What Is a Roth 401(k) and How Is It Different from a Regular 401(k)?

If you're saving for retirement, you've probably heard about 401(k) plans. But did you know there's a version that lets you contribute after-tax dollars and potentially withdraw money tax-free in reti...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're saving for retirement, you've probably heard about 401(k) plans. But did you know there's a version that lets you contribute after-tax dollars and potentially withdraw money tax-free in retirement? That's the Roth 401(k), and it's becoming an increasingly popular option for Americans looking to maximize their retirement savings strategy.

The choice between a Roth 401(k) and a traditional 401(k) isn't just a minor detail—it can significantly impact how much money you have available in retirement. Understanding the differences between these two accounts will help you make the right decision for your financial situation.

What Is a Roth 401(k)?

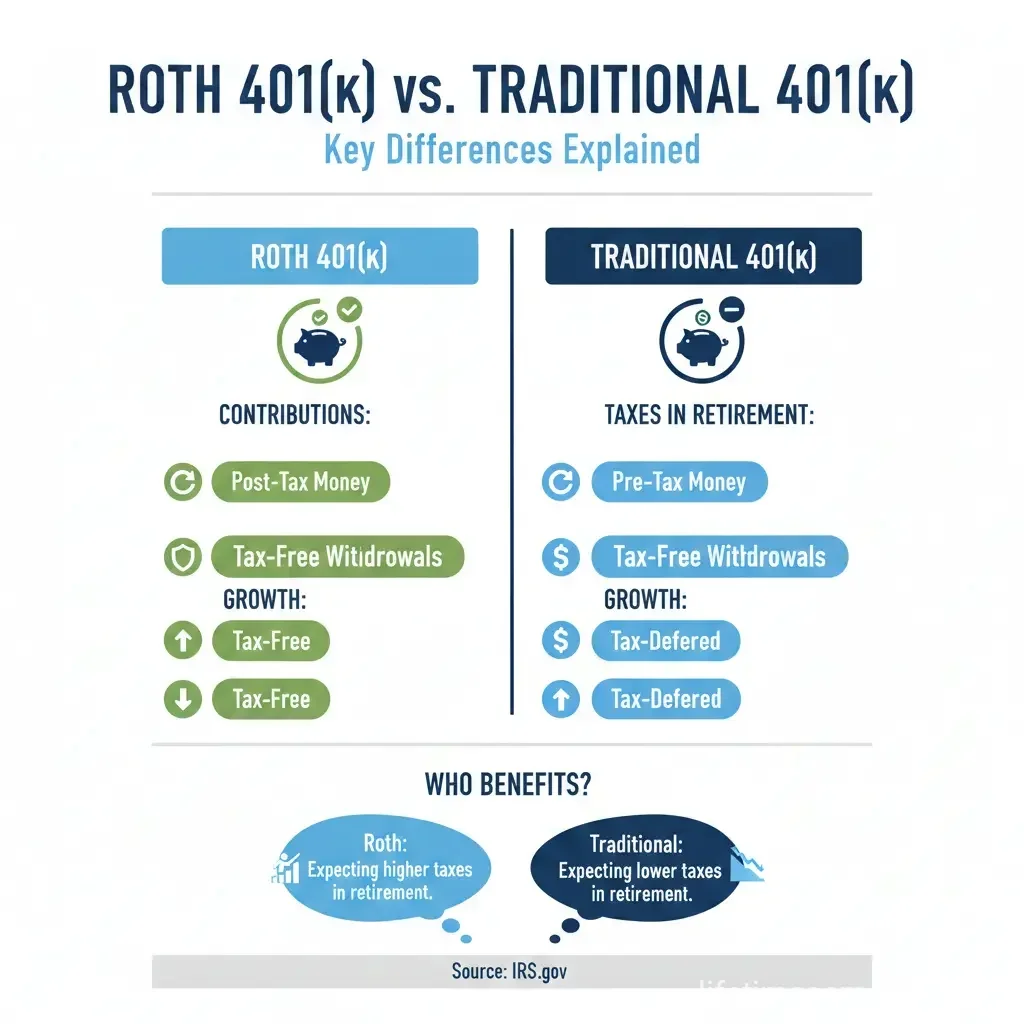

A Roth 401(k) is a hybrid retirement account that combines features of both a Roth IRA and a traditional 401(k). Here's how it works: You contribute money that's already been taxed (after-tax dollars), and then your contributions and earnings grow tax-free. When you're ready to withdraw the money in retirement, you won't pay taxes on qualified distributions.

The key advantage? You're paying taxes now on your contributions, so the IRS gets its cut upfront. This means your money grows tax-free, and you won't owe federal income taxes when you eventually withdraw it.

Roth 401(k) vs. Traditional 401(k): Key Differences

How Contributions Work

The most fundamental difference between these accounts is when you pay taxes:

- Traditional 401(k): You contribute pre-tax dollars, which reduces your taxable income for the year. This means you get an immediate tax break on your paycheck.

- Roth 401(k): You contribute after-tax dollars. Income taxes are already deducted from your paycheck before your contribution is taken out.

Let's say you earn $100,000 annually and want to contribute $10,000 to your 401(k). With a traditional 401(k), you'd only pay taxes on $90,000 that year. With a Roth 401(k), you'd pay taxes on the full $100,000, but that $10,000 contribution is yours tax-free forever.

