What Is Dollar-Cost Averaging and Should You Use It?

Dollar-cost averaging is a straightforward investment strategy that can help you build wealth steadily while avoiding the stress of trying to time the market perfectly. Whether you're saving for retir...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Dollar-cost averaging is a straightforward investment strategy that can help you build wealth steadily while avoiding the stress of trying to time the market perfectly. Whether you're saving for retirement through a 401(k), investing in individual stocks, or building an emergency fund, understanding this approach could transform how you think about investing.

What Is Dollar-Cost Averaging?

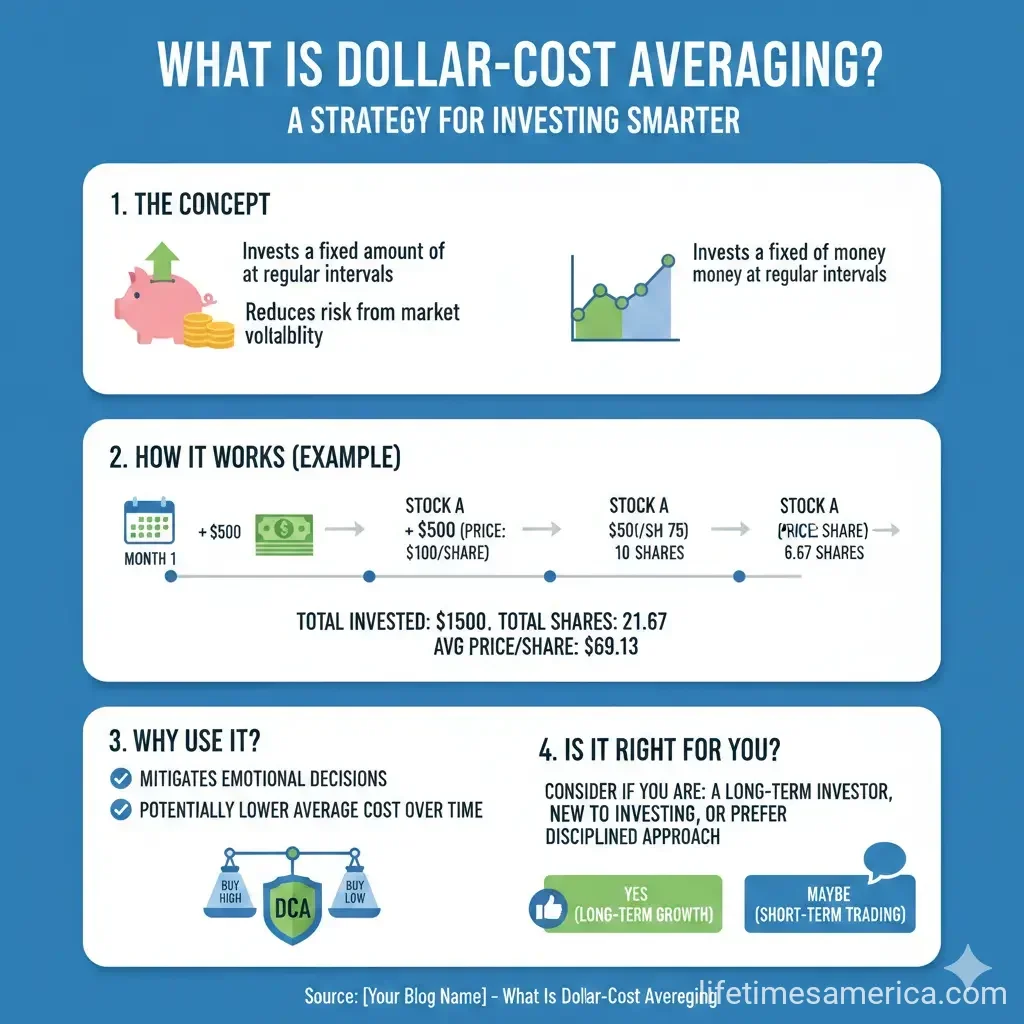

Dollar-cost averaging (DCA) is the practice of investing a fixed amount of money at regular intervals—such as weekly, monthly, or quarterly—regardless of current market conditions. Instead of trying to predict when the market will go up or down, you simply invest the same amount on a consistent schedule.

For example, you might contribute $500 every month to a stock mutual fund, or $200 biweekly to your 401(k). Whether the market is soaring or plummeting, you're putting in the same amount. This removes the guesswork from investing and helps you focus on long-term goals rather than short-term market movements.

How Dollar-Cost Averaging Works in Practice

Here's a concrete example to illustrate how DCA works:

Let's say you invest $500 monthly in the same investment. When the price per share is $24, you'd buy approximately 20.83 shares. When the price rises to $25, you'd buy 20 shares. When it jumps to $28, you'd buy only 17.86 shares. By spreading your investment over time, you're buying more shares when prices are low and fewer when prices are high.

The key insight: your average purchase price per share becomes lower than if you'd invested all your money at once, especially if you started at a market peak.

Why Americans Use Dollar-Cost Averaging

It Takes Emotion Out of Investing

One of the biggest advantages of DCA is psychological. When the stock market drops, many investors panic and sell at the worst possible time. When markets surge, they rush in, often buying just before a correction. Dollar-cost averaging removes this emotional rollercoaster by creating a disciplined system you follow regardless of market conditions.

This is especially valuable during recessions and bear markets, when fear can override rational decision-making.

