FHA Loan Requirements: How to Buy a Home with 3.5% Down

Imagine owning your dream home in 2026 without draining your savings on a massive down payment. With an FHA loan, you can buy a house with just 3.5% down if you meet the key requirements—making homeow...

Imagine owning your dream home in 2026 without draining your savings on a massive down payment. With an FHA loan, you can buy a house with just 3.5% down if you meet the key requirements—making homeownership accessible for first-time buyers and those rebuilding credit across America.

FHA loans, insured by the Federal Housing Administration (FHA) under the U.S. Department of Housing and Urban Development (HUD), help millions step into the housing market each year. They're especially popular in today's market, where median home prices hover around $400,000 in many areas. This guide breaks down the exact FHA loan requirements for 2026, how to qualify for that low 3.5% down payment, and actionable steps to get approved. Whether you're in a low-cost county or a high-cost city like Los Angeles, we'll cover everything you need to know.[1][2]

What Is an FHA Loan and Who Qualifies?

FHA loans stand out for their flexible standards compared to conventional mortgages. Backed by the government, they reduce risk for lenders, allowing lower credit scores and smaller down payments. In 2026, they're ideal for first-time homebuyers, single parents, displaced homemakers, or anyone who hasn't owned a home in the last three years.[2]

Key Benefits of FHA Loans in 2026

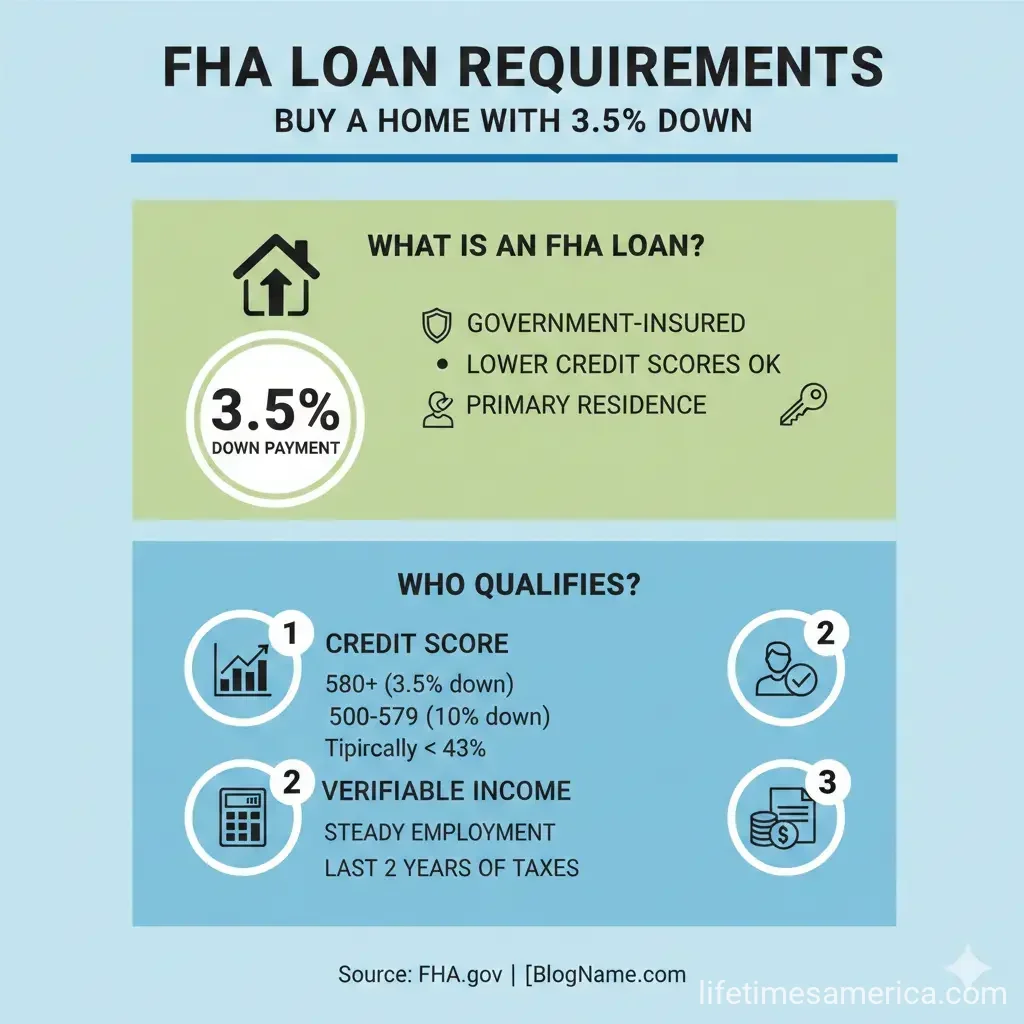

- Low down payment: Just 3.5% with a FICO score of 580 or higher—far below the 20% often required for conventional loans.[1][2][4]

- Flexible credit: Minimum score as low as 500, though with a higher down payment.[3][5]

- Government backing: Easier approval if your finances aren't perfect.[6]

- Loan limits up to $1,249,125: In high-cost areas, covering pricier markets.[7][8][9]

These perks make FHA loans a smart choice amid rising interest rates and home prices. But approval isn't automatic—you must meet specific criteria.[1]

Credit Score Requirements for 3.5% Down

The cornerstone of qualifying for a 3.5% down payment is your credit score. Lenders use your FICO score to assess risk.

Minimum FICO Scores

- 580 or higher: Eligible for 3.5% down payment. This is the threshold for the lowest down payment option.[1][2][4][5][6]

