Workers Compensation Benefits: What You Are Financially Entitled To

If you've been injured at work, understanding your financial entitlements under workers' compensation can make a real difference in your recovery and financial stability. Workers' compensation benefit...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you've been injured at work, understanding your financial entitlements under workers' compensation can make a real difference in your recovery and financial stability. Workers' compensation benefits are designed to provide medical care, wage replacement, and other support when you're hurt on the job—but the specifics of what you're entitled to vary significantly depending on where you work and the nature of your injury. This guide walks you through the key benefits you may qualify for and how to navigate the system.

Understanding Workers' Compensation Benefits

Workers' compensation is a form of insurance providing medical benefits and wage replacement to employees injured during employment. Every state has its own workers' compensation laws, defining who must carry coverage, how claims are filed, and what benefits are available. The system is designed to protect you by ensuring medical care and wage replacement under state statutes, while also protecting employers from lawsuits.

The key principle behind workers' compensation is straightforward: if you're injured at work, your employer's insurance should cover your medical expenses and replace a portion of your lost wages while you recover. However, the amount you receive depends on several factors, including your state, your average weekly wage, and the severity of your injury.

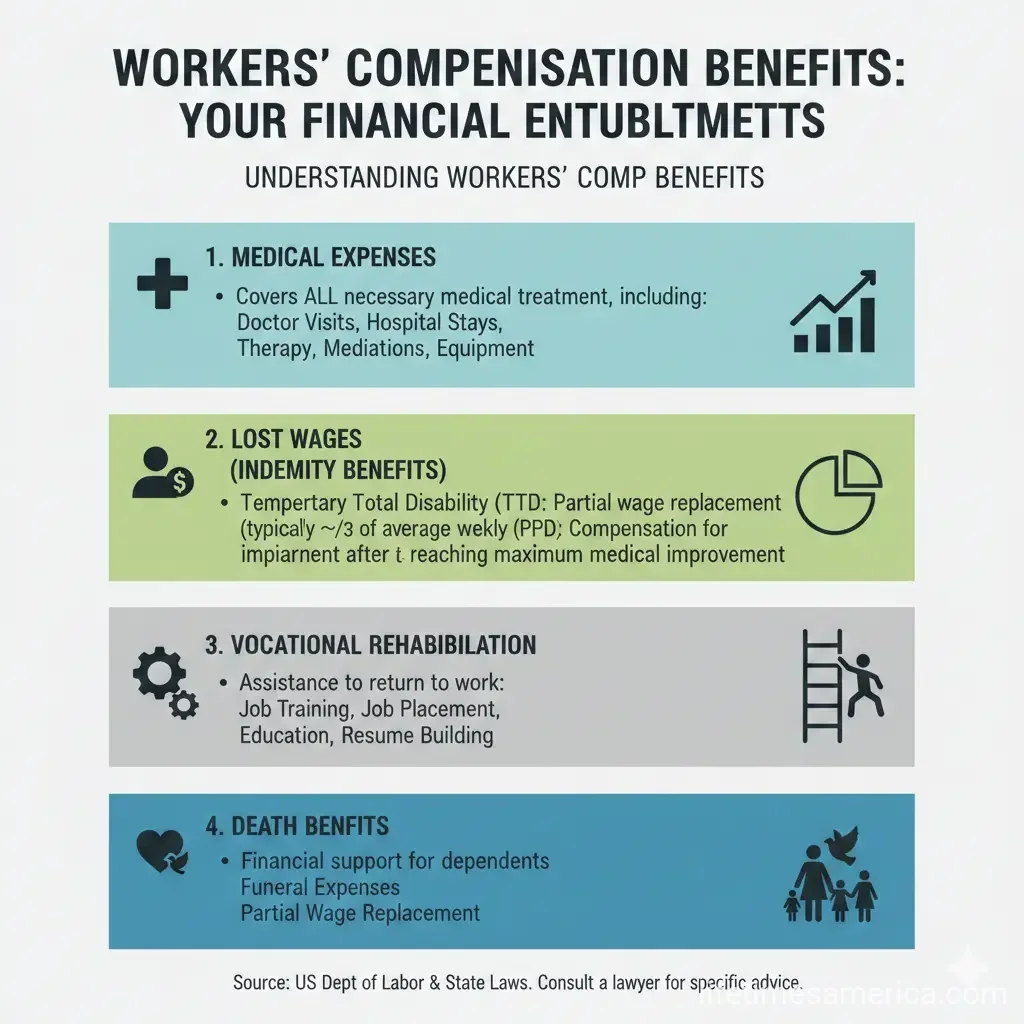

Types of Workers' Compensation Benefits

Medical Benefits

Medical benefits cover all reasonable and necessary treatment related to your work injury. This includes doctor visits, hospital care, surgery, physical therapy, medications, and medical equipment. Your employer's workers' compensation insurance pays these bills directly, so you typically don't pay out of pocket for covered medical treatment.

Temporary Total Disability (TTD)

If your injury prevents you from working temporarily, TTD benefits replace a portion of your lost wages while you're unable to work. Most states pay between 60-70% of your average weekly wage, up to a state-defined maximum. For example, in Nebraska, the maximum weekly benefit rate for TTD increased to $1,166.00 for accidents occurring in 2026. In Oklahoma, the maximum weekly TTD benefit is $1,128.66 for 2026.

These benefits continue until you're able to return to work or transition to permanent disability status.

Permanent Total Disability (PTD)

If your injury prevents you from ever returning to work, you may qualify for PTD benefits. These provide ongoing wage replacement, typically calculated as a percentage of your average weekly wage with a state-determined maximum. In Illinois, the maximum weekly benefit for PTD increased to $2,008.60 for accidents occurring from January 15, 2026 to July 14, 2026. PTD benefits may continue for life, depending on your state's laws.

