What Is Health Insurance and How Does It Work in the USA?

Imagine facing a sudden medical emergency without the safety net of health insurance—bills piling up, treatments delayed, and financial stress mounting. In the USA, health insurance is your shield aga...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine facing a sudden medical emergency without the safety net of health insurance—bills piling up, treatments delayed, and financial stress mounting. In the USA, health insurance is your shield against these scenarios, covering everything from routine checkups to major surgeries. Understanding what health insurance is and how it works in the USA empowers you to make smart choices for 2026 coverage.

Defining Health Insurance in the United States

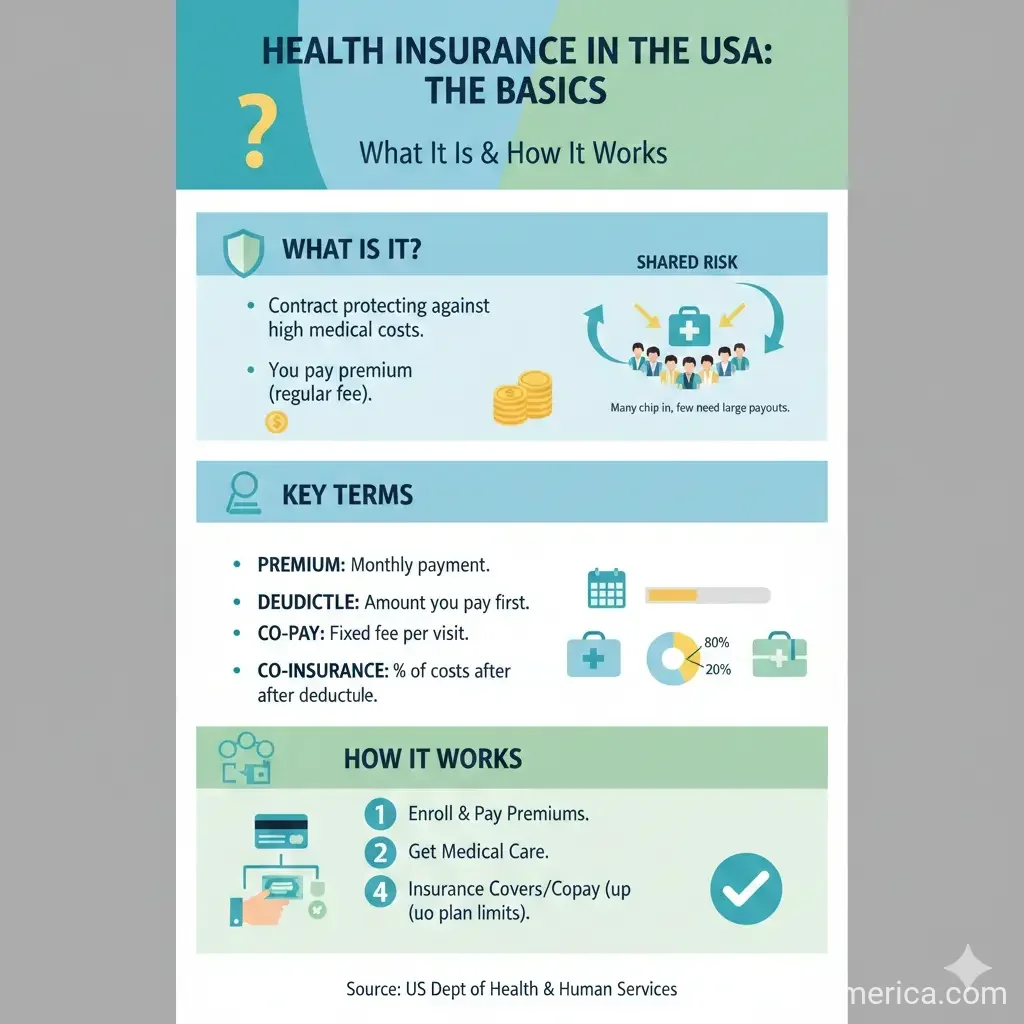

Health insurance is a contract between you and an insurance company or government program that pays for your medical expenses in exchange for regular premiums. It protects against high healthcare costs, which average over $13,000 per person annually in the US. Unlike other countries with universal systems, the USA relies on a mix of private plans, employer-sponsored coverage, and public programs like Medicare and Medicaid.

At its core, health insurance covers **essential health benefits** mandated by the Affordable Care Act (ACA), including hospitalization, prescription drugs, maternity care, and preventive services. Plans fall into categories like Bronze, Silver, Gold, and Platinum on the Marketplace, with higher metal levels offering more coverage but higher premiums.

Key Terms You Need to Know

- Premium: Monthly payment to keep your plan active, regardless of claims.

- Deductible: Amount you pay out-of-pocket before insurance kicks in (e.g., $1,500–$8,000 for High Deductible Health Plans or HDHPs).

- Copayment (Copay): Fixed fee for services, like $30 for a doctor's visit.

- Coinsurance: Your share of costs after deductible, often 20%.

