How to Handle Medical Debt in the USA

Imagine opening your mailbox to find a hospital bill for $5,000 after what you thought was a routine visit. You're not alone—millions of Americans face this reality every year, with medical debt total...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine opening your mailbox to find a hospital bill for $5,000 after what you thought was a routine visit. You're not alone—millions of Americans face this reality every year, with medical debt totaling at least $220 billion nationwide. In 2026, rising health care costs, potential cuts to Medicaid, and expiring enhanced ACA tax credits are making it even harder to stay afloat. This guide breaks down practical steps to tackle medical debt head-on, from negotiating bills to protecting your credit, so you can regain control of your finances.

Understanding Medical Debt in the USA

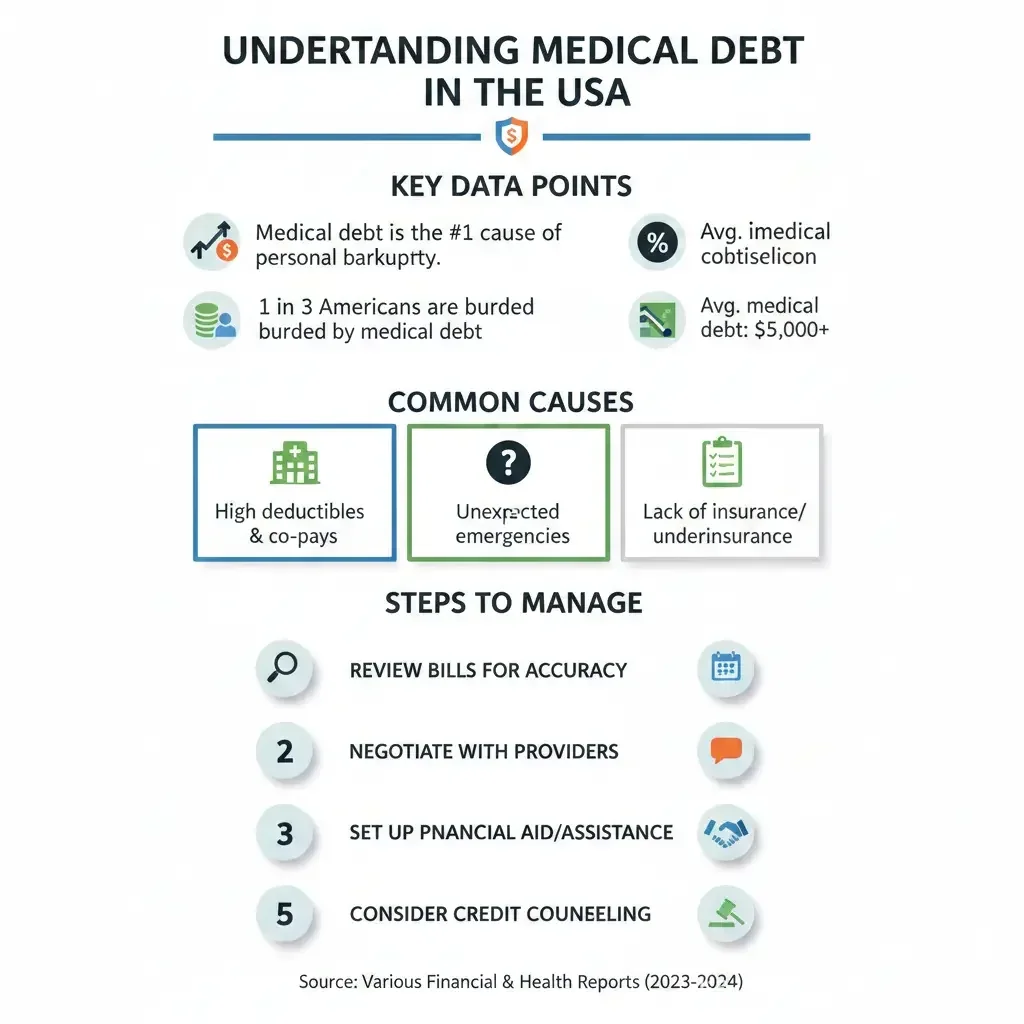

Medical debt hits hard and fast. About 20 million adults—nearly 1 in 12—owe medical bills, with most carrying over $1,000 and half owing more than $2,000. In total, Americans owe at least $220 billion, much of it from those with debts exceeding $10,000. Recent surveys show 41% of working-age adults (around 72 million people) have some form of medical debt, disproportionately affecting lower-income families, minorities, women, parents, and the uninsured.

Why is it so common? High deductibles, coinsurance, and surprise bills catch even insured patients off guard. For instance, many plans cover only 80% of costs, leaving you with 20% of a massive bill. In 2026, experts predict a surge due to higher employer plan costs and policy changes that could leave 15 million underinsured. Lower-income groups, like those earning $50,000–$75,000, often cite uncovered services and sky-high deductibles as top culprits.