Permanent Partial Disability (PPD)

PPD benefits compensate you for permanent loss of function or earning capacity resulting from your work injury. This might apply if you lose a limb, suffer permanent scarring, or experience reduced mobility. In Oklahoma, the maximum weekly PPD/PPI benefit remains at $375 for accidents occurring on or after July 1, 2025. Some states use a schedule that assigns specific dollar amounts to different body parts, while others calculate benefits based on your wage loss.

Death Benefits

If a work-related injury results in death, surviving family members may receive death benefits. In Kentucky, death benefits vary based on family composition, with maximums ranging from $458.89 to $871.36 per week depending on whether there's a widow, widower, or children. These benefits help replace the deceased worker's income for the family.

2026 Benefit Rate Updates

Benefit rates are adjusted annually in most states to account for inflation and wage growth. Rising wages increase indemnity benefits, which are calculated based on a percentage of an employee's pre-injury earnings. This is particularly important in states with higher minimum wages. For instance, California's minimum wage is set to increase to $16.90 per hour starting January 1, 2026.

Several states have updated their mileage reimbursement rates for 2026. Nebraska, Oklahoma, and Illinois all increased their mileage reimbursement rates to $0.725 beginning January 1, 2026. This covers travel to and from medical appointments related to your work injury.

Important Changes and Trends for 2026

States are expanding workers' compensation protections in 2026. Several states have introduced or are considering new legislation that may affect your benefits:

- Mental Health Coverage: Kentucky's proposed HB 26 would expand coverage to include mental health conditions like PTSD for first responders, even when not directly resulting from physical injuries.

- Provider Choice: Indiana's proposed HB 1069 would allow injured workers to choose their attending physician, regardless of injury date, giving you more control over your medical care. Washington's HB 2218 and SB 5847 similarly emphasize your right to seek medical treatment with a provider of your choice.

- Medical Fee Schedules: Missouri is considering legislation to establish standardized healthcare provider fee schedules, ensuring more consistent and transparent pricing.

Employers are facing a largely stable workers' compensation market in 2026, with modest rate movements and strong competition. This stability may benefit employees by ensuring consistent coverage and claims processing.

Tax Implications of Workers' Compensation

Workers' compensation benefits are generally not taxable as income. This is an important distinction—you won't owe federal income tax on most workers' compensation payments. However, there's one significant exception: if your workers' compensation benefits overlap with Social Security Disability Insurance (SSDI), the combined benefits may make part of the payment count as taxable income. Additionally, interest paid on delayed settlements can be taxable.

How to File a Workers' Compensation Claim

Filing a claim is crucial to accessing your benefits. Here's what you need to do:

- Report the injury immediately: Notify your employer as soon as possible after your work injury, ideally within 24-48 hours.

- Seek medical treatment: Get evaluated by a healthcare provider. Keep detailed records of all medical visits and treatments.

- File a formal claim: Your employer should provide you with the necessary forms. Each state has specific deadlines, so don't delay.

- Document everything: Keep records of medical bills, wage loss, and any correspondence with your employer or insurance company.

- Know your state's deadlines: States vary in how long you have to report an injury and file a claim, so check your state's specific requirements.

Next Steps

If you've been injured at work, take action immediately. Report your injury to your employer right away, seek medical treatment, and file your workers' compensation claim as soon as possible. Document everything—medical records, wage information, and communications with your employer and insurance company.

Understanding your state's specific benefit rates and regulations is essential. Visit your state's workers' compensation board or department of labor website for detailed information about maximum benefits, filing procedures, and deadlines. If you face issues with a denied or delayed claim, don't hesitate to seek legal assistance. Many workers' compensation attorneys work on a contingency basis, meaning you only pay if you win.

Workers' compensation exists to protect you when you're hurt on the job. By understanding your entitlements and taking prompt action, you can ensure you receive the financial support and medical care you deserve during your recovery.

Frequently Asked Questions

Sources & References

-

1

Workers' Compensation Laws by State | 2026 Legal Guide — royyanglaw.com

-

2

Workers' Compensation Benefit Rate Update for 2026 — mvplaw.com

-

3

The 4 Forces Driving Workers' Comp Claims in 2026 — www.rpsins.com

-

4

States Kick Off 2026 With Proposed Workers' Compensation Legislation — www.mymatrixx.com

-

5

Comp Renewals for 2026: Stability Persists, With Pockets of Pressure — www.businessinsurance.com

-

6

2026 Workers' Compensation Benefit Schedule — elc.ky.gov

Related Articles

How to Handle Medical Debt in the USA

Imagine opening your mailbox to find a hospital bill for $5,000 after what you thought was a routine visit. You're not alone—millions of Americans face this reality every year, with medical debt total...

Debt Consolidation Loans: How They Work and When to Use One

Struggling with multiple credit card bills piling up each month? You're not alone—millions of Americans face high-interest debt that feels impossible to tackle. A debt consolidation loan could be your...

What Is a Structured Settlement and Can You Sell It for Cash?

Imagine winning a hard-fought personal injury lawsuit only to face a tough choice: take a lump sum that could vanish quickly or opt for steady payments that last a lifetime. That's the world of struct...

What Is Bankruptcy Chapter 7 vs Chapter 13? A Plain-English Guide

Imagine staring at a pile of medical bills, credit card statements, and mortgage notices that keep you up at night. You're not alone—millions of Americans face overwhelming debt each year, and bankrup...