What Is an ETF and How Is It Different from a Mutual Fund?

Imagine building a diversified investment portfolio without picking individual stocks or bonds—sounds appealing, right? That's the power of both ETFs and mutual funds, two popular choices for American...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine building a diversified investment portfolio without picking individual stocks or bonds—sounds appealing, right? That's the power of both ETFs and mutual funds, two popular choices for American investors looking to grow their savings efficiently. But while they share similarities, key differences in trading, costs, and taxes can make one a better fit for your 401(k), IRA, or brokerage account.

In this guide, we'll break down what an ETF is and how it's different from a mutual fund, using real-world examples tailored to U.S. investors. Whether you're just starting with a Roth IRA or fine-tuning your retirement strategy, understanding these options helps you make smarter choices in today's market.

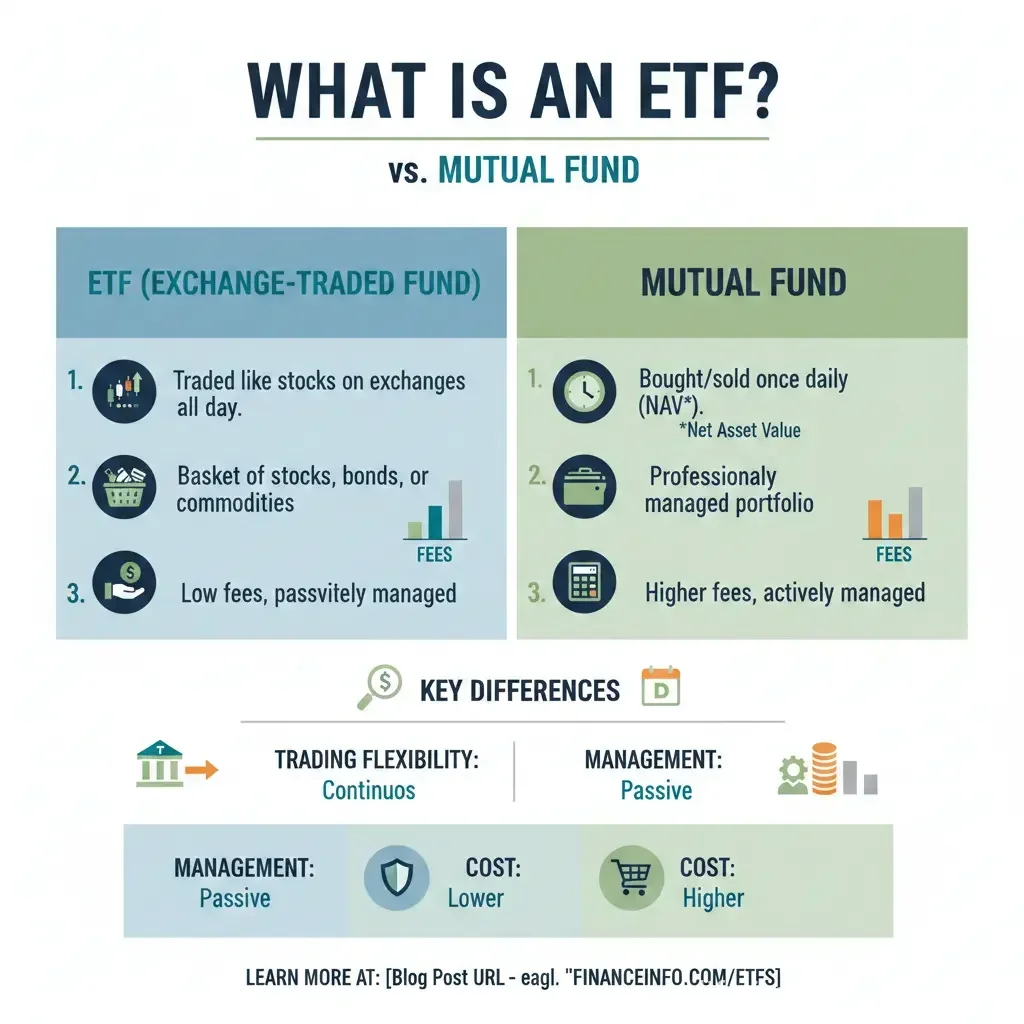

What Is an ETF?

An Exchange-Traded Fund (ETF) is a type of investment fund that holds a collection—or "basket"—of assets like stocks, bonds, or commodities, and trades on stock exchanges just like individual shares. Think of popular ones like the SPDR S&P 500 ETF (SPY), which mirrors the S&P 500 index, giving you exposure to 500 of America's largest companies in one trade.

ETFs burst onto the scene in the 1990s and have exploded in popularity. By 2026, they manage trillions in assets, appealing to everyone from day traders to long-term retirement savers because of their flexibility and low costs.

How ETFs Work

ETFs are created and redeemed through an "in-kind" process involving authorized participants (large institutions). This means when shares are exchanged, the ETF swaps baskets of underlying securities rather than cash, minimizing taxable events. You buy and sell ETF shares throughout the trading day at market prices on exchanges like the NYSE or Nasdaq, similar to stocks.

- Daily pricing: Prices fluctuate in real-time based on supply and demand.

- Transparency: ETFs disclose full holdings daily, unlike mutual funds' monthly reports.

- Styles: Mostly passive (tracking indexes like the Dow Jones), but active ETFs exist too.

For U.S. investors, ETFs fit seamlessly into brokerage accounts at firms like Vanguard, Fidelity, or Charles Schwab, and many 401(k) plans now offer them via self-directed brokerage windows.

What Is a Mutual Fund?

