VA Home Loan Benefits: Who Qualifies and How to Apply

Imagine finally settling into a home of your own without the burden of a down payment or private mortgage insurance—benefits that many Americans dream of but few can access. VA home loans make this a...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine finally settling into a home of your own without the burden of a down payment or private mortgage insurance—benefits that many Americans dream of but few can access. VA home loans make this a reality for eligible veterans, service members, and their families, offering some of the most favorable mortgage terms available today. In 2026, these loans continue to provide no down payment, competitive rates, and flexible guidelines, helping you build equity and stability after your service.

What Are VA Home Loan Benefits?

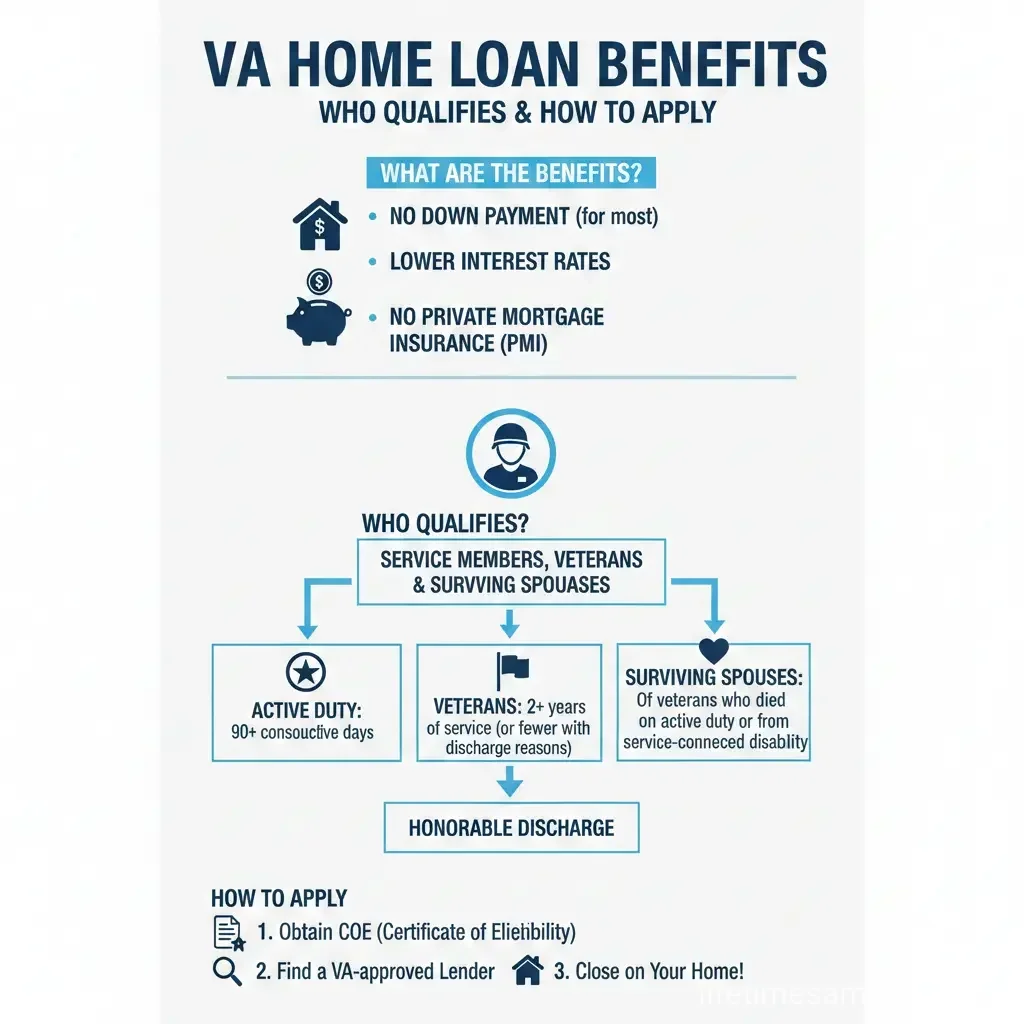

VA home loans, backed by the U.S. Department of Veterans Affairs, are designed to make homeownership achievable for those who've served our nation. Unlike conventional loans, they eliminate the need for a down payment in most cases and skip private mortgage insurance (PMI), saving you thousands upfront and monthly. Key perks include:

- No down payment required—lenders may request one based on credit, but the VA does not.

- Competitive interest rates that often beat market averages.

- Limited closing costs, with no commissions or fees for VA staff.

- No PMI, reducing your monthly payment significantly.

- Lifetime benefit—reuse the guaranty multiple times after selling or paying off a loan.

