What Is a Structured Settlement and Can You Sell It for Cash?

Imagine winning a hard-fought personal injury lawsuit only to face a tough choice: take a lump sum that could vanish quickly or opt for steady payments that last a lifetime. That's the world of struct...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine winning a hard-fought personal injury lawsuit only to face a tough choice: take a lump sum that could vanish quickly or opt for steady payments that last a lifetime. That's the world of structured settlements, a smart financial tool designed for Americans dealing with injury claims.

If you're wondering what is a structured settlement and can you sell it for cash, you're not alone. Thousands of plaintiffs each year choose this option for its tax advantages and security, but life changes, and sometimes that steady stream needs to become immediate cash. This guide breaks it all down with practical advice tailored for U.S. readers, including state laws and real-world examples.

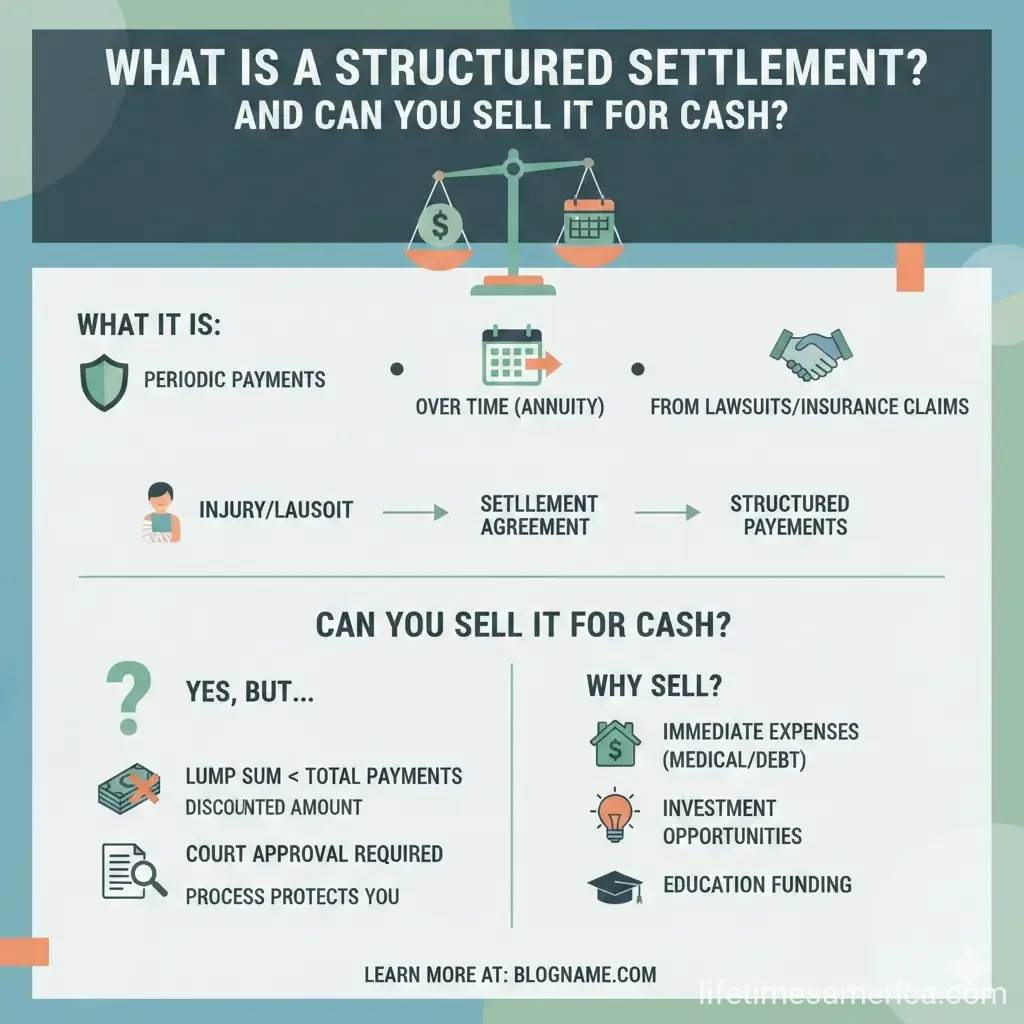

What Is a Structured Settlement?

A structured settlement is a legal agreement where a plaintiff receives compensation from a lawsuit through periodic payments over time, rather than a one-time lump sum. These payments are typically funded by an annuity purchased by the defendant or their insurer, providing guaranteed, tax-free income.

Congress has encouraged structured settlements since 1982 with favorable tax rules under sections like 104(a)(1), 104(a)(2), and 130 of the U.S. Tax Code, making all payments—principal and interest—100% exempt from federal and state income taxes for bodily injury cases. Today, they deliver about $10 billion annually to over 30,000 recipients nationwide.

How Structured Settlements Work

The process starts with a lawsuit settlement, often in personal injury, workers' compensation, medical malpractice, or wrongful death cases. Instead of handing over cash, the at-fault party (defendant) buys an annuity from a highly rated life insurance company. This annuity generates the scheduled payments directly to you, avoiding "constructive receipt" under IRS rules—meaning you don't owe taxes on money you never physically hold.