A mutual fund pools money from many investors to buy a diversified mix of securities, managed by professionals. Like ETFs, they offer instant diversification—say, into tech stocks or international bonds—without you managing it yourself.

Mutual funds have been a staple since the 1920s, powering many Americans' retirements through 401(k)s and IRAs. Iconic examples include the Vanguard 500 Index Fund, which tracks the S&P 500 much like its ETF counterpart.

How Mutual Funds Work

Mutual funds price once daily at Net Asset Value (NAV)—the total value of assets minus liabilities, divided by shares outstanding—after markets close. Orders placed anytime that day execute at the end-of-day NAV.

- Management: Often actively managed by pros aiming to beat benchmarks, though passive index funds are common.

- Minimums: Typically require $500–$5,000 to start, though some brokers now allow fractional shares.

- Accessibility: Bought directly from fund companies, brokers, or in employer 401(k) plans.

ETFs vs. Mutual Funds: Key Differences

Both provide diversification across asset classes, from U.S. Treasuries to emerging markets, and can be passive or active. But their structures lead to distinct advantages. Here's a side-by-side comparison:

| Feature | ETFs | Mutual Funds |

|---|---|---|

| Trading | Throughout the day at market price, like stocks. Limit orders, short selling possible. | Once daily at NAV after market close. |

| Minimum Investment | Price of one share (e.g., $50–$500). | Often $500–$5,000; fractional shares at some brokers. |

| Expense Ratios (2026 Averages) | 0.14% for passive; higher for active. | 0.40% average; lower for index funds. |

| Tax Efficiency | Higher: In-kind redemptions avoid capital gains distributions. | Lower: Redemptions can trigger gains for all shareholders. |

| Transparency | Daily holdings disclosure. | Monthly or quarterly. |

| Best For | Active traders, tax-conscious investors in taxable accounts. | Buy-and-hold in 401(k)s/IRAs, automatic investing. |

Trading Flexibility

ETFs shine for intraday trading. Need to react to Fed announcements or earnings? Sell SPY mid-day without waiting. Mutual funds lock you into end-of-day pricing, better for set-it-and-forget-it strategies like dollar-cost averaging in a 401(k).

Costs and Fees

ETFs edge out with lower expense ratios—passive ones often under 0.10%—saving you money over decades. For example, a $10,000 investment at 0.14% vs. 0.40% costs $14 vs. $40 yearly. Watch for brokerage commissions (many are $0 now) and mutual fund loads (sales fees up to 5.75%, though no-load options exist).

Tax Implications for U.S. Investors

In taxable brokerage accounts, ETFs' structure reduces capital gains distributions. Mutual funds often pass gains to shareholders when others redeem, even if you hold steady—taxed at up to 20% long-term rates per IRS rules. Both defer taxes in IRAs or 401(k)s, but ETFs win outside tax-advantaged accounts. Always consult IRS Publication 550 for details.

Management and Performance

ETFs are mostly passive, rarely beating markets long-term but matching low-cost indexes like the S&P 500. Active mutual funds aim higher but underperform indexes 80–90% over 15 years, per studies. Active ETFs are growing in 2026, blending both worlds.

Pros and Cons for American Investors

Advantages of ETFs

- Low entry barrier: Start with $100.

- Intraday liquidity and advanced orders.

- Tax perks in taxable accounts.

- High transparency for risk monitoring.

Disadvantages of ETFs

- Potential premium/discount to NAV in volatile markets.

- Temptation to trade excessively, racking up costs.

- Limited in some 401(k)s without brokerage windows.

Advantages of Mutual Funds

- Automatic investments ideal for 401(k) contributions.

- Professional management for complex strategies.

- Fractional shares for precise dollar amounts.

Disadvantages of Mutual Funds

- Higher taxes and fees.

- No intraday trading.

- Larger minimums.

Which Should You Choose? Practical Tips

Match to your style: ETFs for flexibility and taxes; mutual funds for hands-off retirement plans. Diversify with both—e.g., SPY ETF for U.S. stocks, Vanguard Total Bond Market mutual fund for fixed income.

Actionable Steps:

- Check your 401(k) or IRA options via plan administrator.

- Use brokerage screeners at Fidelity or Schwab for low-fee ETFs under 0.20%.

- Model taxes with tools on Vanguard.com.

- Start small: Buy one SPY share to test.

- Consult a fiduciary advisor via NAPFA.org for personalized advice.

Ready to Invest Smarter?

ETFs offer trading flexibility, lower costs, and tax efficiency, while mutual funds excel in retirement plans with automatic features. Assess your goals—active trading or long-term saving?—and blend them for a robust portfolio. Open a brokerage account today, fund your IRA before the 2026 tax deadline (April 15, 2027), and track progress quarterly. Your future self will thank you.

Frequently Asked Questions

Sources & References

-

1

ETFs vs. Mutual Funds – What's the Difference? — schwab.com — www.schwab.com

- 2

-

3

ETF vs. Mutual Fund: Compare Costs and Management — nerdwallet.com — www.nerdwallet.com

-

4

Mutual funds vs. ETFs: Which is best for your investment strategy? — troweprice.com — www.troweprice.com

-

5

ETF vs mutual fund: 9 strategic considerations — vettafi.com — www.vettafi.com

- 6

-

7

ETFs vs. Mutual Funds: Which To Choose | Vanguard — investor.vanguard.com — investor.vanguard.com

-

8

Mutual funds vs. ETFs: Which is right for you? — fidelity.com — www.fidelity.com

-

9

6 ETF Investing Predictions for 2026 | Morningstar — morningstar.com — www.morningstar.com

Useful Tools

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...