- 500-579: Still qualify, but need 10% down. Boost your score first if possible—pay down debt or correct errors via AnnualCreditReport.com.[1][2][3]

- Below 500: Generally ineligible, though some lenders offer exceptions for streamline refinances.[4]

Established credit history matters too. Even without a perfect score, on-time payments on credit cards, car loans, or student debt can help. Avoid recent delinquencies, like federal tax debts or prior FHA defaults.[3]

"FHA loan applicants must have a minimum FICO score of 580 to qualify for the low down payment advantage, which is currently at 3.5%."[2]

Down Payment Details: Achieving 3.5%

That 3.5% down payment can mean tens of thousands saved. For a $400,000 home, it's just $14,000—often covered by gifts from family, seller concessions, or grants like those from HUD's Good Neighbor Next Door program.

How to Calculate Your Down Payment

- Check your FICO score via free weekly reports at AnnualCreditReport.com.

- Multiply home price by 0.035 (for 580+ score) or 0.10 (500-579).

- Factor in closing costs (2-5% of loan amount), which can be rolled into the loan or paid upfront.[4]

Gift funds are allowed from relatives, but document the source. FHA doesn't require your own cash reserves beyond the down payment.[2]

Debt-to-Income (DTI) Ratio Guidelines

Your DTI ratio shows lenders if you can handle payments. It's monthly debts divided by gross monthly income.

FHA DTI Limits in 2026

- Front-end DTI: Housing costs ≤ 31% of income.

- Back-end DTI: All debts ≤ 43% ideally, up to 57% with strong compensating factors like cash reserves.[1][3][4][7]

Example: Earning $6,000/month gross with $2,000 in debts? Max housing payment around $1,860 (31%). Use online calculators from HUD.gov to check yours.[3]

Income and Employment Verification

Steady income is crucial. Lenders verify two years of employment history via pay stubs, W-2s, and tax returns.

What Counts as Steady Income?

- W-2 wages, self-employment (two years tax returns), Social Security, or pensions.[3][5][7]

- No gaps longer than 30 days without explanation (e.g., schooling).[7]

- Sufficient residual income post-payment for living expenses.[6]

First-time buyers: Part-time or gig work qualifies if documented. Provide Social Security number and bank statements.[3]

Property Requirements and FHA Appraisals

The home must pass an FHA appraisal for safety, security, and soundness—no major repairs needed post-appraisal.

