How to Set Realistic Financial Goals at Every Life Stage

Imagine kicking off 2026 with a clear path to financial freedom, no matter if you're just starting your career or planning your golden years. Setting realistic financial goals tailored to your life st...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine kicking off 2026 with a clear path to financial freedom, no matter if you're just starting your career or planning your golden years. Setting realistic financial goals tailored to your life stage empowers you to build wealth, reduce stress, and enjoy life's milestones—from buying your first home to retiring comfortably. In the United States, where 84% of Americans set financial resolutions each year, understanding generational priorities makes all the difference.

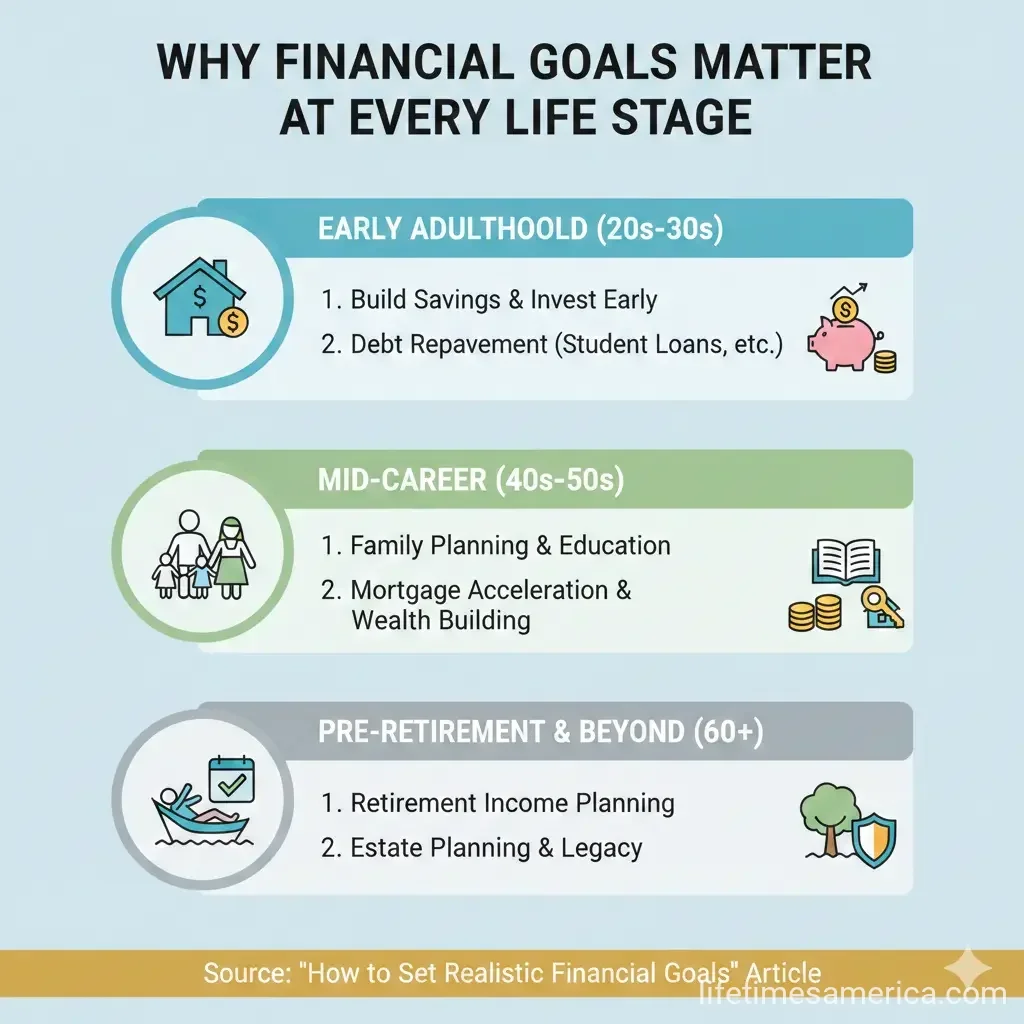

Why Financial Goals Matter at Every Life Stage

Financial goals act as your roadmap, helping you navigate economic pressures like high credit card rates and rising living costs. A 2026 survey by the American Institute of CPAs (AICPA) reveals that nearly all Americans have goals for the year, but they vary widely by generation: Gen Z focuses on big purchases like cars and homes, while older groups prioritize debt and retirement. Experts recommend starting with one key priority to avoid overwhelm, such as building an emergency fund or paying down debt, which tops lists for 31% of Americans.

According to the Consumer Financial Protection Bureau (CFPB), a solid plan includes budgeting, goal-setting, and knowledge-building to avoid overspending or missing savings opportunities. With 67% of Americans living paycheck to paycheck—including high earners—tailoring goals to your stage ensures progress.

Step-by-Step Guide to Setting Realistic Financial Goals

Before diving into life stages, follow this proven 6-step process adapted for 2026 from official resources like the Department of Financial Protection and Innovation (DFPI) and USA.gov.

Step 1: Evaluate Your Current Situation

Track your income from wages, benefits, or side gigs, and list expenses like rent, groceries, and debt payments. Use free tools from the CFPB or apps to catalog assets and debts. This baseline reveals surpluses for savings.

