How to Pay Off Your Mortgage Faster

Imagine waking up each morning knowing your home is truly yours—no more monthly mortgage payments weighing on your budget. In 2026, with home values steady and interest rates stabilizing around 6-7% f...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine waking up each morning knowing your home is truly yours—no more monthly mortgage payments weighing on your budget. In 2026, with home values steady and interest rates stabilizing around 6-7% for many loans, paying off your mortgage faster isn't just a dream; it's a practical goal that can save you tens of thousands in interest and free up cash for retirement or family goals.

Whether you're tackling a 30-year conventional loan or refinancing into something shorter, these proven strategies can shave years off your payoff timeline. We'll break down actionable steps tailored for American homeowners, including tips from financial experts like Dave Ramsey and real-world examples using current rates.

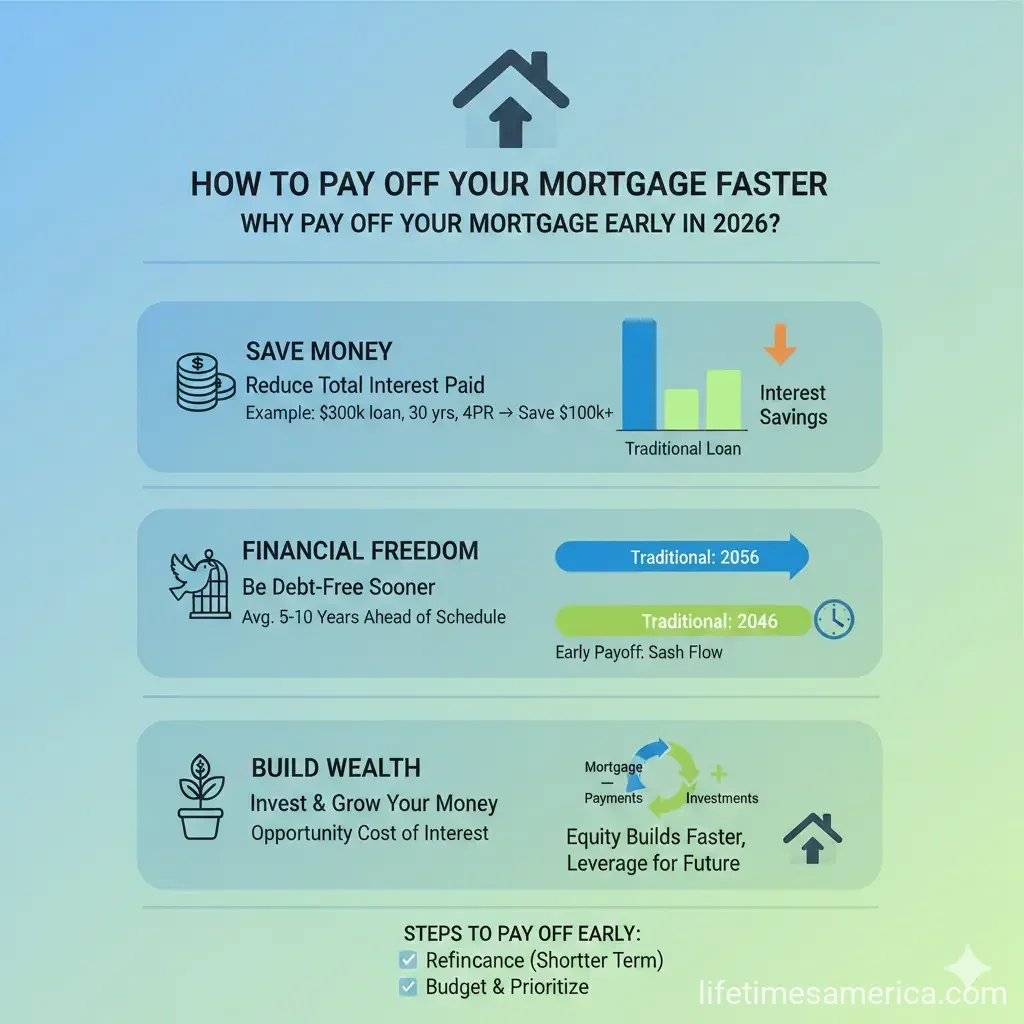

Why Pay Off Your Mortgage Early in 2026?

Owning your home outright provides financial freedom, especially as you approach retirement age. According to recent trends, more Americans are prioritizing mortgage payoff amid economic shifts, aiming for debt-free living. You'll save significantly on interest—for a $220,000, 30-year mortgage at 4% interest, standard payments total over $360,000 including interest, but aggressive strategies can cut that dramatically.

Plus, reaching 80% of your home's original value lets you drop private mortgage insurance (PMI), which costs 0.5-1% of your loan annually on conventional loans with less than 20% down. No prepayment penalties on most U.S. mortgages mean you can prepay freely—check your closing disclosure or ask your servicer to confirm.