For example, a $500,000 car accident settlement might fund an annuity paying $3,000 monthly for 20 years, customized to your needs like college funds for kids or stepped-up payments for retirement. State insurance commissions regulate annuities, and structured settlement consultants help tailor the plan during negotiations.

Types of Structured Settlements

- Lifetime payments: Continue for life, ideal for catastrophic injuries.

- Period-certain: Fixed term, like 10-30 years.

- Deferred or stepped: Smaller now, increasing later for inflation or milestones.

- Lump sum plus periodic: Initial cash for immediate needs, then ongoing payments.

Benefits of a Structured Settlement

Structured settlements offer lifelong financial stability, especially for those unaccustomed to managing large sums. Key perks include:

- Tax-free growth: Unlike lump sums invested elsewhere, every dollar stays tax-free.

- Professional management: Life insurers handle payments, shielding funds from spendthrift risks.

- Customization: Match payments to life events, like Medicare gaps or disability costs.

- Security: Government-backed via highly rated insurers, preferred by judges and attorneys.

In 2026, with inflation hovering and Social Security adjustments lagging, these annuities provide predictable income immune to market swings.

Drawbacks of Structured Settlements

They're not perfect. Payments are fixed, so they may not keep pace with rising costs unless designed with increases. You can't easily access the full value upfront, and early death means heirs might lose future payments. Still, for most injury victims, benefits outweigh risks.

Can You Sell Your Structured Settlement for Cash?

Yes, you can sell your structured settlement for cash, but it's heavily regulated to protect you. Since the late 1990s, all 50 states have enacted Structured Settlement Protection Acts (SSPAs), spurred by the National Structured Settlements Trade Association (NSSTA). These laws require court approval for any transfer, ensuring it's in your best interest.

The Selling Process in 2026

- Contact a factoring company: These buyers offer lump sums at a discount (typically 9-18% off present value).

- Submit paperwork: Disclose your annuity details, financial needs, and why you need cash (e.g., debt, medical bills).

- Court hearing: A judge reviews independence from the buyer, fair terms, and your best interest—often within 30-60 days.

- Get paid: If approved, the factoring company becomes your payee.

For instance, selling $100,000 in future payments might net $70,000-$85,000 cash today, depending on rates and time left. Washington State's SSPA mandates three-day disclosures pre-agreement, including payment schedules and penalties. Check your state's attorney general site for specifics.

Pros and Cons of Selling

| Pros | Cons |

|---|---|

| Immediate cash for emergencies like home repairs or IRS debts. | Less total money due to discounts. |

| Flexibility for changing needs. | Lose tax-free status on sold portion. |

| Debt relief in tough economy. | Court fees and delays. |

Only sell if essential—NSSTA advises exhausting alternatives first.

Practical Tips for Americans Considering Structured Settlements or Sales

- Consult experts: Work with NSSTA-certified consultants and plaintiff attorneys early.

- Plan for taxes: Use IRS.gov tools to model lump sum vs. structured tax impacts.

- Check state laws: Visit usa.gov for SSPA details; e.g., California's requires financial counseling.

- Compare buyers: Get quotes from multiple factoring companies; avoid high discounts.

- Protect heirs: Add reversionary features for remaining payments.

In 2026, with 401(k) volatility, blending structured payments with Medicare supplements offers robust retirement planning.

Next Steps for Your Financial Future

Receiving a settlement? Discuss structured options with your attorney before signing. Need cash now? Shop factoring quotes and prepare for court. Resources like Annuity.org or your state bar association can guide you. Prioritize long-term security—your future self will thank you. Consult professionals to fit this to your unique situation.

Frequently Asked Questions

Sources & References

-

1

Structured Settlement: Understanding Its Legal Definition — legal-resources.uslegalforms.com

-

2

What are Structured Settlements? — nssta.com

-

3

Structured Settlements: Definition & Benefits (2026) — www.consumershield.com

-

4

What is a Structured Settlement? Understanding the Basics — ringlerassociates.com

-

5

Structured Settlements – What They Are and Why They Matter — www.genre.com

-

6

Everything You Should Know About Structured Settlements — www.walthew.com

-

7

What Is a Structured Settlement and How Does It Work? — www.annuity.org

-

8

Structured Settlement: A Comprehensive Guide 2026 — cameronlawlv.com

-

9

Structured Settlements - Individual — www.corebridgefinancial.com

Related Articles

How to Handle Medical Debt in the USA

Imagine opening your mailbox to find a hospital bill for $5,000 after what you thought was a routine visit. You're not alone—millions of Americans face this reality every year, with medical debt total...

Debt Consolidation Loans: How They Work and When to Use One

Struggling with multiple credit card bills piling up each month? You're not alone—millions of Americans face high-interest debt that feels impossible to tackle. A debt consolidation loan could be your...

Workers Compensation Benefits: What You Are Financially Entitled To

If you've been injured at work, understanding your financial entitlements under workers' compensation can make a real difference in your recovery and financial stability. Workers' compensation benefit...

What Is Bankruptcy Chapter 7 vs Chapter 13? A Plain-English Guide

Imagine staring at a pile of medical bills, credit card statements, and mortgage notices that keep you up at night. You're not alone—millions of Americans face overwhelming debt each year, and bankrup...