What Is a Personal Loan and When Should You Get One?

Imagine you're facing a hefty medical bill after an unexpected ER visit, or you want to consolidate those high-interest credit cards dragging down your budget. A personal loan could be the flexible fi...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine you're facing a hefty medical bill after an unexpected ER visit, or you want to consolidate those high-interest credit cards dragging down your budget. A personal loan could be the flexible financial lifeline you need, but knowing when to grab one—and when to steer clear—is key to avoiding costly mistakes.

In this guide, we'll break down everything Americans need to know about personal loans in 2026, from how they work to smart times to use them. Whether you're eyeing debt relief or a home upgrade, you'll get practical tips tailored to U.S. lenders, rates, and regulations.

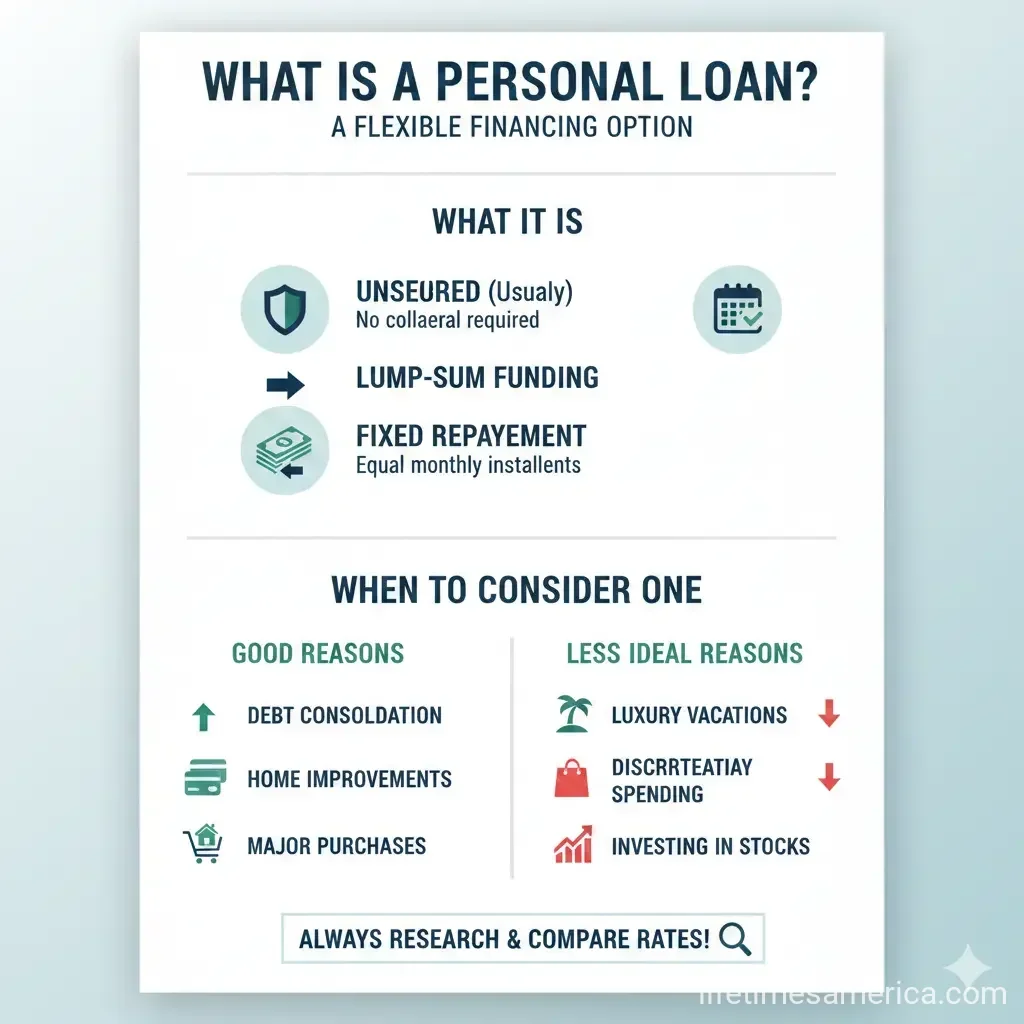

What Is a Personal Loan?

A personal loan is an installment loan where you borrow a lump sum from a bank, credit union, or online lender and repay it in fixed monthly payments over a set term, typically with a fixed interest rate. Unlike revolving credit like credit cards, you get the full amount upfront and make predictable payments that include principal and interest.

Most personal loans are unsecured, meaning no collateral like your car or home is required—just a solid credit score and income proof. Loan amounts range from $600 to $100,000, with terms from 12 to 84 months, depending on the lender. For example, Wells Fargo offers up to $100,000 with APRs from 6.74% to 25.99% as of early 2026.

Key Features of Personal Loans

- Fixed payments: Budget-friendly monthly installments that don't fluctuate.

- Versatile use: Funds for debt consolidation, medical bills, home improvements, or big purchases—no restrictions on most unsecured loans.

- Fees to watch: Origination fees (1%-8% of loan amount) and possible late payment charges can add up.

