What Is Bankruptcy Chapter 7 vs Chapter 13? A Plain-English Guide

Imagine staring at a pile of medical bills, credit card statements, and mortgage notices that keep you up at night. You're not alone—millions of Americans face overwhelming debt each year, and bankrup...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine staring at a pile of medical bills, credit card statements, and mortgage notices that keep you up at night. You're not alone—millions of Americans face overwhelming debt each year, and bankruptcy under Chapters 7 or 13 offers a legal lifeline to regain control. This plain-English guide breaks down What Is Bankruptcy Chapter 7 vs Chapter 13?, helping you decide which path fits your situation in 2026.

Understanding Bankruptcy Basics

Bankruptcy is a federal legal process governed by the U.S. Bankruptcy Code that helps individuals and businesses eliminate or restructure debt when they can't pay. It provides an "automatic stay," immediately halting creditor collections, foreclosures, and lawsuits upon filing. For most Americans, Chapters 7 and 13 are the go-to options for personal debt relief—Chapter 7 for quick elimination, Chapter 13 for organized repayment.

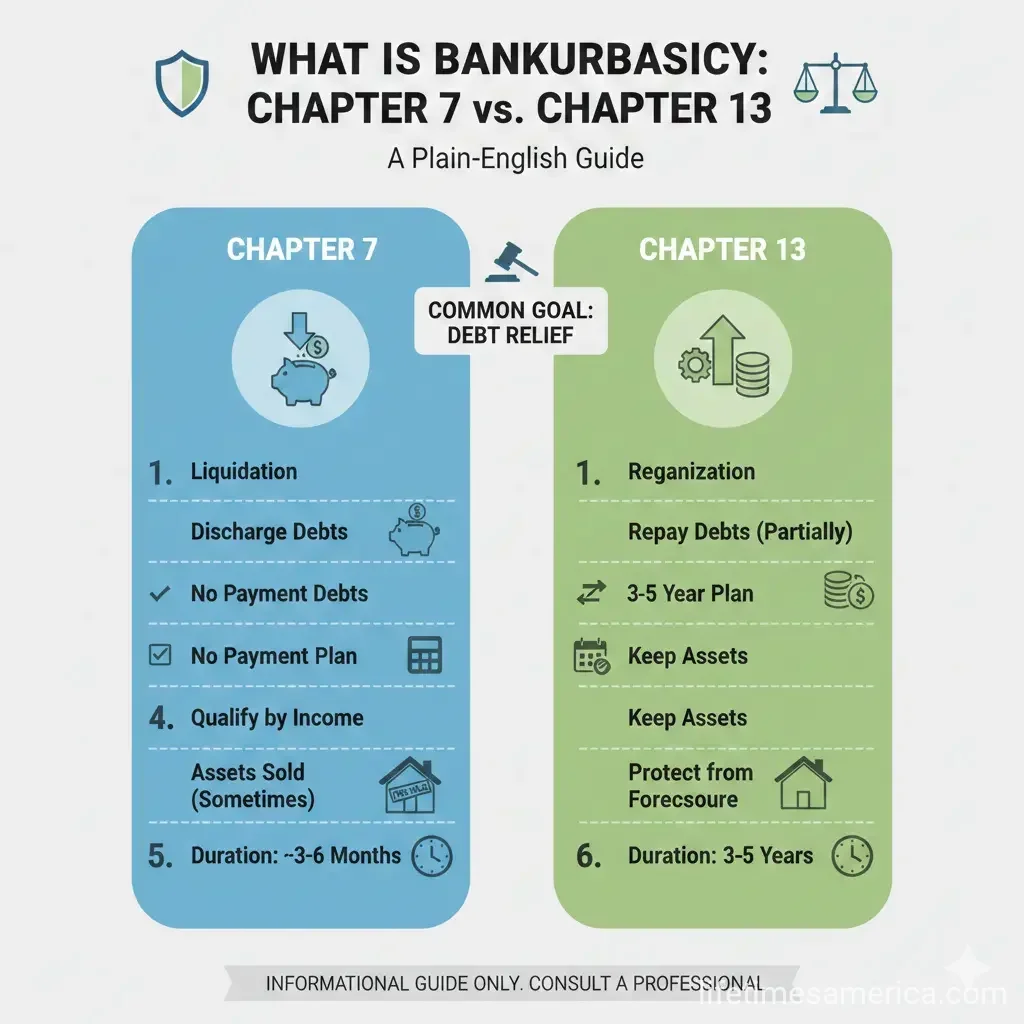

These chapters aren't one-size-fits-all. Chapter 7, often called "liquidation bankruptcy," sells non-exempt assets to pay creditors and discharges remaining eligible debts. Chapter 13, known as the "wage earner's plan," lets you keep your property while repaying debts over time through a court-approved plan.

Chapter 7 Bankruptcy: The Fast Track to a Fresh Start

Chapter 7 is ideal if you have low income, few assets, and mostly unsecured debts like credit cards or medical bills. It's quicker—typically wrapping up in 4-6 months—and discharges most eligible debts, giving you a clean slate.

How Chapter 7 Works

- Complete credit counseling from an approved agency.

