Debt Consolidation Loans: How They Work and When to Use One

Struggling with multiple credit card bills piling up each month? You're not alone—millions of Americans face high-interest debt that feels impossible to tackle. A debt consolidation loan could be your...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Struggling with multiple credit card bills piling up each month? You're not alone—millions of Americans face high-interest debt that feels impossible to tackle. A debt consolidation loan could be your path to simpler payments and real savings, but only if used wisely.

In this guide, we'll break down exactly how debt consolidation loans work, when they make sense for your situation, and practical steps to get started in 2026. Whether you're juggling credit cards, medical bills, or personal loans, understanding this tool can help you regain control of your finances.

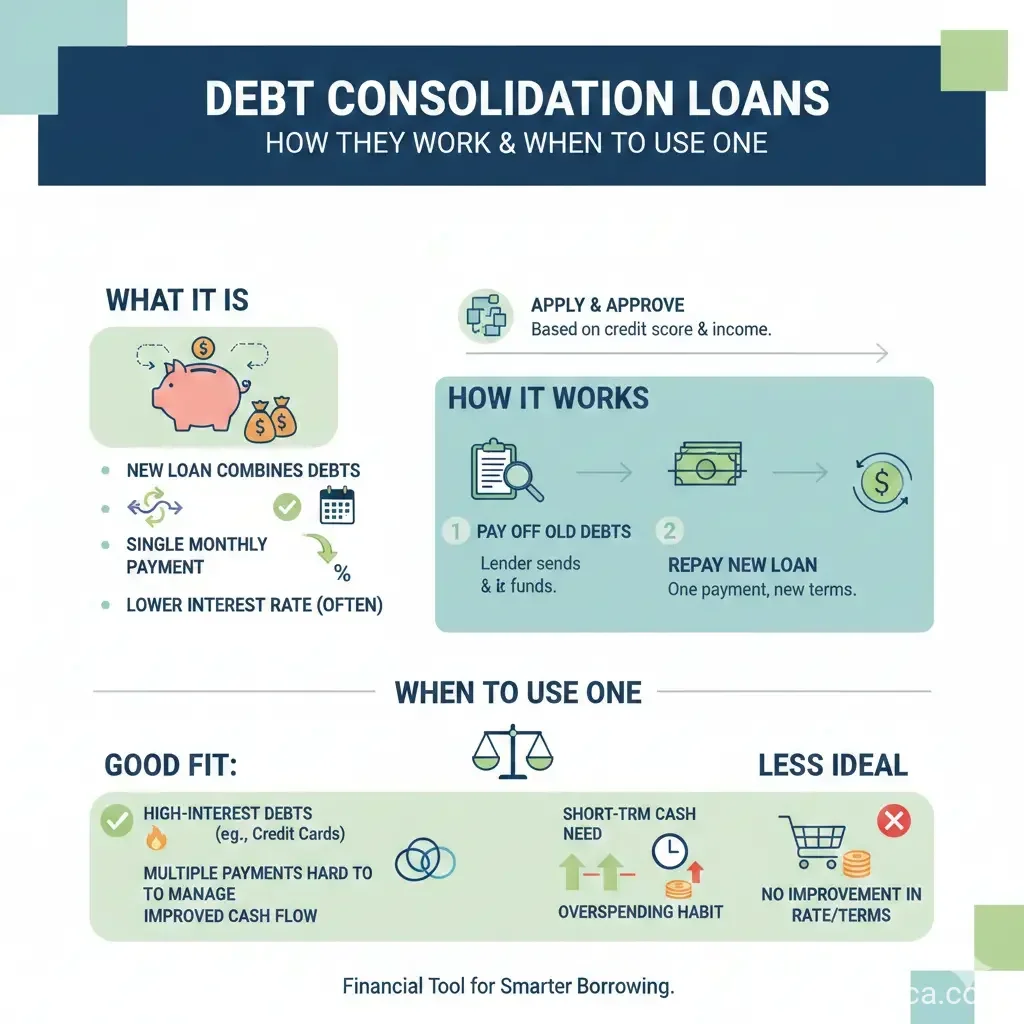

What Is a Debt Consolidation Loan?

Debt consolidation involves combining multiple debts into one single loan with a fixed monthly payment. Instead of tracking several due dates and rates, you make just one payment to the new lender.

These are typically unsecured personal loans, meaning no collateral like your home or car is required. Loan amounts range from $1,000 to $50,000, with some lenders offering up to $100,000. Repayment terms span 1 to 10 years, and funds often arrive within one business day after approval.

Common debts you can consolidate include:

- Credit card balances (often at 20%+ APR)

- Medical bills

- Retail store cards

- Unsecured personal loans

How It Differs from Other Options

Unlike balance transfer cards with temporary 0% APR promo periods (3-5% fees), debt consolidation loans offer fixed rates without expiration. Secured options like home equity loans (HELOCs) require collateral and carry foreclosure risks but may yield lower rates.

| Option | Upfront Costs | Repayment Terms | Collateral | Credit Needed |

|---|---|---|---|---|

| Debt Consolidation Loan | 0%-12% origination fee | 1-7 years | No | Good (670+) |

| Balance Transfer Card | 3%-5% fee | No set term | No | Good |

| Home Equity Loan/HELOC | 2%-5% closing costs | Up to 30 years / 10+20 years | Yes | 680+ |

How Debt Consolidation Loans Work Step by Step

The process mirrors applying for a personal loan but focuses on payoff efficiency.