- Out-of-Pocket Maximum: Cap on your annual spending, after which insurance covers 100%.

How Health Insurance Works: The Step-by-Step Process

Getting and using health insurance involves enrollment, paying premiums, meeting your deductible, and filing claims. Here's how it flows in practice:

- Enroll in a Plan: Choose during Open Enrollment (November 1, 2025–January 15, 2026 for Marketplace plans) or after a qualifying life event like job loss.

- Pay Premiums: Automatically deducted or billed monthly. Employers often cover 50–80% for job-based plans.

- Access Care: Visit in-network providers to minimize costs. Preventive services are often free.

- Pay Your Share: Cover deductibles, copays, and coinsurance until out-of-pocket max.

- Claims Processing: Providers bill insurance directly; you get Explanation of Benefits (EOB) statements.

For 2026, expect average Marketplace premiums after tax credits at $50/month for the lowest-cost plan—a $13 increase from 2025, but still affordable for many. Nearly 60% of re-enrollees can find plans at or below $50 after credits.

Main Types of Health Insurance in the USA

1. Marketplace Plans (ACA/Obamacare)

Shop at HealthCare.gov or state exchanges for individual/family coverage. Eligible Americans get premium tax credits based on income (100–400% of federal poverty level). In 2026, enhanced credits expire end of 2025, potentially raising costs for some, with CBO projecting 14 million more uninsured by 2034 if not extended. Bronze and Catastrophic plans are now HSA-eligible nationwide, expanding access to 1.6 million more consumers.

2. Employer-Sponsored Insurance

The most common type, covering 150+ million Americans. Employers offer during open enrollment; you may qualify mid-year after events like marriage. Premiums average $8,435 for single coverage, with employers paying most.

3. Medicare

Federal program for those 65+ or with disabilities. Parts A (hospital), B (outpatient), D (drugs), and optional Medigap or Medicare Advantage. Enrollment via Social Security; 2026 changes may affect Marketplace interactions.

4. Medicaid and CHIP

Free/low-cost for low-income families, pregnant women, children. Eligibility expanded under ACA; states administer with federal funds. CHIP covers kids in higher-income families ineligible for Medicaid.

5. Short-Term Limited Duration Insurance (STLDI)

For temporary gaps (e.g., job transitions). 2024 rules limit initial terms to 3 months, total to 4 months. Excepted from ACA rules like pre-existing condition protections.

6. Health Savings Accounts (HSAs)

Pair with HDHPs. Contribute pre-tax up to annual limits (rolls over, earns interest). New in 2026: All Bronze/Catastrophic plans qualify, covering deductibles/copays.

2026 Updates: What’s Changing for Health Insurance

Open Enrollment: November 1, 2025–January 15, 2026. Key shifts include:

- Expanded HSA eligibility to every county on HealthCare.gov.

- Potential premium hikes post-ACA credit expiration; review plans carefully.

- Shortened Marketplace enrollment windows and no auto-reenrollment under recent laws.

- Immigrant eligibility tweaks: No credits for some low-income noncitizens.

Compare options at HealthCare.gov or your employer's portal. Federal changes from the "Big, Beautiful Bill" (OBBBA) could reduce coverage for millions by 2034.

Practical Tips for Choosing and Using Your Plan

- Assess Needs: Healthy? Opt for Bronze/HDHP with HSA. Chronic conditions? Gold/Platinum.

- Check Networks: Ensure doctors/hospitals are in-network to avoid full bills.

- Maximize Savings: Apply for credits at HealthCare.gov; contribute to HSA.

- Appeal Denials: If claims rejected, request internal/external reviews.

- Stay Enrolled: Missing premiums cancels coverage; set autopay.

For federal employees, compare 2026 FEHB plans via OPM.gov. Use NAIC tools for state-specific advice.

Next Steps to Secure Your 2026 Coverage

Don't wait—mark your calendar for November 1, 2025. Visit HealthCare.gov to preview plans, estimate subsidies, and compare. Talk to your employer HR about job-based options. If low-income, check Medicaid eligibility at your state site or usa.gov. Consulting a licensed broker (find via NAIC) ensures personalized advice. With proactive steps, you'll navigate what health insurance is and how it works in the USA confidently, safeguarding your health and finances.

Frequently Asked Questions

Sources & References

-

1

Federal Government Poised to Amend Definition of Short-Term Limited Duration Insurance — www.mitchellwilliamslaw.com

-

2

New in 2026: More plans now work with Health Savings Accounts — www.healthcare.gov

-

3

What Are My Health Plan Options for 2026? - NAIC — content.naic.org

-

4

4 “Big, Beautiful Bill” changes that will reshape care in 2026 — www.ama-assn.org

- 5

-

6

Individual Health Plans for 2026: What You Need to Know — www.swiftkennedy.com

-

7

Tips about the Health Insurance Marketplace® | HealthCare.gov — www.healthcare.gov

-

8

ACA Marketplace Financial Help Changes for 2026 Coverage — www.anthem.com

-

9

Healthcare: Compare 2026 Plans - OPM.gov — www.opm.gov

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...