What Is a Personal Financial Plan and How Do You Make One?

A personal financial plan is your roadmap to financial stability and success. It's a structured strategy that connects your income, spending, debt, and savings to help you achieve your life goals—whet...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

A personal financial plan is your roadmap to financial stability and success. It's a structured strategy that connects your income, spending, debt, and savings to help you achieve your life goals—whether that's buying a home, funding your children's education, or retiring comfortably. Without a plan, your money drifts without direction. With one, every dollar works toward something meaningful.

The good news? Creating a personal financial plan doesn't require a finance degree or a six-figure income. It requires clarity about where you stand today and where you want to go tomorrow. This guide walks you through the essential components and practical steps to build a plan that actually works for your life.

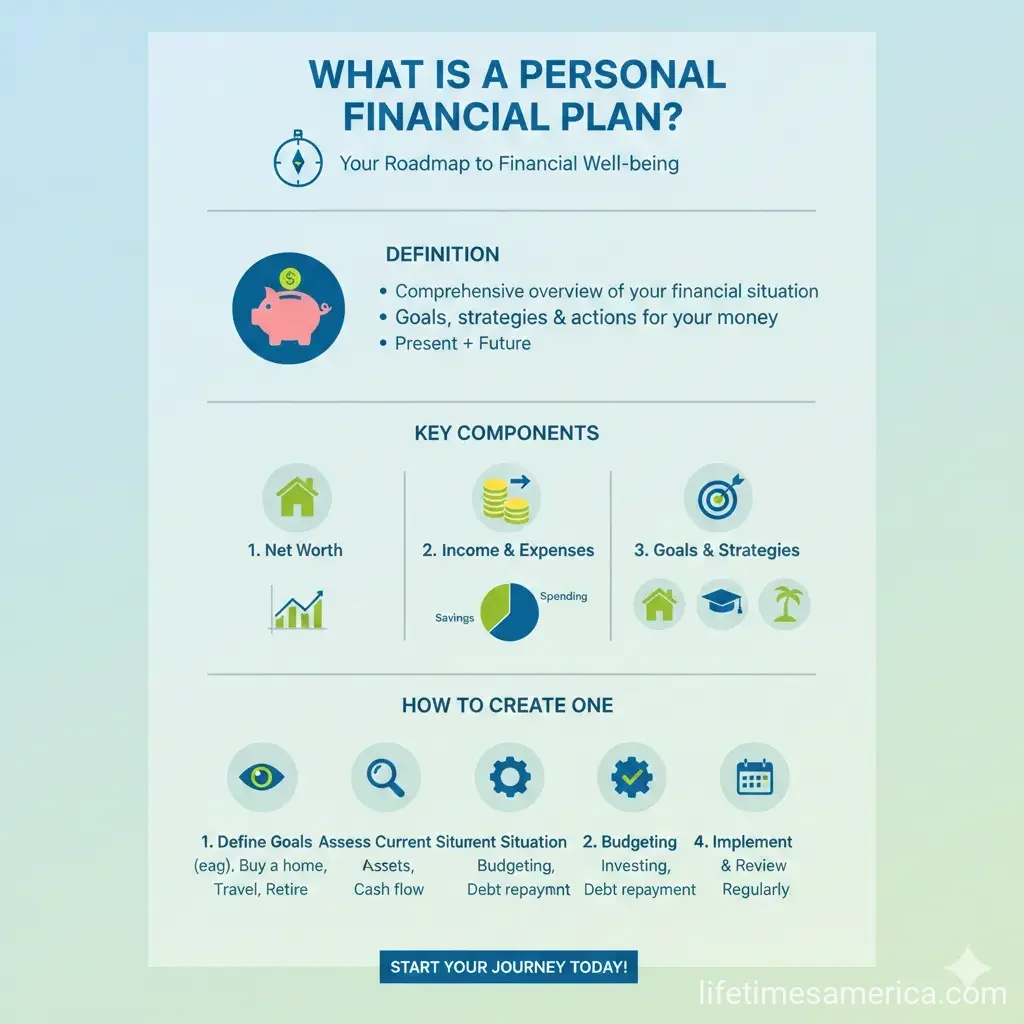

What Is a Personal Financial Plan?

A personal financial plan is a comprehensive document that outlines your financial goals, current financial situation, and the strategies you'll use to reach those goals. Think of it as a GPS for your money—it shows where you are, where you want to be, and the best route to get there.

A solid financial plan addresses multiple areas of your finances, not just one or two. It covers your income and expenses, debt management, savings, investments, insurance protection, tax strategy, and retirement planning. Each component supports the others, creating an integrated system rather than isolated financial decisions.

