How to Use Your HSA to Build Wealth for Retirement

Imagine turning your everyday health savings into a powerhouse retirement fund—one that grows tax-free and lets you withdraw money penalty-free for medical bills even after age 65. That's the hidden p...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine turning your everyday health savings into a powerhouse retirement fund—one that grows tax-free and lets you withdraw money penalty-free for medical bills even after age 65. That's the hidden potential of a Health Savings Account (HSA). Far from just a medical expense piggy bank, an HSA offers the only triple tax advantage in the U.S. tax code: contributions reduce your taxable income, growth is tax-free, and qualified withdrawals are tax-free too. In 2026, with rising healthcare costs and longer retirements, learning how to use your HSA to build wealth for retirement could add hundreds of thousands to your nest egg.

Whether you're in your 20s just starting out or nearing retirement, this guide breaks down actionable steps, investment strategies, and real-world examples tailored for Americans. We'll cover contribution limits, smart investing, advanced tactics, and integration with your broader financial plan—all backed by current 2026 rules.

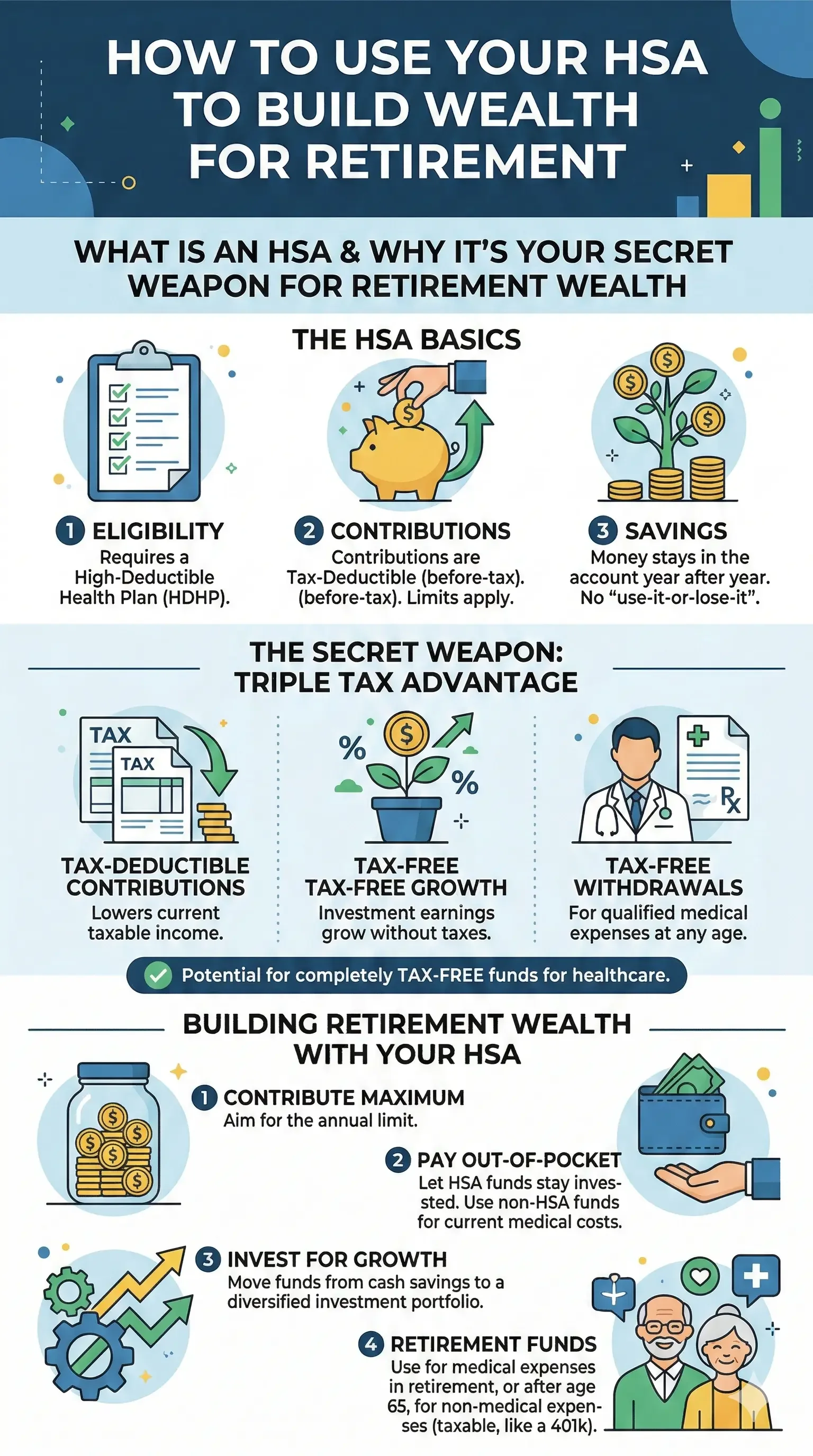

What Is an HSA and Why It's Your Secret Weapon for Retirement Wealth

A Health Savings Account pairs with a High Deductible Health Plan (HDHP) to help cover out-of-pocket medical costs tax-free. But its real magic shines in retirement planning. Unlike 401(k)s or IRAs, HSAs let you use funds for qualified medical expenses at any age without taxes or penalties, making them ideal for healthcare in your golden years—where expenses can skyrocket.

