 401(k) if you're under 50 years old. If you're 50 or older, you can add an additional $8,000 in catch-up contributions, bringing your total to $32,500. Those between ages 60 and 63 can take advantage of "super-catch-up" contributions of an additional $11,250, for a total of $35,750.

The responsibility for building your retirement nest egg falls on you. Your employer's match is a bonus, but it's your job to decide how much to save and where to invest that money.

Investment Control and Risk

Who Makes Investment Decisions?

With a pension, your employer or plan administrator makes all investment decisions. You have no control over how the fund's money is invested. This might sound limiting, but it also means you don't have to worry about picking stocks or managing a portfolio. The tradeoff is that you also can't benefit from aggressive growth strategies if you're comfortable with higher risk.

A 401(k) gives you significant control over your investments. You can choose from various asset classes—stocks, bonds, mutual funds, target-date funds—based on your risk tolerance and financial goals. This flexibility is powerful, but it also means you're responsible for making informed decisions. Poor investment choices or market downturns could reduce your retirement savings.

Predictability vs. Uncertainty

Pension payments are predictable and stable. You know exactly how much you'll receive each month because it's calculated using a benefit formula. This makes budgeting in retirement much easier.

401(k) payouts depend on account balance and investment performance. Your retirement income can fluctuate based on market conditions and your personal investment decisions. This adds uncertainty—you might have more or less than you expected depending on how your investments perform.

How You Receive Your Money in Retirement

Pension Payouts

Pensions typically provide guaranteed monthly payments for life. Once you retire, you receive a designated amount every month, which provides a stable income stream you can count on. Some pensions may offer alternative payout options, but the standard is a monthly check for as long as you live.

This structure effectively covers longevity risk—the concern about outliving your savings—since payments continue regardless of how long you live.

401(k) Withdrawals

With a 401(k), you have more flexibility in how you access your money. You can take withdrawals in any amount at any time once you're retired. However, if you withdraw before age 59½, you'll typically face a 10% early withdrawal penalty plus income taxes on the amount withdrawn. After age 59½, you can withdraw without penalty, though you'll still owe income taxes on traditional 401(k) withdrawals.

You might take a lump sum, periodic withdrawals, or set up systematic distributions. Some people use a strategy called a "4% rule," withdrawing about 4% of their balance annually to make their savings last through retirement. The challenge is that if you withdraw too much too quickly, you could run out of money.

Advantages and Disadvantages

Why Choose a Pension?

Advantages:

- Guaranteed income for life—You know exactly what you'll receive each month, providing security and peace of mind

- No investment risk on your shoulders—Your employer handles all investment decisions and bears the market risk

- Survivor benefits—Many pensions offer benefits that support your loved ones after you pass away

- Predictable budgeting—You can plan your retirement finances with certainty

Disadvantages:

- Lack of portability—If you change jobs, you could lose your pension benefits or face penalties for early withdrawal

- Less control—You have no say in how your money is invested

- Increasingly rare—Fewer employers offer pensions today, making them harder to find

Why Choose a 401(k)?

Advantages:

- Investment control—You choose how your money is invested based on your goals and risk tolerance

- Flexibility in withdrawals—You can take money out as needed in retirement

- Loan options—You can borrow against your savings if you face financial hardship

- Portability—You can take your 401(k) with you if you change jobs by rolling it over to a new employer's plan or an IRA

- Tax-deferred growth—Your money grows without being taxed until you withdraw it

- Employer match—Your employer's contributions are free money that helps your savings grow faster

Disadvantages:

- Investment risk on you—Poor investment choices or market downturns can reduce your savings

- Uncertain retirement income—You don't know exactly how much you'll have

- Account could run out—If you withdraw too much or live longer than expected, you could deplete your savings

- Requires financial knowledge—You need to understand investments to make good decisions

Important 2026 Changes for 401(k) Savers

If you're a high-income earner, pay attention to a significant change taking effect in 2026. If your FICA income was $150,000 or more in the prior year and you're over 50, any catch-up contributions you make must go into your plan's Roth option rather than traditional tax-deferred contributions.

This means higher-income older workers who want to make traditional contributions can still contribute the base limit of $24,500 to the traditional option, but catch-up contributions must be Roth. This change, part of the Secure 2.0 retirement legislation, affects how you plan your tax strategy in retirement.

Survivor Benefits: What Happens to Your Money?

Both pensions and 401(k)s offer survivor benefits, but they work differently. Federal law requires both types of plans to pay survivor benefits to a married participant's spouse unless the spouse waives that right.

With a 401(k), survivor benefits are whatever remains in your account. If you die with $200,000 in your 401(k), your beneficiary receives that $200,000.

With a defined-benefit pension, surviving spouses have the option to receive monthly benefits for life, similar to what the retiree was receiving. This provides ongoing income security for your family.

Taking the Next Steps

Whether you have a pension, a 401(k), or ideally both, understanding how each works is essential for retirement planning. If you have a pension, appreciate the guaranteed income it provides and plan your other retirement savings around it. If you rely on a 401(k), make sure you're contributing enough to capture any employer match, diversifying your investments appropriately for your age and risk tolerance, and regularly reviewing your portfolio.

Consider meeting with a financial advisor to create a comprehensive retirement plan that accounts for Social Security, pensions, 401(k)s, IRAs, and any other income sources. The more you understand your retirement income sources today, the more confident you'll be about your financial security tomorrow.

Frequently Asked Questions

Sources & References

-

1

Pension Plan vs 401(k) | PensionBee (US) — www.pensionbee.com

-

2

Pension vs. 401(k): Which One Is for You? - Farther — www.farther.com

-

3

How are pensions and 401(k)s different? - PBGC — www.pbgc.gov

-

4

3 Big Changes for Retirement Planning in 2026 - Morningstar — www.morningstar.com

-

5

9 Ways Your Retirement Planning Will Change in 2026 - AARP — www.aarp.org

-

6

Big Changes Ahead for 401(k) Plans in 2026 - Savant Wealth — savantwealth.com

Useful Tools

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...