Eligible Properties

- Single-family homes, condos (FHA-approved), townhomes, or 2-4 unit properties (you occupy one unit).[5][6]

- Primary residence only: Move in within 60 days of closing. No investment properties.[4][5]

- Loan limits: $541,287 floor in low-cost areas; $1,249,125 ceiling in high-cost (e.g., San Francisco).[6][7][8][9]

Check county limits at HUD.gov. Multi-unit? Rent others to offset payments.[5]

Mortgage Insurance Premium (MIP)

All FHA loans require MIP to protect lenders.

- Upfront MIP: 1.75% of loan, financed into mortgage.[6]

- Annual MIP: 0.15%-0.75% monthly, for 11 years (or loan life if down payment <10%).[4][6]

Budget extra $100-200/month. Refinance to conventional after building equity to drop MIP.[5]

Steps to Apply for an FHA Loan in 2026

- Get pre-approved: Shop FHA-approved lenders via HUD's lender list at HUD.gov.

- Find a home: Work with a real estate agent experienced in FHA buys.

- Submit docs: Pay stubs, tax returns, bank statements, ID.

- Appraisal and underwriting: 30-45 days typical closing.

- Close: Sign at title company; funds via wire or cashier's check.

Pro tip: Use FHA's 203(k) loan for fixer-uppers, combining purchase and rehab costs.[5]

FAQ: Common FHA Loan Questions

What credit score do I need for an FHA loan?

A minimum of 580 for 3.5% down; 500-579 requires 10% down.[1][2][6]

Can I use gift money for the down payment?

Yes, from family or approved sources, with a gift letter.[2]

What's the maximum FHA loan amount in 2026?

$541,287 in low-cost areas; up to $1,249,125 in high-cost.[7][8][9]

Do I need a 2-year work history?

Typically yes, but recent grads or career changers can qualify with documentation.[7]

Can I remove FHA MIP?

After 11 years if refinancing or meeting conditions; otherwise, it stays.[4]

Are FHA loans only for first-time buyers?

No, but first-timers and repeat buyers with credit challenges qualify easily.[2]

Ready to Buy? Your Next Steps

Start by pulling your credit report and calculating DTI today. Contact an FHA-approved lender—many offer free consultations. Explore local down payment assistance via HUD.gov or state housing agencies. With 3.5% down, 2026 could be your year to join America's 65 million homeowners. Act now before rates shift.

Sources & References

- NEW FHA Loan Requirements 2026 - First Time Home Buyer — youtube.com

- FHA Loan Requirements in 2026 — fha.com

- FHA Loan Requirements 2026 - Freedom Mortgage — freedommortgage.com

- FHA loan limits: How much can you borrow in 2026? — rocketmortgage.com

- FHA Loan Requirements Checklist 2026 - CrossCountry Mortgage — crosscountrymortgage.com

- FHA Loan Requirements for 2026 - Compass Mortgage — compmort.com

- 2026 FHA Loan Limits - Rate — rate.com

- HUD's Federal Housing Administration Announces 2026 Loan Limits — hud.gov

- FHFA Announces Conforming Loan Limit Values for 2026 — fhfa.gov

Useful Tools

Related Articles

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...

What Is PMI (Private Mortgage Insurance) and How Do You Avoid It?

Buying your first home is exciting, but those extra mortgage costs can quickly dampen the thrill. If you've heard whispers about Private Mortgage Insurance (PMI) sneaking into your monthly payments, y...

What Is a Reverse Mortgage and Who Should Consider It?

If you're 62 or older and looking for ways to tap into your home's value without selling it, a reverse mortgage might be worth exploring. Unlike traditional mortgages where you make monthly payments,...

What Is a Mortgage and How Does It Work?

Imagine standing in front of your dream home, keys in hand, but without enough cash to buy it outright. That's where a mortgage steps in—a powerful financial tool that makes homeownership possible for...