Who Does Medical Debt Affect Most?

- Low-income households: They report the highest rates of debt from uncovered care.

- Uninsured or underinsured: Gaps in coverage lead to unaffordable out-of-pocket costs.

- People with chronic conditions or disabilities: Ongoing care racks up bills quickly.

- Black and Hispanic adults, women, and parents: These groups face debt at higher rates.

One in five adults has struggled to pay medical bills, with 63% dipping into savings to cover them. It doesn't stop there—medical debt often leads to collections calls, credit damage, and even housing instability.

Step-by-Step Guide: How to Handle Your Medical Debt

Don't panic. Systematic action can reduce or eliminate your burden. Start by gathering all bills, Explanation of Benefits (EOB) from your insurer, and payment records.

Step 1: Review and Dispute Errors

Errors happen—billing codes wrong, services not covered, or duplicate charges. Request itemized bills from providers; federal law under the No Surprises Act protects against many surprise bills. Compare with your EOB. If something's off, dispute in writing within 60–180 days, depending on your state.

- Check for out-of-network charges without consent.

- Verify insurance applied correctly—call your insurer if not.

- Common fix: 59% of debts are under $500 and often negotiable or erroneous.

Step 2: Negotiate with Providers

Hospitals and doctors often reduce bills for cash payments or financial hardship. Ask for a discount—many write off 20–50% upfront. Set up interest-free payment plans; No Surprises Act limits collections on surprise bills.

"Patients should always negotiate. Providers prefer partial payment over nothing."

Pro tip: Contact the hospital's billing department or patient advocate. Nonprofits like the Patient Advocate Foundation offer free help (patientadvocate.org).

Step 3: Explore Financial Assistance Programs

Most hospitals must screen for charity care under the ACA. Apply even if insured—programs like Hill-Burton (for certain facilities) forgive debts for low-income patients. In 2026, states are stepping up: some ban medical debt on credit reports, and others forgive debts via programs.

- Check hospital charity care policy (required screening for incomes <400% federal poverty level).

- Use Dollar For (dollarfor.org) to find aid.

- State resources: Visit healthcare.gov for Medicaid expansion status.

Step 4: Manage Payments Without Ruining Credit

Good news: As of 2025–2026, CFPB rules prohibit medical debt under $500 on credit reports, with full bans in final stages despite challenges. Pay what you can to avoid collections. Options include:

- Payment plans: 11% of debtors use long-term plans.

- Credit cards: Only for small amounts—17% have card debt from bills.

- Loans from family: 10% borrow from loved ones. Avoid payday loans—they destroyed one patient's credit.

If debt spirals, consider nonprofit credit counseling via NFCC.org, not for-profit debt settlement.

Step 5: Prevent Future Debt

Shop plans during Open Enrollment (Nov 1–Jan 15). Choose high-deductible plans only if you have an HSA. Price transparency rules (effective 2026) let you compare costs upfront via hospital websites.

Frequently Asked Questions

Sources & References

-

1

[2] — insights.bu.edu

-

2

[2] — insights.bu.edu

-

3

[3] — www.ilr.cornell.edu

-

4

The Burden of Medical Debt in the United States — www.healthsystemtracker.org

-

5

The Debt Set To Rise For Americans In 2026 — insights.bu.edu

-

6

Healthcare Insights: How Medical Debt Is Crushing 100 Million Americans — www.ilr.cornell.edu

-

7

Addressing Medical Debt - ABIM Foundation — abimfoundation.org

-

8

Kansas Survey Respondents Receive Unexpected Medical Bills — healthcarevaluehub.org

-

9

Americans' Challenges with Health Care Costs | KFF — www.kff.org

- 10

-

11

States Move to the Front Lines to Alleviate Medical Debt — www.commonwealthfund.org

-

12

Medical Debt Associated With Subsequent Difficulty Paying Rent or Mortgage — publichealth.jhu.edu

Related Articles

Debt Consolidation Loans: How They Work and When to Use One

Struggling with multiple credit card bills piling up each month? You're not alone—millions of Americans face high-interest debt that feels impossible to tackle. A debt consolidation loan could be your...

Workers Compensation Benefits: What You Are Financially Entitled To

If you've been injured at work, understanding your financial entitlements under workers' compensation can make a real difference in your recovery and financial stability. Workers' compensation benefit...

What Is a Structured Settlement and Can You Sell It for Cash?

Imagine winning a hard-fought personal injury lawsuit only to face a tough choice: take a lump sum that could vanish quickly or opt for steady payments that last a lifetime. That's the world of struct...

What Is Bankruptcy Chapter 7 vs Chapter 13? A Plain-English Guide

Imagine staring at a pile of medical bills, credit card statements, and mortgage notices that keep you up at night. You're not alone—millions of Americans face overwhelming debt each year, and bankrup...