It Helps You Avoid "Timing the Market"

Professional investors struggle to time the market perfectly—and ordinary investors shouldn't expect to do better. By investing fixed amounts regularly, you're guaranteed to buy at various price points throughout the market cycle. You won't catch the absolute bottom, but you also won't be fooled into buying at the peak.

It Reduces Risk Through Consistency

Dollar-cost averaging spreads your investment risk over time rather than concentrating it all at once. If you invested $12,000 in January and the market crashed in February, you'd suffer a significant loss. With DCA, you'd only have invested $1,000 in January, limiting your exposure to that particular market condition.

It Makes Investing More Accessible

You don't need a large lump sum to start investing with DCA. Many Americans use this strategy through their 401(k) plans at work, where contributions are automatically deducted from each paycheck. This makes investing a natural part of your budget rather than a special financial event.

The Numbers: A Real Example

Let's look at a concrete scenario comparing DCA to investing everything at once:

Imagine you have $12,000 to invest in stock ABCD. The stock price fluctuates over time.

- With lump-sum investing (putting all $12,000 in at once), you buy a fixed number of shares at that single price point

- With dollar-cost averaging (investing $1,000 monthly), you buy different quantities at different prices

Because you own more shares through DCA, when the stock price eventually rises, your total profit grows more quickly. Even if the stock falls to $40 per share—below your average cost—you'd still have an overall gain with DCA that you wouldn't have with lump-sum investing at a higher price.

Dollar-Cost Averaging and Your 401(k)

If you have a 401(k) through your employer, you're already using dollar-cost averaging. Your contributions are automatically deducted from each paycheck and invested in your chosen funds. This consistent approach is specifically designed to help you weather market volatility and build long-term retirement savings.

The IRS allows you to contribute up to $23,500 annually to a traditional or Roth 401(k) in 2024 (check current limits for 2026 with your plan administrator). By spreading these contributions across 26 paychecks, you're naturally practicing dollar-cost averaging.

Potential Downsides to Consider

You Might Miss Out on Higher Returns

Here's the honest trade-off: in a consistently rising market, investing everything at once would generate higher returns than spreading it out. If you had invested $12,000 in January 2009 (right after the financial crisis), you would've done better than someone who invested $1,000 monthly for the next year. However, no one can reliably predict when the market will rise, so this advantage only exists in hindsight.

Transaction Fees Can Add Up

Some brokers charge per-transaction fees for frequent trades. However, most modern brokers—including major platforms used by Americans—now offer commission-free trading for stocks and ETFs. Check with your specific broker to confirm their fee structure before implementing a DCA strategy.

You're Holding Cash Longer

With DCA, you're keeping money in cash (earning minimal interest) while you wait to invest it. In a bull market, this cash could have been generating returns. This is the opportunity cost of the strategy—you sacrifice potential gains for reduced risk and peace of mind.

Is Dollar-Cost Averaging Right for You?

Consider These Factors

Your investment timeline: DCA works best if you're investing for the long term—typically at least 5-10 years or longer. If you need the money soon, this strategy may not be appropriate.

Your risk tolerance: If market volatility keeps you up at night, DCA's steady approach provides psychological comfort. If you're comfortable with risk and have a longer timeline, lump-sum investing might work better.

Your available funds: If you're receiving regular income (like a salary), DCA happens naturally. If you have a large sum available now, you'll need to decide whether to invest it all or spread it out.

Your market outlook: DCA is particularly valuable if you're uncertain about market conditions or concerned about volatility. If you're confident the market will rise, lump-sum investing might appeal to you more.

Getting Started with Dollar-Cost Averaging

Step 1: Determine your investment amount. How much can you comfortably invest at each interval? Even $50-100 monthly adds up over time through compound growth.

Step 2: Choose your investment. Select a diversified mutual fund, ETF, or mix of investments aligned with your risk tolerance and timeline.

Step 3: Set up automatic contributions. Use your employer's 401(k) plan, set up automatic transfers from your bank account, or use your broker's automatic investment plan. Automation removes the temptation to skip months.

Step 4: Stay consistent. Don't panic-sell during downturns or try to time market peaks. Stick to your schedule regardless of market conditions.

Step 5: Review periodically. Check your progress annually, but don't obsess over short-term fluctuations. Rebalance your portfolio if your asset allocation drifts from your target.

The Bottom Line

Dollar-cost averaging isn't a get-rich-quick scheme or a guaranteed path to wealth. What it is: a practical, emotion-reducing strategy that helps ordinary Americans build long-term wealth without needing to predict market movements.

If you're already contributing to a 401(k) through your employer, you're already benefiting from dollar-cost averaging. If you're investing outside of retirement accounts, implementing a regular investment schedule—whether monthly, quarterly, or another interval—can help you reach your financial goals with less stress and fewer emotional decisions.

The best investment strategy is one you'll actually stick with for years. For most Americans, that's dollar-cost averaging.

Frequently Asked Questions

Sources & References

-

1

Benefits of Dollar Cost Averaging - Gasaway Investment Advisors — www.gasawayinvestments.com

-

2

What Is Dollar Cost Averaging? | Ally — www.ally.com

-

3

Dollar-Cost Averaging: How It Works, Pros and Cons - NerdWallet — www.nerdwallet.com

-

4

The Pros and Cons of Dollar-Cost Averaging | FINRA.org — www.finra.org

- 5

-

6

What is Dollar Cost Averaging? | Wells Fargo Advisors — www.wellsfargoadvisors.com

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...