- Approval factors: Credit score (ideally 670+), debt-to-income ratio under 36%, and stable income.

Types of Personal Loans

Personal loans aren't one-size-fits-all. Here's a rundown of the main types available to U.S. borrowers in 2026.

Unsecured Personal Loans

The most common type, these don't require collateral and rely on your creditworthiness. They're ideal for good-credit borrowers but come with higher APRs (often 6%-36%). PenFed Credit Union, for instance, offers $600-$50,000 unsecured loans.

Secured Personal Loans

Backed by collateral like savings or a vehicle, these offer lower rates but risk losing your asset if you default. They're easier to qualify for with fair credit.

Debt Consolidation Loans

Combine multiple high-interest debts (like credit cards at 20%+ APR) into one lower-rate loan. If your new rate is 10%, you could save hundreds monthly—but watch origination fees.

Other Variations

- Variable-rate loans: Rare; rates tied to market indexes, with possible caps.

- Personal line of credit (PLOC): Revolving like a credit card—borrow as needed, pay interest only on what you use, but no grace period.

- Cosigned or joint loans: Add a creditworthy co-borrower to boost approval odds.

How Do Personal Loans Work?

Getting a personal loan is straightforward. Lenders like Citi or online platforms review your credit report, income (via pay stubs or tax returns), and debt load. If approved, you get funds in 1-7 days via direct deposit.

Your monthly payment covers principal plus interest. For a $10,000 loan at 10% APR over 36 months, expect about $332/month. Use free calculators on lender sites to precompute. Pre-approvals (soft credit checks) let you shop rates without dinging your score.

2026 Rates and Terms

Average unsecured personal loan APRs hover at 11.5%-12.5% for excellent credit, per recent data, but can hit 36% for subprime borrowers. Terms up to 84 months (7 years) are common at big banks like Wells Fargo.

When Should You Get a Personal Loan?

Personal loans shine for one-time, planned expenses where fixed payments beat variable credit card interest. Here's when they're a smart move for Americans.

Top 5 Reasons to Get One

- Debt consolidation: Roll credit card debt (avg. 21% APR) into a 9% loan to save $1,000+ yearly on a $20,000 balance.

- Emergency medical bills: Cover out-of-pocket costs not hit by Medicare or insurance gaps.

- Home improvements: Fund repairs without tapping home equity (riskier in volatile markets).

- Major purchases: New appliances or wedding costs, if you can repay in 2-3 years.

- Relocation or moving: Bridge gaps when job hunting across states.

Red Flags: When to Avoid Personal Loans

- Can't afford payments: Ensure it fits your budget (use 50/30/20 rule: 50% needs, 30% wants, 20% savings/debt).

- Short-term needs: Use credit cards or 0% intro APR cards instead.

- Poor credit without cosigner: Rates skyrocket above 25%.

- No clear repayment plan: Avoid if it means more debt.

Pros and Cons of Personal Loans

| Pros | Cons |

|---|---|

| Fixed rates and payments for budgeting | Origination fees increase costs (1-8%) |

| No collateral risk on unsecured loans | Hard inquiries may lower credit score temporarily |

| Build credit with on-time payments | High APRs for bad credit (up to 36%) |

| Fast funding (1-7 days) | Prepayment penalties on some loans |

How to Get a Personal Loan in the U.S. in 2026

Shop smart: Compare at least three lenders. Check credit unions like PenFed for lower rates, or banks like PNC and Citi for quick apps.

Step-by-Step Guide

- Check credit: Free weekly reports at AnnualCreditReport.com (mandated by FACTA).

- Pre-qualify: Soft pulls at sites like Bankrate or Fortune's top lists.

- Gather docs: ID, income proof, bank statements.

- Apply: Online in minutes; American Express offers preapprovals to cardholders.

- Review terms: Avoid high fees; negotiate if possible.

- Repay on time: Set autopay for discounts (0.25%-0.50% off APR at many lenders).

Pro tip: Federal law (Truth in Lending Act) requires clear APR disclosures—always verify.

Personal Loan Alternatives

Not sold? Consider 0% APR credit cards (12-21 months intro), home equity lines (lower rates but home risk), or 401(k) loans (no credit check, but job-loss risks repayment).

Next Steps for Smarter Borrowing

Ready to apply? Pull your free credit report today, compare rates at three lenders, and calculate payments with online tools. Avoid impulse borrowing—project cash flow for the full term. With discipline, a personal loan can boost your financial health, not hinder it. Start prequalifying now to find your best 2026 rate.

Frequently Asked Questions

Sources & References

-

1

8 types of personal loans and their uses — plus 5 to avoid - Bankrate — www.bankrate.com

- 2

-

3

What is A Personal Loan? | PNC Insights — www.pnc.com

-

4

Types of Personal Loans (2026) | ConsumerAffairs® — www.consumeraffairs.com

-

5

What Is a Personal Loan and How Does It Work? - NCOA — www.ncoa.org

- 6

-

7

What is a Personal Loan? - Citi.com — www.citi.com

Useful Tools

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...