Strategy 1: Refinance to a Shorter-Term Mortgage

Switching from a 30-year to a 15-year fixed-rate mortgage halves your payoff time and slashes interest costs. In 2026, 15-year rates hover around 5.5-6.5%, lower than 30-year options, making monthly payments higher but total interest far less.

Example: On a $300,000 loan, a 30-year at 6.5% means $1,896 monthly and $382,000 in interest. Refinance to 15-year at 5.75%? Payments jump to $2,500, but interest drops to $150,000, saving over $230,000.

Is Refinancing Right for You?

- Shop lenders via the Consumer Financial Protection Bureau's rate comparison tools at consumerfinance.gov.

- Break-even point: Divide closing costs (2-5% of loan) by monthly savings. If under 2-3 years, it's worth it.

- Consider adjustable-rate mortgages (ARMs) for initial lower rates, but watch for adjustments after 5-7 years.

Strategy 2: Make Extra Principal Payments

The simplest way to accelerate payoff: Direct extra cash straight to principal. Always specify "apply to principal only" in writing to your servicer—otherwise, it might go to interest or future payments.

Biweekly Payments

Pay half your monthly amount every two weeks, creating 26 half-payments (13 full ones) yearly. For a $1,200 monthly mortgage, this adds one free payment annually, potentially cutting 5-8 years off a 30-year loan.

1/12th Extra Each Month

Add 1/12 of your monthly payment ($75 on a $900 payment) to hit an extra full payment yearly without a big hit. On a $900 payment, pay $975 monthly to mimic this.

Rounding Up or Gradual Increases

Round up to the nearest $50 or $100—$1,200 becomes $1,250. Or use the "dollar-a-month" plan: Increase by $1 monthly ($900, then $901, etc.). On a $150,000 loan at 6%, this shaves 8 years.

Pro Tip: Automate via your bank's online portal for consistency.

Strategy 3: Leverage Windfalls and Bonuses

Tax refunds, holiday bonuses, or inheritance? Send them to principal. The average U.S. tax refund in 2026 is around $3,000—apply it to knock years off.

Even credit card rewards or side hustle cash count. Aim to build an emergency fund first (3-6 months' expenses in a high-yield savings account) before aggressive prepayments, as your home isn't liquid.

Strategy 4: Avoid PMI from the Start or Drop It Early

Put 20% down on conventional loans to skip PMI entirely—saving 0.5-1% yearly ($100-200/month on $200,000 loans). If you already have it, extra payments toward 80% loan-to-value trigger automatic cancellation under the Homeowners Protection Act.

Request removal manually once you hit 80% with proof like a new appraisal.

Strategy 5: Budget Ruthlessly and Prioritize Debt

Free up cash by tackling high-interest debt first using the debt avalanche (highest rate) or snowball (smallest balance) methods. Follow the 50/30/20 rule: 50% needs, 30% wants, 20% savings/debt.

Apps like Mint or YNAB track spending; automate transfers to mortgage post-budgeting.

Sample Budget Adjustment

| Category | Monthly Allocation | Extra to Mortgage |

|---|---|---|

| Dining Out | Cut $200 | $200 |

| Subscriptions | Cancel 2 ($50) | $50 |

| Windfalls | 100% apply | $500 avg |

| Total Extra | - | $750 |

Potential Savings: Real 2026 Examples

For a $250,000 mortgage at 6.5%:

- Standard 30-year: 30 years, $280,000 interest.

- Biweekly: 25 years, $220,000 interest (save $60,000).

- 15-year refinance + extras: 12 years, $120,000 interest (save $160,000).

Run your numbers with free calculators at consumerfinance.gov.

Common Pitfalls to Avoid

- Illiquid funds: Keep stocks, bonds, or a HELOC accessible.

- Prepayment penalties: Rare but check your note.

- Opportunity cost: If investments yield > mortgage rate (e.g., S&P 500 avg 10%), weigh investing vs. payoff.

Take Control of Your Financial Future

Start small: Review your mortgage statement today, calculate extras with a payoff calculator, and automate your first additional payment. Consult a HUD-approved counselor via hud.gov for personalized advice. By 2030, you could be mortgage-free, with more for 401(k)s, Medicare planning, or family vacations.

Frequently Asked Questions

Sources & References

-

1

Dave Ramsey's 6 Proven Strategies To Pay Off Your Mortgage Faster — www.nasdaq.com

-

2

Tips on How to Pay Off Your Mortgage Early - Nationwide — www.nationwide.com

-

3

Why So Many People Are Paying Off Their Mortgage in 2026 — www.youtube.com

-

4

When Should You Pay Off Your Mortgage Early? - Bankrate — www.bankrate.com

-

5

How to Pay Off Debt: Top Strategies for 2026 - NerdWallet — www.nerdwallet.com

Useful Tools

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...