Step 2: Define SMART Goals

Make goals Specific, Measurable, Achievable, Relevant, and Time-bound. Short-term: Build a $1,000 emergency fund in three months. Long-term: Save $50,000 for a home down payment by 2030. USA.gov emphasizes measurability to stay motivated.

Step 3: Create a Budget

Try the 50/30/20 rule: 50% needs (housing, utilities), 30% wants (dining out), 20% savings/debt. Subtract expenses from income and adjust. Fewer than half of U.S. adults budget, yet it's key for the 26% overspending.

Step 4: Build an Emergency Fund

Aim for 3-6 months of expenses in a high-yield savings account. In 2026, 29% prioritize this, especially Gen Z with limited cushions.

Step 5: Automate and Track Progress

Set up auto-transfers to 401(k)s, IRAs, or savings. Review monthly and adjust for life changes like job shifts.

Step 6: Seek Resources and Review Annually

Use IRS.gov for retirement calculators, SSA.gov for Social Security estimates, or CFPB tools. Revisit goals yearly.

Financial Goals by Life Stage in 2026

Generational surveys show distinct priorities. Here's how to set realistic targets with U.S.-specific advice.

Gen Z (Ages 18-28): Building Foundations

Focus on milestones like cars (top goal) or homes (36%). Many lack emergency savings or debt (27%), so start small.

- Save $500/month for a car down payment using a Roth IRA for flexibility.

- Build a $1,000 starter emergency fund via apps like Acorns.

- Avoid high-interest debt; use student loan forgiveness if eligible via Federal Student Aid.

Actionable tip: Automate 10% of paycheck to savings for vacations or stability.

Millennials (Ages 29-44): Balancing Act

Prioritize debt payoff (35%), vacations (36%), and stability amid family costs. High earners often live paycheck to paycheck.

- Pay down credit card debt with avalanche method (highest interest first).

- Max 401(k) matches—2026 limit is $23,500 plus catch-up if over 50 (IRS.gov).

- Save for kids' 529 plans for tax-free education growth.

Use budgeting tools to free up cash for home down payments or weddings.

Gen X (Ages 45-60): Catching Up on Retirement

Debt reduction (37%) and investing (31%) lead, as you juggle college tuition and aging parents.

- Increase 401(k)/Roth IRA contributions—2026 IRA limit $7,000 + $1,000 catch-up.

- Review Medicare eligibility at 65 via Medicare.gov.

- Build to 10x salary in retirement savings per Fidelity guidelines.

Experts urge annual boosts to employer plans.

Baby Boomers (Ages 61+): Securing Retirement

Debt payoff (33%) and vacations (27%) mix with legacy planning. Boomers lead in emergency savings over debt.

- Reduce risk in portfolios; shift to bonds via Vanguard tools.

- Optimize Social Security claims—delay to 70 for max benefits (SSA.gov).

- Update estate plans with wills or trusts to minimize estate taxes.

Review Medicaid for long-term care if needed.

Common Pitfalls and How to Avoid Them

Don't tackle everything at once—focus on one goal, like 70% of resolution-makers saving more. Track credit via AnnualCreditReport.com (free weekly). With elevated rates, prioritize high-interest debt over low-yield savings.

"Rather than trying to tackle everything at once, I recommend focusing on the single most important financial priority in 2026 and making consistent progress there first."

Take Control of Your Financial Future Today

Setting realistic goals at every life stage turns 2026 aspirations into achievements. Start by evaluating your situation this week, pick one goal like an emergency fund or debt cut, and automate it. Leverage free U.S. resources—IRS.gov for taxes, CFPB.gov for budgets, SSA.gov for retirement—to stay on track. Consistent small steps lead to big wins; review progress monthly and celebrate milestones. Your secure future starts now.

Frequently Asked Questions

Sources & References

-

1

Generational Financial Goals for 2026 - 401k Specialist — 401kspecialistmag.com

-

2

How Americans are prioritizing money goals in 2026: survey — www.livenowfox.com

-

3

6-Step Financial Plan for 2026 - DFPI — dfpi.ca.gov

-

4

How to Achieve Your Financial Goals in 2026 — www.heffins.com

-

5

Simple steps to accomplish your 2026 money resolutions — www.fnbsf.com

-

6

How to Set and Stick to New Financial Goals in 2026 - TD Stories — stories.td.com

- 7

Useful Tools

Related Articles

How to Build a 6-Month Emergency Fund on a Minimum Wage

Building a six-month emergency fund on minimum wage might feel impossible, but it's more achievable than you think. With the right strategy and consistent effort, you can create a financial safety net...

The Best "Financial Literacy" Books Every American Should Read in 2026

Imagine standing at the edge of financial freedom, armed with knowledge that turns everyday dollars into lifelong security. In 2026, with inflation hovering around 2.5% and retirement accounts like 40...

How to Avoid "Lifestyle Creep" After a 2026 Promotion

Picture this: You've just landed that well-deserved promotion in 2026, your salary jumps by 20% or more, and suddenly you're eyeing a sleeker car, fancier dinners out, or that home upgrade you've alwa...

The Best Cashback Apps for Grocery Shopping in 2026

Imagine slashing your grocery bill by hundreds of dollars each year without clipping coupons or hunting for sales. In 2026, cashback apps make it simple for Americans to earn real money back on everyd...