What Is Renters Insurance and Is It Worth It?

Imagine coming home to find your apartment flooded from a burst pipe, your laptop stolen, or a guest slipping on a wet floor and suing you for medical bills. These aren't rare disasters—they happen ev...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine coming home to find your apartment flooded from a burst pipe, your laptop stolen, or a guest slipping on a wet floor and suing you for medical bills. These aren't rare disasters—they happen every day to renters across America. Renters insurance steps in as your financial safety net, often for less than the cost of a couple of takeout meals a month. But is it really worth it in 2026? Let's break it down so you can decide with confidence.

What Is Renters Insurance?

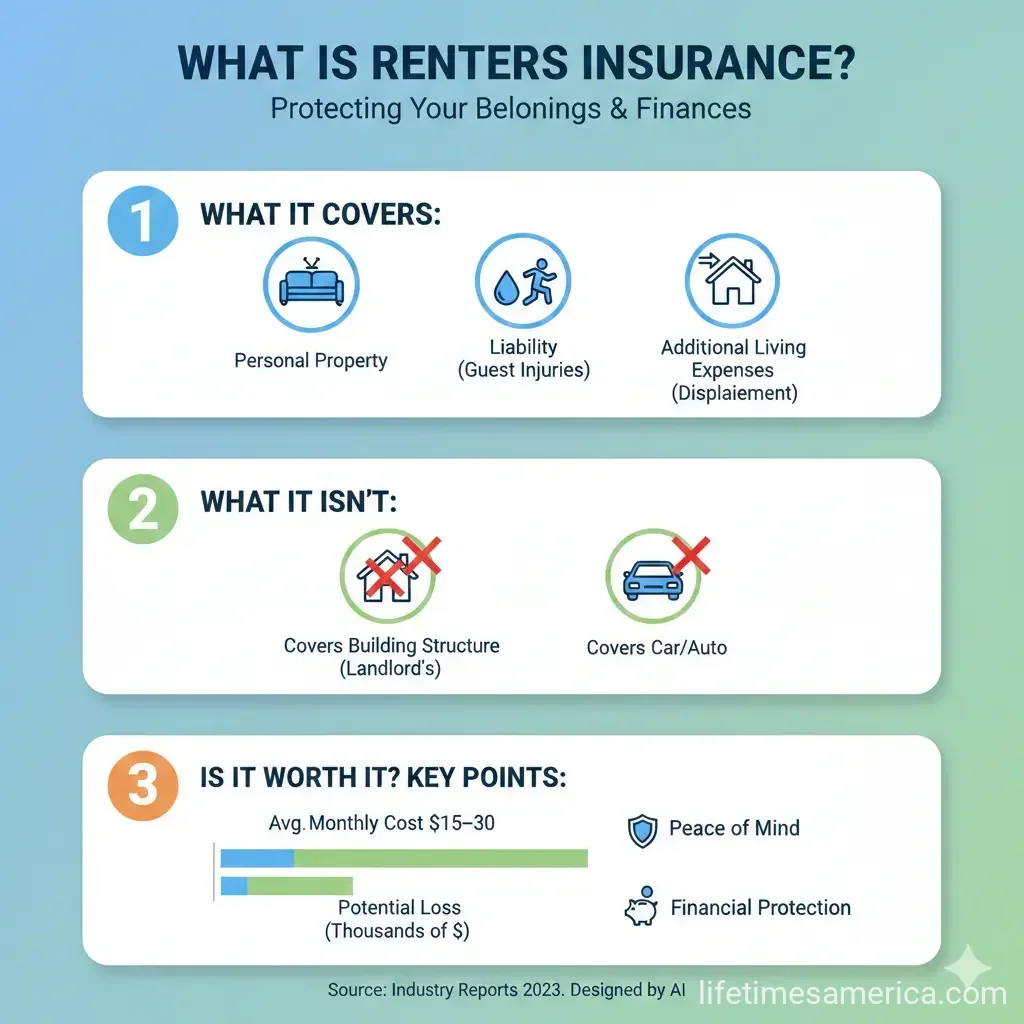

Renters insurance, also known as HO-4 insurance, is a policy that protects your personal belongings and provides liability coverage when you rent an apartment, house, or condo. Unlike homeowners insurance, it doesn't cover the building structure—that's your landlord's responsibility—but it safeguards everything you own inside.

Your landlord's policy might handle repairs to the property itself, but it won't touch your stuff or any accidents you're liable for. That's where your renters policy comes in, covering theft, fire, vandalism, and more.

How Does Renters Insurance Work?

You pay a monthly or annual premium, typically $10–$30 depending on your location, coverage amount, and deductible. In exchange, if a covered event occurs, you file a claim. After paying your deductible (say, $500–$1,000 out-of-pocket), the insurer reimburses you up to your policy's coverage limits.

For example, if your $2,000 TV is damaged in a fire and your deductible is $500, you'd pay $500, and the policy covers the remaining $1,500 (assuming it's within limits). Higher deductibles lower your premiums, making it a smart tweak for low-risk renters.