The key insight? Financial planning is a process, not a one-time event. Your plan evolves as your life changes—new job, growing family, inheritance, or shift in priorities. Regular reviews and adjustments keep your plan aligned with your reality.

Why You Need a Personal Financial Plan

Without a plan, you're vulnerable to financial stress and missed opportunities. A clear plan reduces uncertainty and supports better decision-making throughout the year. It helps you:

- Identify where your money actually goes each month

- Allocate income purposefully toward priorities rather than letting it slip away

- Build a safety net that protects your family from financial shocks

- Make progress toward long-term goals like retirement or homeownership

- Minimize taxes through strategic planning and use of tax-advantaged accounts

- Ensure your family is protected through appropriate insurance coverage

The Essential Components of a Personal Financial Plan

1. Clear Financial Goals

You can't create a plan without knowing what you're planning for. Start by listing your financial goals—both big and small—and assign realistic time horizons to each.

Organize your goals into three categories:

- Short-term goals (1-3 years): Building an emergency fund, paying off credit card debt, saving for a vacation, or home repairs

- Mid-term goals (3-10 years): Saving for a home down payment, funding children's college tuition, or starting a business

- Long-term goals (10+ years): Retirement, generational wealth building, or charitable giving

Clear goals make your plan measurable and keep you motivated when progress feels slow.

2. A Complete Financial Picture (Net Worth Statement)

Before you can chart your course, you need to know where you stand. Calculate your net worth—the foundation of understanding your financial position.

To determine your net worth:

- List all your assets: checking and savings accounts, retirement accounts (401(k), IRA), investment accounts, real estate, vehicles, and valuable personal property

- List all your liabilities: credit card balances, mortgages, student loans, car loans, and any other debt

- Subtract total liabilities from total assets. The result is your net worth.

This baseline helps you set realistic targets and track progress over time. Review it annually to see how your financial position is improving.

3. A Budget and Cash Flow Plan

Your budget is where financial planning becomes real. It shows where your money actually goes each month and where you can adjust spending to meet your goals.

Create a structured map of your monthly or biweekly income and expenses. Separate your expenses into two categories:

- Fixed expenses: Rent or mortgage, insurance, loan payments, utilities—costs that stay roughly the same each month

- Variable expenses: Groceries, gas, dining out, entertainment—costs that fluctuate

Don't overlook irregular but important expenses like car repairs, annual insurance premiums, property taxes, and out-of-pocket healthcare costs. A budget calculator can help ensure you capture everything.

The goal isn't to live like a miser—it's to understand where your money goes and make intentional choices about spending.

4. Debt Management Plan

If you carry debt, create a structured plan to pay it down. Track all outstanding balances, interest rates, and minimum payments.

Consider these proven strategies:

- Debt snowball method: Pay off smallest balances first for quick wins and motivation

- Debt avalanche method: Pay off highest interest-rate debt first to minimize total interest paid

- Balance transfer: Move high-interest credit card debt to a 0% promotional rate card (if available)

Reducing debt frees up cash flow for savings and investments, accelerating progress toward your other goals.

5. Emergency Fund and Liquidity

An emergency fund protects your financial plan from falling apart when life happens. Aim to build a liquid buffer that covers 3-6 months of essential expenses in an accessible savings account.

This fund absorbs unexpected costs—job loss, medical emergency, car repair—without derailing your long-term goals or forcing you into high-interest debt.

6. Retirement Planning

Retirement isn't an afterthought—it's a core section of any comprehensive financial plan. Start by estimating how much you'll need in retirement and when you want to retire.

Key retirement accounts to maximize:

- 401(k) or 403(b): Employer-sponsored plans with tax-deferred growth. Contribute at least enough to capture any employer match—it's free money.

- Traditional IRA or Roth IRA: Individual retirement accounts with annual contribution limits set by the IRS. For 2026, contribution limits are subject to annual adjustments.

- Social Security: Plan to claim strategically. Waiting until age 70 results in higher monthly benefits than claiming at 62.

Review your investment allocations annually to ensure they match your time horizon and risk tolerance.

7. Insurance Coverage

Insurance is critical protection that keeps your family's finances on track if something happens to you. Your plan should include:

- Life insurance: Protects your family's income if you pass away. Term life is typically affordable for most households.

- Disability insurance: Replaces income if you become unable to work due to illness or injury

- Health insurance: Protects against catastrophic medical costs

- Homeowners or renters insurance: Covers your property and liability

- Umbrella liability coverage: Provides additional liability protection beyond standard policies

Review your coverage annually to ensure it's adequate without overpaying for unnecessary policies.