Contribution Limits and Income Restrictions

One major advantage of a Roth 401(k) is that there are no income limits. This is a game-changer for high earners who want to take advantage of Roth benefits.

Here's how the 2026 contribution limits compare:

- Roth 401(k): Up to $23,500 per year (or more with catch-up contributions)

- Roth IRA: Up to $7,000 per year, but only if your income is below $165,000 (single) or $246,000 (married filing jointly)

- Traditional 401(k): Same $23,500 limit as Roth 401(k)

For those age 50 and older, you can add an extra $7,500 catch-up contribution to either a Roth or traditional 401(k). And if you're between ages 60-63, you can contribute an additional $11,250.

Tax Treatment of Withdrawals

This is where the real difference becomes clear:

- Traditional 401(k): Withdrawals of both contributions and earnings are taxed as ordinary income.

- Roth 401(k): Qualified withdrawals of contributions and earnings are completely tax-free.

With a Roth 401(k), if you withdraw money before age 59½, your contributions come out tax and penalty-free (since you already paid taxes on them). However, any earnings withdrawn early may be subject to taxes and a 10% penalty. Once you reach 59½ and have held the account for at least five years, you can withdraw both contributions and earnings tax-free.

Early Withdrawal Rules

Both account types have penalties for early withdrawal, but the rules differ slightly:

- Traditional 401(k): If you withdraw before age 59½, you'll owe income taxes and a 10% penalty on the entire distribution. However, if you separate from service at age 55 or older, you're exempt from the 10% penalty.

- Roth 401(k): Your contributions are always accessible tax and penalty-free. Only earnings withdrawn before age 59½ may be subject to taxes and penalties.

Required Minimum Distributions (RMDs)

This is one of the most significant advantages of a Roth 401(k). Thanks to the SECURE 2.0 Act, Roth 401(k)s no longer require you to take distributions during your lifetime. This means your money can continue growing tax-free for as long as you live.

Traditional 401(k)s are different—you must begin taking required minimum distributions at age 73. This can push you into a higher tax bracket and affect your Medicare premiums and Social Security taxation.

This RMD advantage makes Roth 401(k)s particularly attractive for people who don't need the money in retirement and want to leave a larger inheritance to their heirs.

Who Should Choose a Roth 401(k)?

A Roth 401(k) makes sense if you fall into one of these categories:

- You expect to be in a higher tax bracket in retirement: If you think your tax rate will be higher when you retire than it is now, paying taxes today at a lower rate is advantageous.

- You're a high earner: Roth 401(k)s have no income limits, making them perfect for high-income Americans who can't contribute to Roth IRAs.

- You want to leave money to heirs: Roth assets can pass to beneficiaries with potential tax advantages.

- You don't need the money in retirement: The lack of RMDs means your money can keep growing tax-free.

- You're young and have decades until retirement: The longer your money has to grow tax-free, the more you benefit.

Who Should Stick with a Traditional 401(k)?

A traditional 401(k) might be better if:

- You need the immediate tax deduction: If you're in a high tax bracket now and want to reduce your current taxable income, a traditional 401(k) provides that benefit.

- You expect to be in a lower tax bracket in retirement: If you think you'll pay less in taxes once you retire, deferring taxes makes sense.

- You need more cash flow now: The tax deduction from a traditional 401(k) means more money stays in your paycheck.

- You're planning to retire soon: You won't have as much time to benefit from tax-free growth.

Can You Have Both?

Many employers offer both Roth and traditional 401(k) options in the same plan. You can split your contributions between the two types, giving you flexibility to hedge your bets on future tax rates. For example, you might contribute $15,000 to a traditional 401(k) and $8,500 to a Roth 401(k), as long as your total doesn't exceed the annual limit.

Roth 401(k) vs. Roth IRA: What's the Difference?

While both accounts are "Roth" accounts with similar tax benefits, they have important differences:

| Feature | Roth 401(k) | Roth IRA |

|---|---|---|

| Contribution Limit (2026) | $23,500 | $7,000 |

| Income Limits | None | $165,000 (single), $246,000 (married) |

| RMDs During Lifetime | None | None |

| Employer Match | Possible | Not available |

Making Your Decision

Choosing between a Roth and traditional 401(k) ultimately comes down to predicting your future tax situation. If you believe tax rates will be higher in retirement, a Roth 401(k) is likely the better choice. If you think you'll be in a lower tax bracket once you retire, a traditional 401(k) makes more sense.

The good news? If your employer offers both options, you don't have to choose just one. You can split your contributions to take advantage of both accounts' benefits. This strategy gives you tax diversification in retirement—some money that's already been taxed and some that will be taxed when withdrawn.

Next Steps: Review your employer's 401(k) plan documents to see if a Roth option is available. If it is, consider meeting with a financial advisor or tax professional to determine which option aligns with your retirement goals. You can also use online calculators to compare scenarios based on your specific income and retirement timeline. The decision you make today can have a significant impact on your financial security in retirement, so it's worth taking the time to get it right.

Frequently Asked Questions

Sources & References

-

1

Should You Consider a Roth 401(k)? | Charles Schwab — www.schwab.com

-

2

Roth 401(k) vs. Traditional 401(k): Understanding the Key Differences | Johnson Financial Group — www.johnsonfinancialgroup.com

-

3

Pros and Cons of a Roth 401(k) | Fidelity — www.fidelity.com

-

4

Roth Comparison Chart | Internal Revenue Service — www.irs.gov

Useful Tools

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...