What Does Renters Insurance Cover?

A standard policy includes three core protections: personal property, liability, and loss of use. Here's what they mean for you.

Personal Property Coverage

This reimburses you for stolen, damaged, or destroyed belongings like clothes, furniture, electronics, and appliances. Covered perils include fire, smoke, lightning, theft, vandalism, windstorms, and water damage from leaks (not floods).

- Electronics and jewelry: Often has sublimits, like $1,500 for jewelry or $200 for cash—add riders for high-value items.

- Kids' gear: Toys, bikes, and school supplies are protected.

- Replacement cost: Many policies pay to replace items at current prices, not depreciated value.

Liability Protection

If someone gets hurt in your rental or you accidentally damage someone else's property, this covers medical bills, legal fees, and lawsuits—up to $100,000 or more. It even applies off-site, like if your dog bites a neighbor at the park.

Landlords often require at least $100,000 in liability to protect their property from tenant-caused damage, like a grease fire spreading.

Loss of Use (Additional Living Expenses)

If a covered peril makes your place unlivable, this pays for hotel stays, short-term rentals, food, laundry, pet boarding, and storage—typically up to 30% of your personal property limit.

What Renters Insurance Doesn't Cover

Standard policies exclude floods, earthquakes, pest damage, wear-and-tear, and your roommate's stuff (each needs their own policy). Car damage, business equipment, and intentional acts are also out. For floods, add separate NFIP coverage via FEMA; earthquakes need endorsements.

Pro tip: Review exclusions carefully—policies vary by state and insurer.

Is Renters Insurance Required?

No U.S. state or federal law mandates renters insurance, but over 60% of landlords do as a lease condition. It's especially common in high-rises in states like Florida, Texas, Georgia, California, and New York.

In 2026, with rising natural disasters from climate shifts, more property managers in hurricane-prone areas like Florida are enforcing it. Check your lease: You might need proof of coverage to sign or renew. Some states allow landlords to require it, but local laws vary—consult your attorney if unsure.

Cost of Renters Insurance in 2026

Average premiums range from $10–$15 monthly nationwide, or $120–$180 yearly, for $30,000–$50,000 in personal property and $100,000 liability. Costs vary by:

- Location: Urban areas like New York or Miami run $20–$30/month due to theft and storm risks.

- Coverage amount: $40,000 property + $100,000 liability ≈ $15/month.

- Deductible: $1,000 deductible saves $5–$10/month vs. $500.

- Discounts: Bundling with auto insurance (10–25% off), claim-free history, or smart home devices.

In Massachusetts, expect $12–$20/month for basic coverage. Shop around—online insurers like Lemonade offer quick quotes in 30+ states.

Is Renters Insurance Worth It?

Absolutely, for most Americans. The average renter owns $30,000+ in belongings—a burglary could wipe that out. At $15/month, it pays for itself with one claim. Real risks in 2026 include wildfires in California, hurricanes in Florida, and urban theft spikes.

Without it, you're on the hook for repairs, lawsuits (average slip-and-fall claim: $30,000), or rebuilding after eviction. Even if your lease doesn't require it, the peace of mind outweighs the tiny cost—especially with inflation making replacements pricier.

How to Get Renters Insurance: Actionable Steps

- Inventory your stuff: List items, values, and photos—apps like Sortly help.

- Choose coverage: Aim for replacement cost equaling your belongings' value + $100,000 liability.

- Compare quotes: Use sites like Policygenius or Insurify for 5–10 carriers. Check state availability.

- Customize: Add flood/earthquake riders if needed; raise deductible if you're risk-averse.

- Buy and prove: Get a declarations page for your landlord. Pay annually for savings.

Roommates? Each get individual policies—joint ones are rare and tricky.

Protect Your Future Today

Renters insurance isn't just smart—it's essential in 2026's unpredictable world. For pennies a day, it shields your wallet from theft, disasters, and lawsuits. Take 15 minutes now: Inventory your gear, grab quotes, and secure a policy. Your future self (and landlord) will thank you. Visit usa.gov for state insurance resources or your state's DOI site for licensed carriers.

Frequently Asked Questions

Sources & References

-

1

Is Renters Insurance Worth It in 2026? Real Costs, Coverage, and Risks — www.kanguroseguro.com

-

2

Renters Insurance Explained: Why You Should Get a Policy in 2026 — www.advanceamerica.net

-

3

What Does Renters Insurance Cover in 2026 - Lemonade — www.lemonade.com

-

4

Renters Insurance | Mass.gov — www.mass.gov

-

5

Renting Your Home? Protect Your Belongings with Renters Insurance — content.naic.org

-

6

Renters Insurance Requirements for Landlords 2026 - Obie — www.obieinsurance.com

-

7

What Is Renters Insurance and What Does It Cover? | Allstate — www.allstate.com

- 8

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...