Required Minimum Distributions (RMDs) Explained Simply

Imagine reaching retirement only to find Uncle Sam knocking on your door, demanding a portion of your hard-earned savings each year. That's the reality of Required Minimum Distributions (RMDs), the ma...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine reaching retirement only to find Uncle Sam knocking on your door, demanding a portion of your hard-earned savings each year. That's the reality of Required Minimum Distributions (RMDs), the mandatory withdrawals from your tax-deferred retirement accounts starting at age 73. But don't worry—understanding RMDs doesn't have to be complicated. This guide breaks it down simply, with practical steps to help you navigate 2026 rules and keep more of your money working for you.

What Are Required Minimum Distributions (RMDs)?

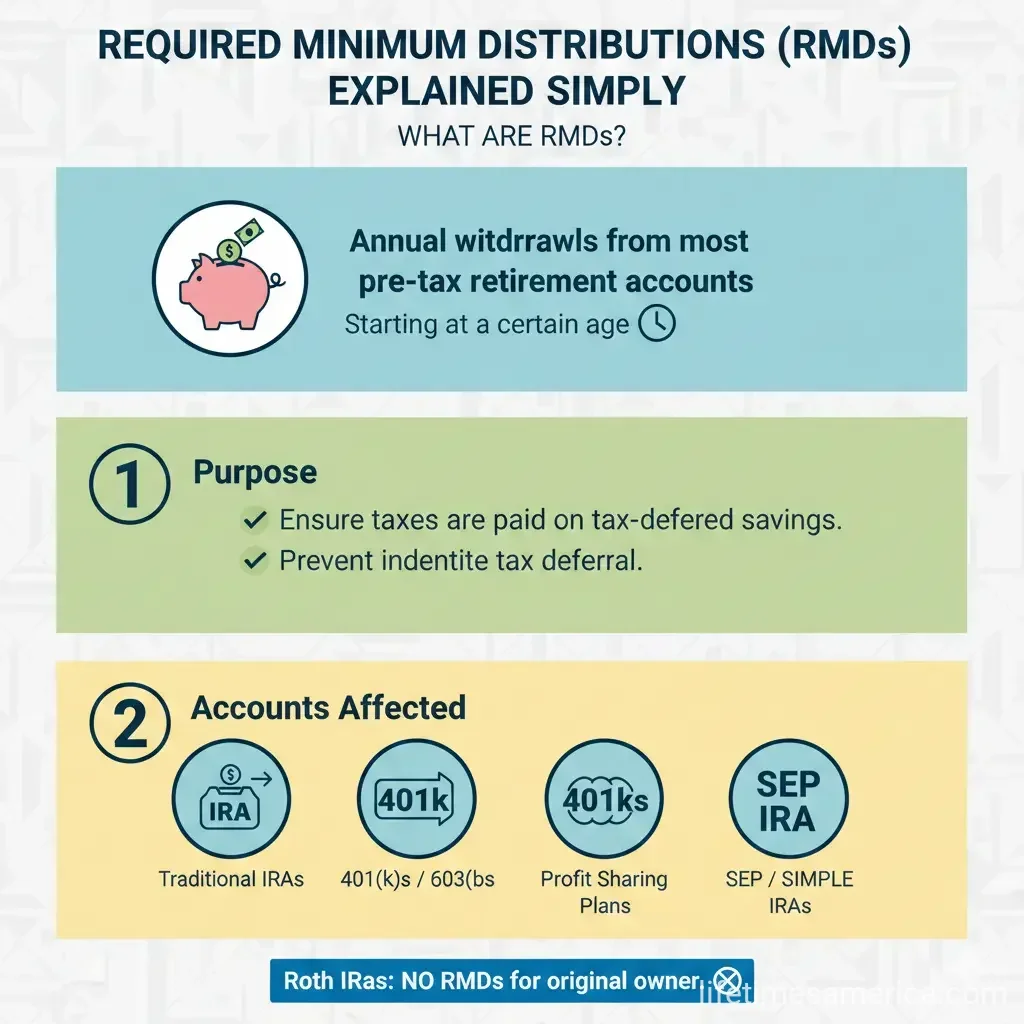

Required Minimum Distributions, or RMDs, are the minimum amounts you must withdraw annually from certain retirement accounts once you hit the required age. These rules ensure you don't defer taxes on these funds indefinitely. In 2026, if you're turning 73, it's time to start planning your first withdrawal.

RMDs apply to tax-deferred accounts like Traditional IRAs, SEP IRAs, SIMPLE IRAs, 401(k)s, 403(b)s, profit-sharing plans, and 457(b) plans. Good news: Roth IRAs are exempt during your lifetime, and starting in 2024, Roth 401(k)s and Roth 403(b)s no longer require RMDs.

Withdrawals count as ordinary income, so they'll be taxed at your regular rate. You can always take more than the minimum, but falling short triggers penalties.

Who Needs to Take RMDs in 2026?

