What Is Homeowners Insurance and What Does It Cover?

Imagine coming home to find your roof torn off by a fierce storm, water pouring into your living room, and your prized family heirlooms ruined. Without the right protection, this nightmare could drain...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine coming home to find your roof torn off by a fierce storm, water pouring into your living room, and your prized family heirlooms ruined. Without the right protection, this nightmare could drain your savings. Homeowners insurance steps in as your financial safety net, covering repairs, replacements, and even temporary housing while you recover.

Whether you're a first-time buyer in Texas or a long-time owner in Florida, understanding what is homeowners insurance and what does it cover is crucial. In the United States, most mortgage lenders require it to protect their investment in your property. This guide breaks down the essentials, policy types, and tips to get the coverage you need in 2026.

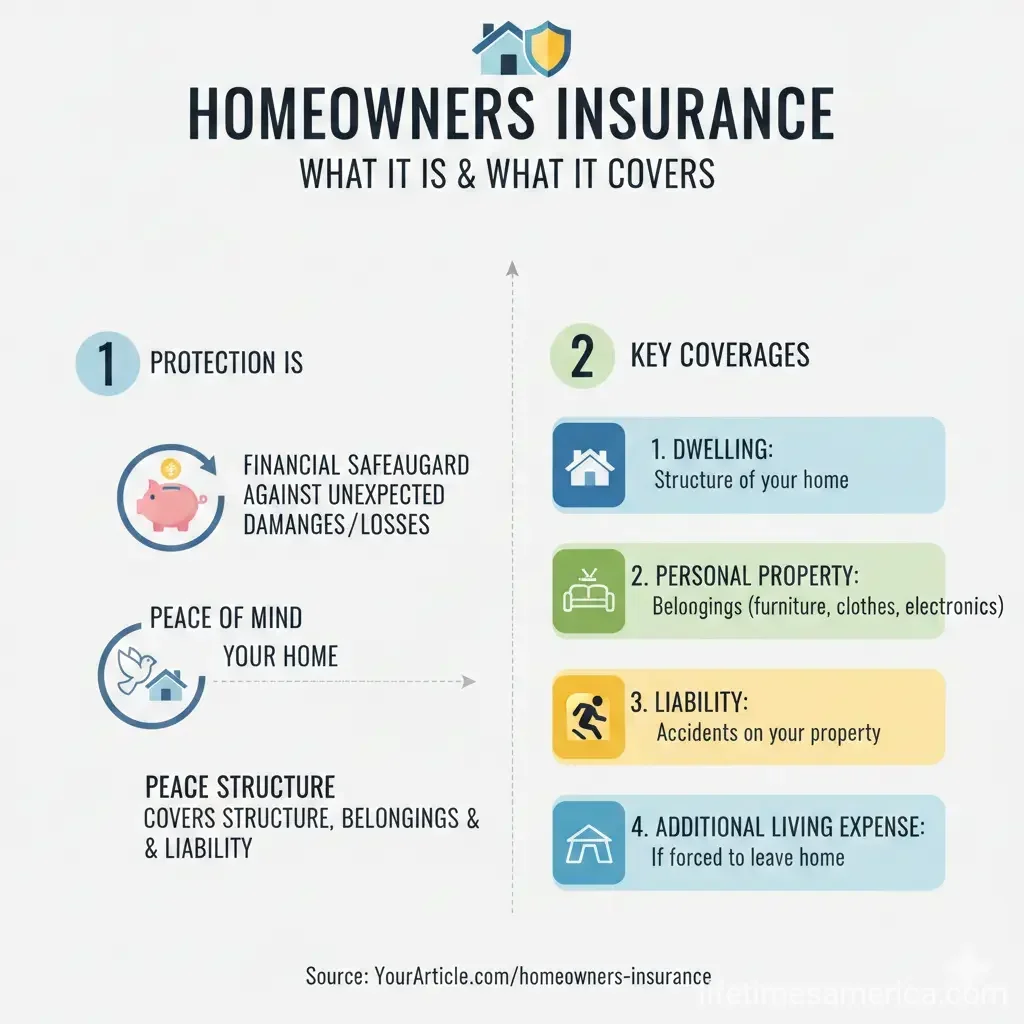

What Is Homeowners Insurance?

Homeowners insurance is a policy that protects your home, personal belongings, and financial assets against damage, theft, or liability claims from covered events, known as perils. It typically includes coverage for the dwelling itself, other structures, contents inside your home, loss of use, liability, and medical payments.

In 2026, with rising climate risks and stabilizing premiums in many areas, this insurance remains a cornerstone of homeownership. Policies pay to repair or rebuild after disasters like fire, windstorms, or hail—common claims according to the Insurance Information Institute.

Why Do Americans Need It?

Beyond lender requirements, homeowners insurance safeguards against unexpected losses. For instance, if a guest slips on your icy driveway and sues, liability coverage handles legal fees and settlements—often starting at $100,000 but recommended up to $300,000 or more. In high-risk states like California or Louisiana, it provides peace of mind amid wildfires or hurricanes.