In 2026, all Bronze and Catastrophic plans on the marketplace qualify for HSAs, expanding access for more Americans seeking lower premiums. Funds roll over indefinitely, earn interest, and can be invested, turning your HSA into a stealth retirement account.

2026 HSA Contribution Limits

Maximize your tax shield by contributing the full amount:

- Individual coverage: $4,400

- Family coverage: $8,750

- Catch-up contributions (age 55+): Additional $1,000

These limits come from employer or IRS adjustments for inflation. Contributions are tax-deductible, shielding income from federal taxes—potentially saving you thousands annually depending on your bracket.

Step-by-Step: How to Invest Your HSA for Maximum Growth

Don't let your HSA sit in cash earning pennies. Once you hit your provider's minimum balance (often $1,000–$2,000), invest the rest. Providers like Fidelity offer stocks, ETFs, mutual funds, target-date funds, and even fractional shares.

Choose the Right Investments by Age and Risk Tolerance

Tailor your portfolio to your timeline:

- 20s–30s (Aggressive Growth): Go heavy on stocks or S&P 500 index funds averaging 11% historical returns. Pay minor medical bills out-of-pocket to let funds compound.

- 40s–50s (Balanced): Mix 60% stocks, 40% bonds. Target-date funds auto-adjust for simplicity.

- 60s+ (Conservative): Shift to bonds and core funds for stability, keeping 1–2 years of medical expenses in cash.

A $10,000 HSA investment at 7% annual growth hits $38,697 in 20 years—$7,724 more than in a taxable account—thanks to no tax drag.

Popular HSA Investment Options

| Investment Type | Pros | Cons | Best For |

|---|---|---|---|

| Index Funds/ETFs (e.g., S&P 500) | Low fees, 7–11% avg. returns | Market volatility | Long-term growth |

| Target-Date Funds | Auto-rebalances by retirement year | Slightly higher fees | Hands-off investors |

| Bonds/Core Funds | Stability, lower risk | Lower returns (3–5%) | Near-retirees |

| Self-Directed (Stocks, Real Estate, Crypto) | High customization | Higher risk, complexity | Experienced investors |

Select low-fee options (under 0.5%) and enable auto-sweep to invest excess cash automatically.

Advanced Strategies: Supercharge Your HSA for Retirement

Go beyond basics with proven tactics to build serious wealth.

The "Pay Out-of-Pocket" Maximizer Strategy

Pay current medical bills with cash or credit, save receipts (no expiration on reimbursements), and let your HSA grow undisturbed. Example: From age 35–65, max contributions at 7% returns while paying $4,000/year out-of-pocket yields ~$860,000 at 65, plus $120,000 in reimbursable expenses.

"Maintain a tiny cash buffer, pursue aggressive low-cost allocation and turn auto-sweep on."

Layer with Other Retirement Accounts

HSAs shine in comprehensive planning:

- In early retirement, use HSA for medical costs to keep income low during Roth conversions from traditional IRAs.

- Fund long-term care—70% of 65+ Americans need it.

- Coordinate with FSAs via Section 125 rules to avoid eligibility issues.

During job changes, use COBRA to maintain HDHP/HSA eligibility.

Common Pitfalls to Avoid

- Early Withdrawals: Non-medical uses before 65 incur income tax + 20% penalty. Let it grow!

- Cash Hoarding: Inflation erodes value; invest beyond your buffer.

- Missing Catch-Ups: 55+ folks, add that extra $1,000.

- HDHP Mismatch: Confirm your plan qualifies via Healthcare.gov.

Next Steps to Start Building Wealth Today

1. Check if your plan is HSA-eligible at Healthcare.gov.

2. Max 2026 contributions via payroll or IRA rollover.

3. Build a small cash buffer, then invest aggressively.

4. Save all medical receipts digitally.

5. Review annually—adjust as you age.

Your HSA isn't just for doctor's visits; it's a tax-free wealth machine. Start today, and by retirement, you'll thank yourself with funds ready for healthcare—and beyond.

Frequently Asked Questions

Sources & References

-

1

HSA Retirement Strategy 2026: Maximizing Tax Benefits — claritybenefitsolutions.com

-

2

HSA for 2026: Everything You Need to Know - YouTube (IRA Podcast) — www.youtube.com

-

3

HSA Investment Guide for Every Age and Goal | Truemed — www.truemed.com

-

4

A 2026 Guide to HSA Investments - SmartAsset — smartasset.com

-

5

New in 2026: More Plans Now Work with Health Savings Accounts — Healthcare.gov — www.healthcare.gov

-

6

3 Ways to Get More Out of Your HSA in 2026 - Nasdaq — www.nasdaq.com

-

7

Health Savings Account | HSA Investment Options — Fidelity — www.fidelity.com

Useful Tools

Related Articles

How to Negotiate Your Medical Bills and Reduce Hospital Debt

A surprise medical bill can hit like a truck, turning a routine hospital visit into a financial nightmare. With medical costs soaring—insurance premiums more than doubled for millions from 2025 to 202...

Health Savings Accounts (HSA): The Triple-Tax Advantage Secret

Imagine slashing your tax bill today, watching your savings grow tax-free, and pulling money out tax-free for healthcare in retirement—that's the power of a Health Savings Account (HSA). With healthca...