- Anyone turning 73 in 2026 must begin RMDs that year.

- IRA owners: Start at 73, even if still working.

- 401(k) or similar plan participants: Can delay until retirement, unless you're a 5% business owner.

- Inherited accounts have separate rules—consult IRS Publication 590-B for details.

When Do RMDs Start? Key 2026 Deadlines

Thanks to the SECURE 2.0 Act, the RMD age rose from 72 to 73 in 2023 and will hit 75 in 2033. For 2026:

- First RMD: Due by April 1 of the year after you turn 73. If you turn 73 in 2026, take it by April 1, 2027.

- Subsequent RMDs: December 31 each year.

- Watch out: Delaying your first RMD means two withdrawals in one tax year (e.g., 2026 and 2027 RMDs both in 2027), potentially bumping you into a higher tax bracket.

Real-Life Example for 2026

Say you're 73 in 2026 with a traditional IRA. Your first RMD is based on your December 31, 2025, balance. You can wait until April 1, 2027, but then you'll owe your 2027 RMD by December 31, 2027—both taxable in 2027.

How to Calculate Your RMD for 2026

Calculating your RMD is straightforward: Divide your account balance as of December 31 of the prior year by a life expectancy factor from IRS tables in Publication 590-B.

Formula: RMD = Account Balance (Dec. 31 prior year) ÷ Life Expectancy Factor

Which IRS Table to Use?

- Uniform Lifetime Table: For most people. At age 73, factor is about 26.5; age 75 is 24.6.

- Joint Life Table: If your spouse is your sole beneficiary and 10+ years younger.

- New tables apply from 2022 onward for longer life expectancies.

Step-by-Step Calculation Example

You're 74 in 2026, married to a spouse 5 years younger (sole beneficiary). Your IRA balance on December 31, 2025: $200,000. Using the Joint Life Table, factor is 25.5.

RMD = $200,000 ÷ 25.5 = $7,843. Withdraw at least this by December 31, 2026.

Another example: Age 75, $500,000 balance (Dec. 31, 2025), Uniform Table factor 24.6. RMD = $500,000 ÷ 24.6 ≈ $20,325.

Multiple Accounts? Here's the Rule

- Calculate each 401(k), 457(b), or similar separately—withdraw from each.

- For multiple IRAs or 403(b)s: Calculate total RMD, withdraw from any one (or combination).

Use free online calculators from IRS partners or financial sites, but verify with your records.

Penalties for Missing Your RMD

Don't miss deadlines—penalties are steep. The excise tax is 25% of the undistributed amount, dropping to 10% if corrected within two years.

Pro Tip: File IRS Form 5329 to report and pay, or request a waiver if you have reasonable cause.

Strategies to Manage RMDs Effectively

RMDs force taxable income, but smart planning minimizes the hit. Here are actionable tips for 2026:

Qualified Charitable Distributions (QCDs)

Over 70½? Donate up to $105,000 (2026 limit, inflation-adjusted) directly from your IRA to charity. Counts toward RMD but isn't taxable income.

Example: $100,000 RMD, donate $50,000 via QCD. Taxable income drops by $50,000, plus potential senior deductions.

Other Tactics

- Convert to Roth IRA beforehand (pay taxes now, avoid future RMDs).

- Work longer if possible to delay 401(k) RMDs.

- Bundle withdrawals or use for Roth conversions strategically.

- Consider tax-loss harvesting to offset RMD income.

Recent Changes from SECURE 2.0 Act

The SECURE 2.0 Act brought welcome updates:

- RMD age to 75 by 2033.

- No RMDs for Roth 401(k)s/403(b)s after 2023.

- Lower penalties and automatic waivers in some cases.

- Expanded QCD limits.

Frequently Asked Questions

Next Steps to Prepare for Your 2026 RMD

Stay ahead: Review account balances by December 31, 2025. Use IRS worksheets or calculators. Talk to a tax advisor or financial planner about QCDs, conversions, or tax strategies. Download IRS Publication 590-B from irs.gov and set calendar reminders for deadlines. With planning, RMDs become a manageable part of your retirement—not a surprise tax bill.[3]

You're now equipped to handle RMDs confidently. Start calculating today and enjoy the retirement you've earned.

Sources & References

Required Minimum Distribution (RMD) 2026 Calculator and Table — nerdwallet.com[1]

Understanding Required Minimum Distributions (RMDs) for 2026 — irafinancial.com[2]

Retirement plan and IRA required minimum distributions FAQs - IRS — irs.gov[3]

RMD Rules for 2026: Deadlines, Penalties, and Changes — schneiderdowns.com[4]

Retirement topics - Required minimum distributions (RMDs) - IRS — irs.gov[5]

Required Minimum Distributions: What's New in 2026 — schwab.com[6]

Required Minimum Distributions: Know Your Deadlines - FINRA.org — finra.org[7]

How Required Minimum Distributions (RMDs) Work - Edward Jones — edwardjones.com[8]

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...