- Calculate your total debt: Add up balances. Example: $5,000 at 20% APR, $2,000 at 25%, $1,000 at 16% = $8,000 total.

- Check your credit: Scores above 740 qualify for best rates (often under 10%); 670-739 may work but at higher rates.

- Apply: Lenders review income, debt-to-income ratio (DTI), and credit reports.

- Get funds and pay off debts: Use the lump sum to clear old accounts; some lenders pay creditors directly.

- Make one payment: Fixed rate and term simplify budgeting.

If your new rate is lower than your old ones—say, dropping from 20% average to 8-12%—you'll save on interest and pay off faster.

Pros and Cons of Debt Consolidation Loans

Debt consolidation simplifies life but isn't a magic fix. Here's a balanced view:

Key Pros

- Lower interest rates: Ideal if consolidating high-APR credit cards.

- Single payment: Easier tracking reduces late fees.

- Credit boost potential: Paying off revolving debt improves scores over time.

- Fixed terms: Predictable payments help budgeting.

Potential Cons

- Origination fees (0-12%) add upfront costs.

- Temptation to rack up old cards again.

- May extend debt if term is too long.

- Not ideal for poor credit (high rates or denial).

"Debt consolidation reduces the interest rate on your debt, lowers monthly payments and simplifies bill paying."

When Should You Use a Debt Consolidation Loan?

Use one when you have good credit (670+ FICO), multiple high-interest debts, and discipline to avoid new spending. It's worth it if the new rate beats your averages and monthly payment fits your budget.

Ideal scenarios:

- Multiple cards over 18% APR.

- DTI under 36% (lenders prefer this).

- Stable income to qualify.

Avoid if:

- Credit score below 670 (consider nonprofit debt management instead).

- You can't resist credit cards.

- Total debt exceeds what you can borrow affordably.

In 2026, with average credit card APRs near 21%, consolidation to 10-12% rates can save thousands.

How to Get a Debt Consolidation Loan in 2026

Shop smart—compare at least three lenders. Check credit unions, online banks, and platforms like those partnered with Experian or Bankrate.

Steps to Apply

- Pull free credit reports at AnnualCreditReport.com (weekly access).

- Use prequalification tools (soft pulls won't hurt scores).

- Gather docs: ID, income proof (W-2s, pay stubs), bank statements.

- Apply; expect decision in minutes.

- Close and pay off debts immediately.

Tip: Nonprofit credit counseling via NFCC.org offers debt management plans (DMPs) at ~8% rates without a new loan—great alternative if credit is iffy.

Fair Credit Reporting Act (FCRA) protects your rights; dispute errors before applying.

Debt Consolidation vs. Alternatives

| Method | Best For | Credit Impact | Rates |

|---|---|---|---|

| Debt Consolidation Loan | Good credit, high-interest unsecured debt | Short dip, then improves | 8-15% |

| Debt Management Plan | Any credit, credit cards | Neutral | ~8% |

| Debt Settlement | Hardship, poor credit | Damages score | N/A (forgiven debt) |

Next Steps to Simplify Your Debt

Ready to act? List your debts today, check your score at CreditKarma or directly from Equifax/TransUnion, and prequalify with lenders. If overwhelmed, contact a nonprofit counselor via NFCC.org for free advice. Consistent payments on a consolidation loan can make you debt-free faster—start now for a brighter financial future.

Frequently Asked Questions

Sources & References

-

1

How Debt Consolidation Loans Work - Bankrate — www.bankrate.com

-

2

What Is Debt Consolidation and How Does It Work? - Experian — www.experian.com

-

3

What is debt consolidation? | Fulton Bank — www.fultonbank.com

-

4

Debt Consolidation & Relevant Legal Considerations - Justia — www.justia.com

- 5

-

6

Is Debt Consolidation Worth It? A 2026 Analysis — www.peopledrivencu.org

-

7

Debt Consolidation Explained — www.luminate.bank

Related Articles

How to Handle Medical Debt in the USA

Imagine opening your mailbox to find a hospital bill for $5,000 after what you thought was a routine visit. You're not alone—millions of Americans face this reality every year, with medical debt total...

Workers Compensation Benefits: What You Are Financially Entitled To

If you've been injured at work, understanding your financial entitlements under workers' compensation can make a real difference in your recovery and financial stability. Workers' compensation benefit...

What Is a Structured Settlement and Can You Sell It for Cash?

Imagine winning a hard-fought personal injury lawsuit only to face a tough choice: take a lump sum that could vanish quickly or opt for steady payments that last a lifetime. That's the world of struct...

What Is Bankruptcy Chapter 7 vs Chapter 13? A Plain-English Guide

Imagine staring at a pile of medical bills, credit card statements, and mortgage notices that keep you up at night. You're not alone—millions of Americans face overwhelming debt each year, and bankrup...