8. Tax Optimization Strategy

Integrate tax planning into your financial structure to keep more of what you earn. Key strategies include:

- Maximizing contributions to tax-deferred retirement accounts (401(k), traditional IRA)

- Using Health Savings Accounts (HSAs) if you have a high-deductible health plan

- Reviewing IRS withholding to avoid overpaying taxes or owing a large bill at tax time

- Taking advantage of tax deductions and credits you qualify for

- Coordinating with a tax professional or accountant, especially if you're self-employed or have complex income

Use IRS tools and resources at irs.gov to review your withholding and ensure you're optimizing your tax situation.

How to Build Your Personal Financial Plan: Step-by-Step

Step 1: Assess Your Current Situation

Document your complete financial picture: total income, all expenses (fixed and variable), savings balances, and outstanding debt. This baseline identifies where financial pressure exists and where adjustments are possible.

Step 2: Define Your Priorities

Identify your primary financial objectives for the next 1-5 years. Common priorities include emergency savings, debt reduction, retirement contributions, essential purchases, and future planning needs. Limit your list to a small number of targets so you can allocate income with purpose.

Step 3: Develop Strategies for Each Area

For each financial component—investments, debt, savings, insurance, taxes—design specific action steps. Decide how much to save, where to invest, how to manage risk, and when to review and adjust.

Step 4: Implement Your Plan

Put your strategies into action by selecting the right financial products and accounts that fit your needs. Set up automatic transfers to savings and retirement accounts. Open necessary accounts. Enroll in workplace benefits. Make it automatic and stress-free whenever possible.

Step 5: Review and Adjust Regularly

Schedule annual reviews of your complete financial plan. Life changes—new job, marriage, children, inheritance, health issues—require plan adjustments. Markets shift. Tax laws change. Your priorities may evolve. Regular reviews keep your plan aligned with your actual life.

Common Financial Planning Mistakes to Avoid

- No written plan: Vague goals and mental notes don't work. Write it down.

- Ignoring insurance: One unexpected illness or injury can derail years of financial progress.

- No emergency fund: Without a buffer, unexpected expenses force you into debt.

- Chasing short-term trends: Investment strategy should align with long-term goals, not market noise.

- Neglecting tax strategy: Failing to optimize taxes means overpaying and reducing wealth-building capacity.

- Setting it and forgetting it: Life changes. Your plan must evolve with your circumstances.

Next Steps: Start Your Financial Plan Today

You don't need to be perfect or have all the answers to start. Begin with what you can control right now:

- Spend one hour documenting your current financial picture—income, expenses, assets, and debt

- List your top three financial goals for the next year

- Set up automatic transfers to a savings account, even if it's just $25 per paycheck

- Review your workplace retirement plan and ensure you're capturing any employer match

- Schedule a calendar reminder to review your plan in three months

A personal financial plan is one of the most powerful tools you have for building the life you want. It transforms vague wishes into concrete action and gives you confidence that your money is working toward something meaningful. Start today, stay consistent, and adjust as needed. Your future self will thank you.

Frequently Asked Questions

Sources & References

-

1

The 8 Essential Elements of a Complete Financial Plan — www.plancorp.com

-

2

The Essential Guide to Financial Plan in Financial Management 2026 — www.matthewsheppardbrown.com

-

3

How to Build a Simple Financial Plan for 2026 — www.onedigital.com

-

4

Financial Planning for Beginners: A Guide — www.heygotrade.com

-

5

8 Keys to Good Financial Plans — www.schwab.com

-

6

How to Plan Your Finances for 2026: 7 Strategies — www.westernsouthern.com

Related Articles

How to Build a 6-Month Emergency Fund on a Minimum Wage

Building a six-month emergency fund on minimum wage might feel impossible, but it's more achievable than you think. With the right strategy and consistent effort, you can create a financial safety net...

The Best "Financial Literacy" Books Every American Should Read in 2026

Imagine standing at the edge of financial freedom, armed with knowledge that turns everyday dollars into lifelong security. In 2026, with inflation hovering around 2.5% and retirement accounts like 40...

How to Avoid "Lifestyle Creep" After a 2026 Promotion

Picture this: You've just landed that well-deserved promotion in 2026, your salary jumps by 20% or more, and suddenly you're eyeing a sleeker car, fancier dinners out, or that home upgrade you've alwa...

The Best Cashback Apps for Grocery Shopping in 2026

Imagine slashing your grocery bill by hundreds of dollars each year without clipping coupons or hunting for sales. In 2026, cashback apps make it simple for Americans to earn real money back on everyd...