- Prepare and file your petition with the bankruptcy court, including financial documents.

- Automatic stay stops collections.

- Attend the 341 meeting of creditors with a trustee.

- Trustee reviews and may sell non-exempt assets.

- Eligible debts are discharged, usually 60-90 days after the meeting.

Eligibility for Chapter 7

You must pass the means test: your income should be below your state's median or show no disposable income after expenses. No steady income is required, and there's no debt limit. In 2026, median incomes vary by state—for example, about $62,000 for a single person in many areas, adjusted annually by the U.S. Trustee Program.

Exemptions protect essentials like your home equity (up to state limits, e.g., $5,000-$7,500 in some states), car, and retirement accounts like 401(k)s. If assets exceed exemptions, they're sold.

Chapter 13 Bankruptcy: Keep Your Assets, Repay Over Time

Chapter 13 suits those with steady income who want to protect homes, cars, or other property. You propose a 3-5 year repayment plan based on disposable income, paying priority debts in full and others partially.

How Chapter 13 Works

- Complete credit counseling.

- File petition and proposed repayment plan.

- Automatic stay halts collections.

- Attend 341 meeting; court confirms plan.

- Make monthly payments to trustee, who distributes to creditors.

- After plan completion, remaining eligible debts discharge.

Eligibility for Chapter 13

Requires regular income and debts under limits: about $2.75 million combined secured/unsecured in 2026 (adjusted triennially). No means test, but your plan must be feasible.

It's great for catching up on mortgages or car loans—Chapter 13 lets you cure arrears while keeping the property.

Chapter 7 vs Chapter 13: Side-by-Side Comparison

Choosing between them boils down to your income, assets, and goals. Here's a clear breakdown:

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Process | Liquidation of non-exempt assets | Repayment plan (3-5 years) |

| Timeline | 4-6 months | 3-5 years |

| Income Requirement | Below median or pass means test | Steady income required |

| Asset Protection | Limited (exemptions only) | Keep all assets |

| Debt Limits | None | Secured/unsecured caps |

| Best For | Low income, few assets, unsecured debt | Homeowners, steady income, protect property |

| Credit Impact | 10 years on report | 7 years on report |

Pros and Cons of Each Chapter

Chapter 7 Pros and Cons

- Pros: Fast relief, wipes out most unsecured debts, lower attorney fees (around $1,500 average in 2026).

- Cons: Lose non-exempt assets, can't discharge some debts, 10-year credit hit.

Chapter 13 Pros and Cons

- Pros: Keep property, restructure secured debts, potential to discharge more debts like some divorce obligations.

- Cons: Longer commitment, higher costs (fees plus plan payments, averaging $3,000+), must stick to budget.

Which Debts Are Discharged?

Both chapters discharge unsecured debts like credit cards and medical bills. Non-dischargeable debts include student loans, recent taxes, child support, alimony, and DUI injuries. Chapter 13 may handle some non-dischargeable items better by paying them through the plan.

"Chapter 7 wipes out most unsecured debts in roughly four months, but... Chapter 13 lets you keep everything while committing to a three to five year repayment plan."

Real-Life Scenarios: Which Chapter Fits?

- Scenario 1: Single renter with $50,000 credit card debt, low income—Chapter 7 eliminates it quickly.

- Scenario 2: Homeowner behind on mortgage with steady job—Chapter 13 catches up payments, saves the house.

- Scenario 3: High earner failing means test but with car loan arrears—Chapter 13 restructures without losing the vehicle.

Costs, Credit Impact, and Long-Term Effects

Filing fees are $338 for Chapter 7 and $313 for Chapter 13 in 2026, plus attorney costs. Both hurt credit initially but allow rebuilding—many see scores rise within 1-2 years post-discharge. Chapter 7 stays 10 years, Chapter 13 seven years on reports.

Post-bankruptcy, focus on secured cards, budgeting, and 401(k) contributions for recovery.

Steps to Take Before Filing

- Review finances: List all debts, assets, income.

- Complete free credit counseling (required, available via justice.gov/ust).

- Consult a bankruptcy attorney—free initial consults common.

- Gather tax returns, pay stubs (6 months), bank statements.

- Check state exemptions via uscourts.gov.

Frequently Asked Questions

Related Articles

How to Handle Medical Debt in the USA

Imagine opening your mailbox to find a hospital bill for $5,000 after what you thought was a routine visit. You're not alone—millions of Americans face this reality every year, with medical debt total...

Debt Consolidation Loans: How They Work and When to Use One

Struggling with multiple credit card bills piling up each month? You're not alone—millions of Americans face high-interest debt that feels impossible to tackle. A debt consolidation loan could be your...

Workers Compensation Benefits: What You Are Financially Entitled To

If you've been injured at work, understanding your financial entitlements under workers' compensation can make a real difference in your recovery and financial stability. Workers' compensation benefit...

What Is a Structured Settlement and Can You Sell It for Cash?

Imagine winning a hard-fought personal injury lawsuit only to face a tough choice: take a lump sum that could vanish quickly or opt for steady payments that last a lifetime. That's the world of struct...