- No loan limits for full entitlement borrowers in 2026, allowing financing for higher-priced homes.

These advantages stem from the VA's guaranty, which covers up to 25% of the loan amount, reassuring lenders and passing savings to you. In 2026, full entitlement means most veterans face no caps, making big moves—like from a Texas base to a California dream home—feasible without extra cash.

Who Qualifies for VA Home Loan Benefits?

Eligibility hinges on your military service, not just credit or income—though lenders overlay their standards. You must obtain a Certificate of Eligibility (COE) proving your service qualifies you. Here's who typically makes the cut in 2026:

Active Duty Service Members

- 90 consecutive days during wartime.

- 181 days during peacetime.

- Still serving or discharged under conditions other than dishonorable.

Veterans

- Meets active duty minimums above.

- Discharged honorably, or under hardship, convenience of government (at least 20 months of 2-year enlistment), early out (21 months), reduction in force, medical conditions, or service-connected disability.

National Guard and Reserves

- 6 creditable years and still serving, or honorably discharged/retired.

- 90 days non-training active duty (Title 10).

- 90 days active duty including 30 consecutive days under Title 32 sections 316, 502, 503, 504, or 505.

Spouses may qualify if the veteran is permanently disabled or deceased from service-related causes—apply via VA Form 21P-534EZ with marriage license and death certificate. Active Guard/Reserves need a Statement of Service and points statement; discharged use DD Form 214 or NGB Form 22/23.

Credit and Income Requirements

The VA sets no hard minimum credit score, but most lenders require 620+ FICO. Scores of 580-619 may work with strong residual income, low debt, and stable job history. Expect:

- Stable 12+ months payment history.

- No bankruptcy <2 years or foreclosure <3 years.

- Debt-to-income (DTI) under 41%, flexible with residual income.

Residual income is key: money left after bills for living expenses, varying by family size and region (e.g., higher in high-cost areas like New York).

Occupancy and Property Rules

You must occupy the home as your primary residence within 60 days (exceptions for deployments). Eligible properties include single-family homes (up to 4 units), VA-approved condos, manufactured homes. They must meet Minimum Property Requirements (MPRs): safe water/sewage, heating, sound structure, no lead paint hazards (pre-1978 homes).

How to Apply for a VA Home Loan in 2026

Applying is straightforward: get your COE, shop lenders, and submit. Here's your step-by-step guide:

- Request your COE: Use VA's eBenefits portal, mail VA Form 26-1880, or ask your lender. Need DD214, service records.

- Check your finances: Pull free credit reports (annualcreditreport.com), calculate DTI, verify residual income.

- Get pre-approved: Contact VA-approved lenders like Veterans United or Rocket Mortgage. Provide COE, pay stubs, tax returns.

- Find a home: Work with a real estate agent experienced in VA loans. Get it appraised to VA MPRs.

- Submit full application: Lender underwrites based on ability-to-repay, including residual income.

- Close the loan: Pay funding fee (1.25%-3.3% of loan, waivable for disabled vets), sign docs. No down payment needed.

Pro tip: Shop multiple lenders—rates vary. Use VA's lender tool at va.gov. In 2026, full entitlement skips loan limits, but lenders may require 25% coverage via entitlement/down payment.

Practical Tips for Success

- Boost your score: Pay down debt, fix errors before applying.

- Save for funding fee: Roll it into the loan if needed.

- Calculate residual: Use VA worksheets for your region/family size.

- Avoid new debt: No big purchases pre-approval.

- Partner with VA-savvy agents: They know MPRs and seller concessions (up to 4% allowed).

For example, a Texas veteran with 620 FICO, 35% DTI, and strong residuals could finance a $400,000 home with zero down—saving $80,000 upfront versus conventional.

Next Steps to Secure Your VA Home Loan

Start today: Log into eBenefits for your COE, pull your credit report, and connect with a VA lender. With no down payment and flexible terms, 2026 is prime time to claim your homeownership benefit. Visit va.gov/housing-assistance for tools, or call 877-827-3702. Your service earned this—make it yours.

Frequently Asked Questions

Sources & References

-

1

VA Home Loan Eligibility Guidelines — www.newdayusa.com

-

2

2025 VA Loan Eligibility Requirements — www.veteransunited.com

-

3

How Did VA Loan Requirements Change For 2026? — valoannetwork.com

-

4

VA Loan Requirements for 2025 — www.experian.com

- 5

-

6

VA Home Loans - Veterans Benefits Administration — www.benefits.va.gov

- 7

-

8

VA loan limits for 2025: What you need to know — www.rocketmortgage.com

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...