- Financial Protection: Covers repair costs that could otherwise bankrupt you.

- Legal Shield: Defends against lawsuits for injuries on your property.

- Temporary Relief: Pays for hotel stays if your home is uninhabitable.

Standard Coverages in Homeowners Insurance

Most U.S. policies bundle six core coverages, with limits based on your dwelling amount. For a $300,000 home, expect other structures at 10% ($30,000), personal property at 50% ($150,000), and so on.

Dwelling Coverage

This pays to repair or rebuild your home's structure—walls, roof, floors, windows, and built-in appliances like your HVAC system. Attached garages or decks qualify too. Covered perils include fire, lightning, wind, hail, and falling objects, unless excluded.

Choose replacement cost (new materials at current prices) over actual cash value (depreciated) for better protection.

Other Structures Coverage

Protects detached buildings like sheds, fences, pools, or guest houses—typically 10% of your dwelling limit. If a storm topples your backyard gazebo in Ohio, this coverage rebuilds it.

Personal Property Coverage

Covers your belongings—furniture, clothes, electronics, jewelry—against theft or damage, often at 50-70% of dwelling coverage. High-value items like engagement rings may need schedulers for full value. Create a home inventory video or list to speed claims.

Loss of Use (Additional Living Expenses)

If a covered loss makes your home unlivable, this pays for hotels, meals, and storage—usually 20-30% of dwelling coverage. After a kitchen fire in New York, it could cover an Airbnb for months.

Liability Coverage

Handles injuries or property damage you cause to others, including legal defense. Limits start at $100,000; add an umbrella policy for $1 million+ if you have assets like a 401(k).

Medical Payments Coverage

Pays minor medical bills for guests injured on your property, regardless of fault—often $1,000-$5,000 per person.

Common Perils and Exclusions

Standard policies cover named or open perils like fire, theft, vandalism, windstorms, hail, lightning, and explosions. Wind and hail top claims lists.

Key Exclusions: Floods, earthquakes, wear-and-tear, pests, and war. Get separate flood insurance via FEMA's National Flood Insurance Program (NFIP) if in a flood zone—mandatory in many coastal areas. Earthquakes need add-ons, especially in California.

Types of Homeowners Insurance Policies

Policies vary by form, from basic to comprehensive. HO-3 is most common.

| Policy Type | Coverage Style | Best For |

|---|---|---|

| HO-2 (Broad Form) | Named perils for home and contents | Budget-conscious owners |

| HO-3 (Special Form) | Open perils for dwelling; named for contents | Most homes |

| HO-5 (Comprehensive) | Open perils for everything | Low-risk, premium homes |

| HO-8 (Modified) | Named perils; actual cash value | Older homes |

HO-5 offers the broadest protection but is limited to well-maintained homes in safe areas.

Deductibles, Limits, and Premiums in 2026

Your deductible is out-of-pocket before coverage kicks in—$1,000 is common; higher ones lower premiums. Coverage limits tie to dwelling amount; other sections are percentages thereof.

In 2026, premiums stabilize after rises, influenced by climate risks and AI underwriting. Shop via USA.gov's resources or state insurance departments for quotes.

Add-Ons and Customizations for Better Protection

- Flood/Earthquake: Separate NFIP policies average $700/year.

- Sewer Backup/Water Leak: Covers sudden backups.

- Umbrella Liability: Extra $1M+ for lawsuits.

- High-Value Items: Floater for jewelry/art.

Tailor to your needs—e.g., pool owners add liability boosts.

Practical Tips to Maximize Your Policy

- Inventory Belongings: Use apps to document for faster claims.

- Review Annually: Update for renovations or life changes.

- Bundle Policies: Save 10-25% with auto insurance.

- Improve Home: Discounts for storm shutters or security systems.

- Shop Around: Compare via independent agents.

Next Steps for Your Homeowners Insurance

Don't wait for disaster—get quotes from at least three insurers today. Use tools from the National Association of Insurance Commissioners (NAIC) at content.naic.org or your state's department of insurance. Review your policy for 2026 updates, especially with climate trends. Proper coverage lets you focus on living, not worrying.

Frequently Asked Questions

Sources & References

-

1

What Does Homeowners Insurance Cover? Complete Guide — www.nerdwallet.com

-

2

What is Homeowners Insurance and What Does it Cover? — www.statefarm.com

-

3

What is covered by standard homeowners insurance? | III — www.iii.org

-

4

Homeowners Insurance: Coverage types and benefits — content.naic.org

-

5

What Does Home Insurance Cover: 2025 Guide — openly.com

-

6

What Does Homeowners Insurance Cover? — www.allstate.com

-

7

What Does Homeowners Insurance Cover? — www.travelers.com

-

8

How insurance is shaping homeownership in 2026 - VIU by HUB — www.viubyhub.com

-

9

2026 Home Insurance Trends & Predictions | Matic — matic.com

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...